Videos

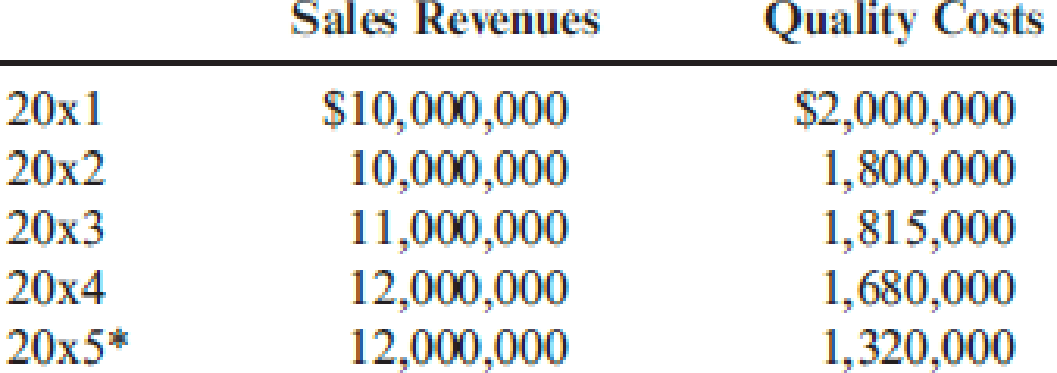

Iona Company, a large printing company, is in its fourth year of a five-year, quality improvement program. The program began in 20x0 with an internal study that revealed the quality costs being incurred. In that year, a five-year plan was developed to lower quality costs to 10 percent of sales by the end of 20x5. Sales and quality costs for each year are as follows:

* Budgeted figures.

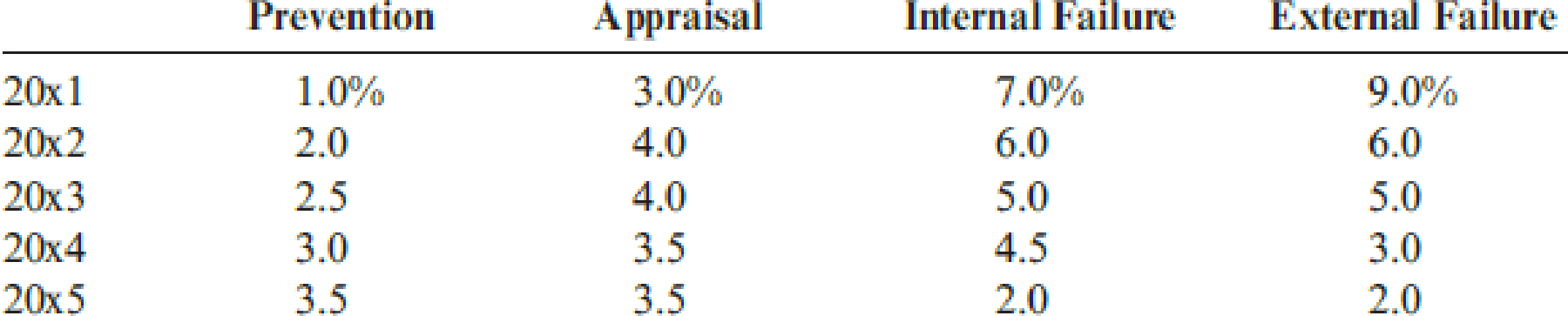

Quality costs by category are expressed as a percentage of sales as follows:

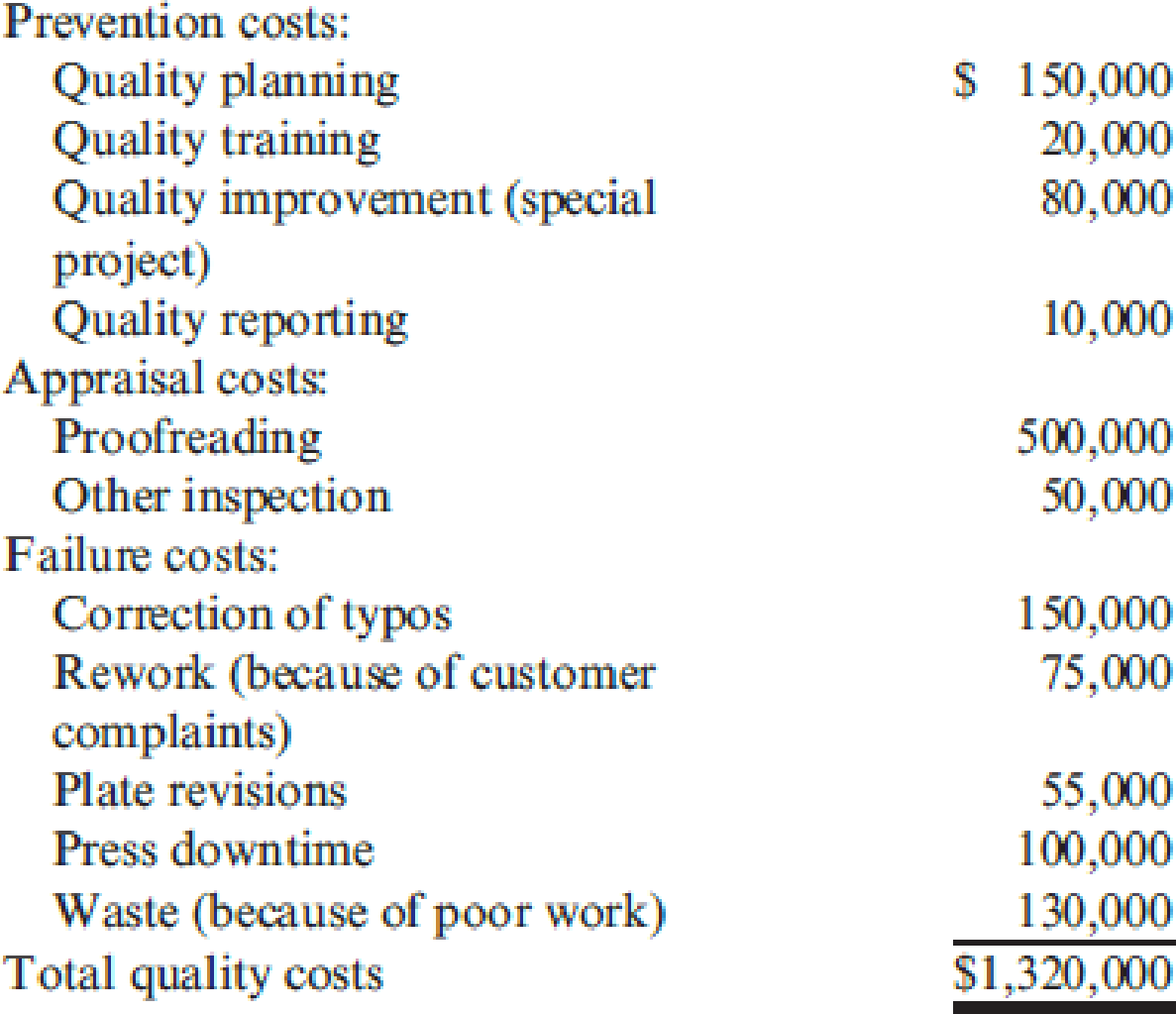

The detail of the 20x5 budget for quality costs is also provided.

All prevention costs are fixed; all other quality costs are variable.

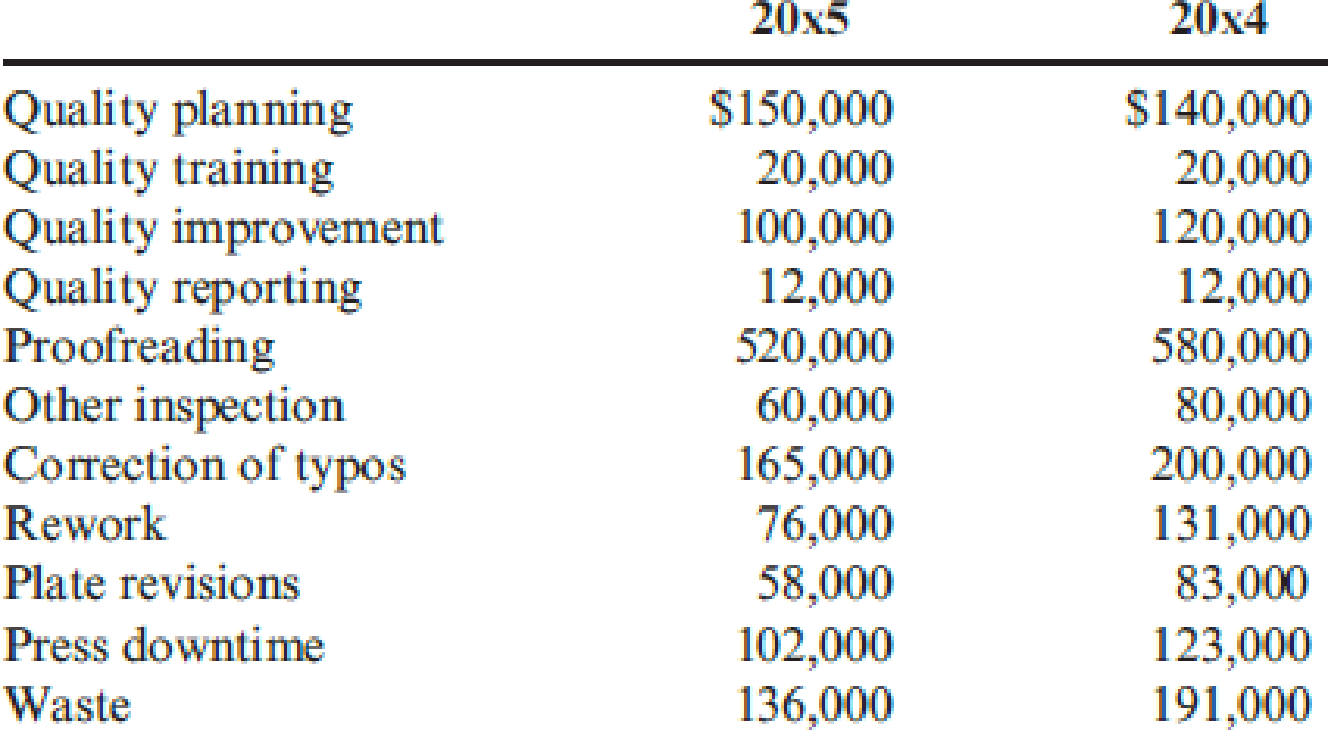

During 20x5, the company had $12 million in sales. Actual quality costs for 20x4 and 20x5 are as follows:

Required:

- 1. Prepare an interim quality cost performance report for 20x5 that compares actual quality costs with budgeted quality costs. Comment on the firm’s ability to achieve its quality goals for the year.

- 2. Prepare a one-period quality performance report for 20x5 that compares the actual quality costs of 20x4 with the actual costs of 20x5. How much did profits change because of improved quality?

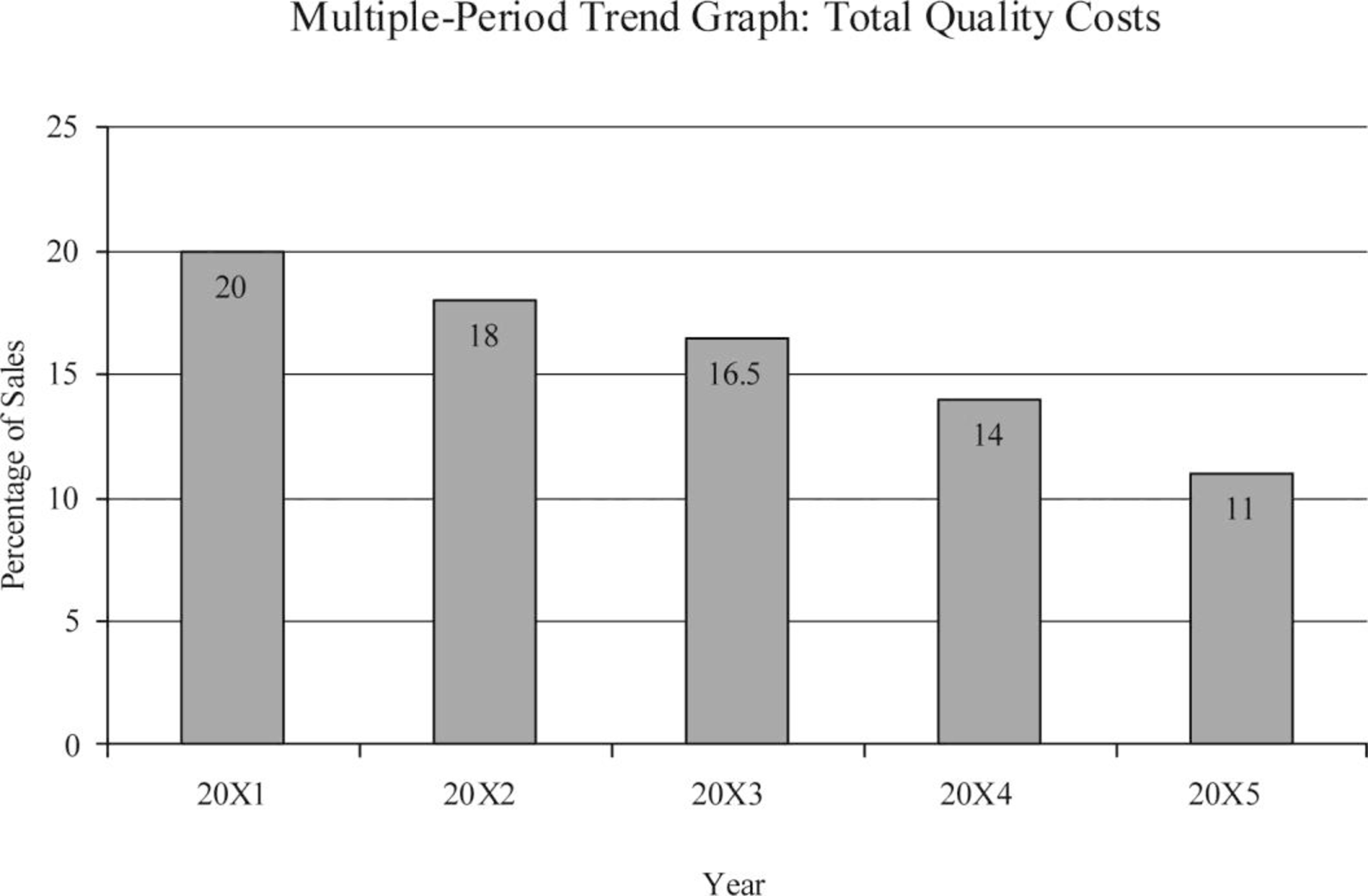

- 3. Prepare a graph that shows the trend in total quality costs as a percentage of sales since the inception of the quality improvement program.

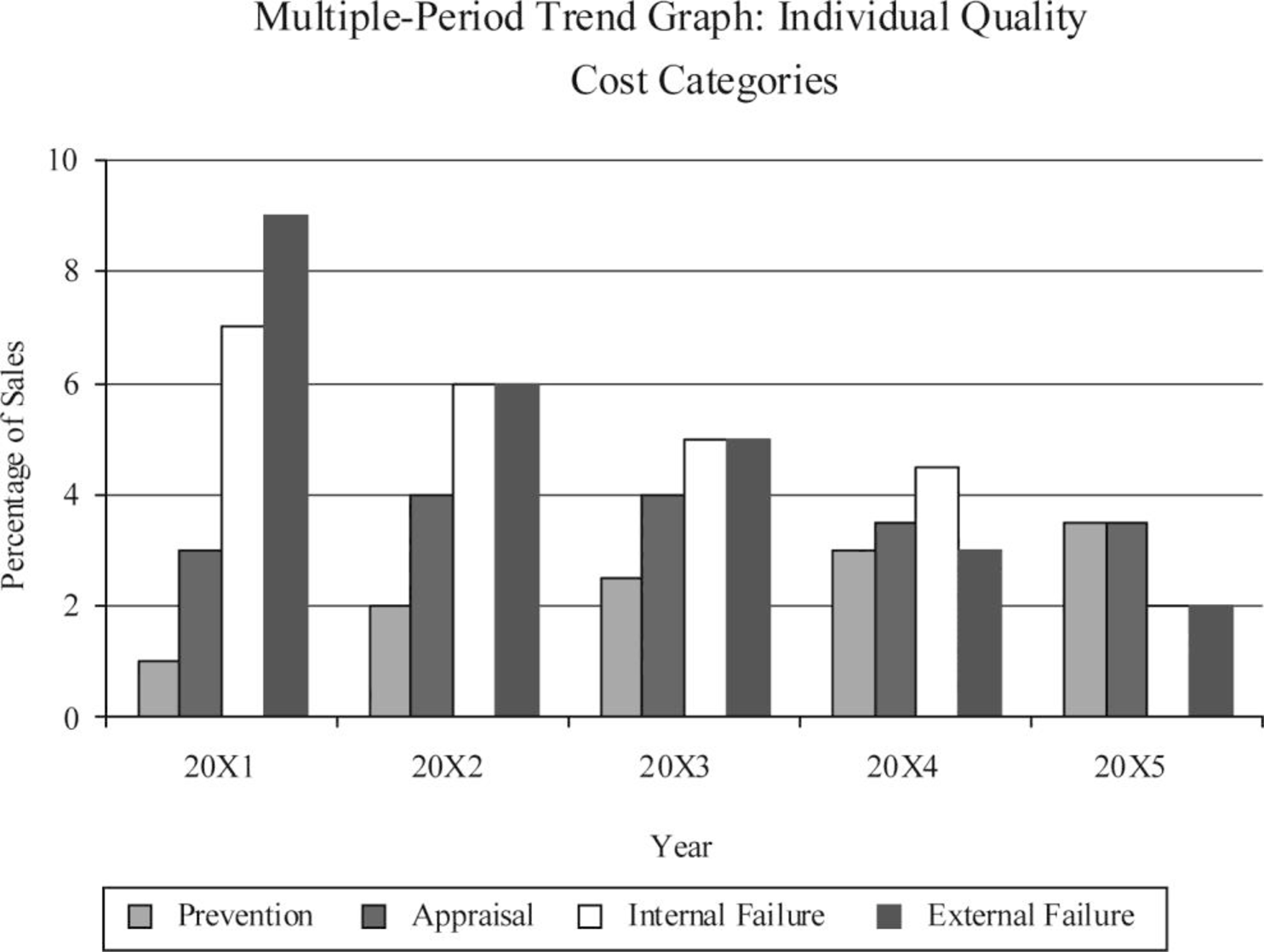

- 4. Prepare a graph that shows the trend for all four quality cost categories for 20x1 through 20x5. How does this graph help management know that the reduction in total quality costs is attributable to quality improvements?

- 5. Assume that the company is preparing a second five-year plan to reduce quality costs to 2.5 percent of sales. Prepare a long-range quality cost performance report assuming sales of $15 million at the end of five years. Assume that the final planned relative distribution of quality costs is as follows: proofreading, 50 percent; other inspection, 13 percent; quality training, 30 percent; and quality reporting, 7 percent.

1.

Prepare an interim quality cost performance report for the year 20x5 that compares actual quality costs with budgeted quality costs and comment on the ability of the firm for achieving its quality goals for the year.

Explanation of Solution

Quality cost performance reports: In a quality cost performance report, identification of quality standard is the main element and it has two important elements namely; actual outcomes and expected or standard outcomes.

Interim quality report: Interim quality performance report compares the actual quality at the end of the period with the budgeted costs and this report examines the progress attained within the period comparative to the planned level of progress for that period.

Prepare an interim quality cost performance report for the year 20x5:

| Company I | ||||

| Interim Performance Report: Quality Costs | ||||

| For the Year Ended December 31, 20x5 | ||||

| Particulars |

Actual Costs (a) |

Budgeted costs (b) |

Variance | |

| Prevention costs: | ||||

| Fixed: | ||||

| Quality planning | $150,000 | $150,000 | $0 | |

| Quality training | $20,000 | $20,000 | $0 | |

| Quality improvement | $100,000 | $80,000 | $20,000 | U |

| Quality reporting | $12,000 | $10,000 | $2,000 | U |

| Total prevention costs | $282,000 | 260,000 | $22,000 | U |

| Appraisal costs: | ||||

| Variable: | ||||

| Proofreading | $520,000 | $500,000 | $20,000 | U |

| Other inspection | $60,000 | $50,000 | $10,000 | U |

| Total appraisal costs | $580,000 | 550,000 | $30,000 | U |

| Failure costs: | ||||

| Variable: | ||||

| Correction of typos | $165,000 | $150,000 | $15,000 | U |

| Rework | $76,000 | $75,000 | $1,000 | U |

| Plate revisions | $58,000 | $55,000 | $3,000 | U |

| Press downtime | $102,000 | $100,000 | $2,000 | U |

| Waste | $ 136,000 | $130,000 | $ 6,000 | U |

| Total failure costs | $537,000 | $510,000 | $27,000 | U |

| Total quality costs | $1,399,000 | $1,320,000 | $79,000 | U |

Table (1)

Every single category and each individual item are equivalent to or higher than the budgeted amounts. Therefore, the firm cannot achieve its budgeted goals for the year.

2.

Prepare a one-period quality performance report for 20x5 that compares the actual quality costs of 20x4 with the actual costs of 20x5 and state the amount of change in profit due to improvement in quality.

Explanation of Solution

Prepare a one-period quality performance report for 20x5:

| Company I | ||||

| Performance Report: Quality Costs | ||||

| One-Year Trend | ||||

| For the Year Ended December 31, 20x5 | ||||

| Particulars |

Actual Costs 20x5 (a) |

Actual Costs 20x4 (b) |

Variance | |

| Prevention costs: | ||||

| Fixed: | ||||

| Quality planning | $150,000 | $140,000 | ($10,000) | U |

| Quality training | $20,000 | $20,000 | $0 | |

| Quality improvement | $100,000 | $120,000 | $20,000 | F |

| Quality reporting | $12,000 | $12,000 | $0 | |

| Total prevention costs | $282,000 | $292,000 | $10,000 | F |

| Appraisal costs: | ||||

| Variable: | ||||

| Proofreading | $520,000 | $580,000 | $60,000 | F |

| Other inspection | $60,000 | $80,000 | $20,000 | F |

| Total appraisal costs | $580,000 | $660,000 | $80,000 | F |

| Failure costs: | ||||

| Variable: | ||||

| Correction of typos | $165,000 | $200,000 | $35,000 | F |

| Rework | $76,000 | $131,000 | $55,000 | F |

| Plate revisions | $58,000 | $83,000 | $25,000 | F |

| Press downtime | $102,000 | $123,000 | $21,000 | F |

| Waste | $ 136,000 | $191,000 | $ 55,000 | F |

| Total failure costs | $537,000 | $728,000 | $191,000 | F |

| Total quality costs | $1,399,000 | $1,680,000 | $281,000 | F |

Table (2)

- The quality cost reduced from 20x4 to 20x5; therefore, the profit increased to $281,000. There is still considerable improvement even though the budgeted reductions for the year are not met.

- Additionally, the improvement was due to the “reduction of failure costs” which is a positive sign denoting that quality is certainly increasing.

3.

Prepare a graph that shows the trend in total quality costs as a percentage of sales since the inception of the quality improvement program.

Explanation of Solution

Multiple-period quality trend reports: Multiple-period quality trend reports is a chart or graph that tracks the change in quality from the starting of the program to the present.

Prepare a graph:

Figure (1)

Working notes:

(1)Calculate the percent of sales:

| Year |

Quality Costs (a) |

Sales Revenues (b) |

Percent of sales |

| 20x1 | $2,000,000 | $10,000,000 | 20% |

| 20x2 | $1,800,000 | $10,000,000 | 18% |

| 20x3 | $1,815,000 | $11,000,000 | 16.5% |

| 20x4 | $1,680,000 | $12,000,000 | 14% |

| 20x5 | $1,320,000 | $12,000,000 | 11.65% |

Table (3)

4.

Prepare a graph that shows the trend for all four quality cost categories for 20x1 through 20x5 and state the manner in which the graphs helps management to know that the reduction in total quality costs is attributable to quality improvement.

Explanation of Solution

Prepare a graph:

Figure (2)

“Increases in prevention and appraisal costs” along with simultaneous decrease in failure costs are good indication that in general quality is increasing. It is to be noted, that decreases in external failure costs are mostly difficult to attain without increase in actual quality.

5.

Prepare a long-range quality cost performance report.

Explanation of Solution

Long-range performance report: Long-range performance report compares the “current actual” with the costs that will be allowed if the “zero-defects standard” is being met by assuming that sales level is equal to that of the existing period.

Prepare a long-range quality cost performance report:

| Company I | ||||

| Performance Report: Quality Costs | ||||

| One-Year Trend | ||||

| For the Year Ended December 31, 20x5 | ||||

| Particulars |

Actual Costs 20x5 (a) |

Long-Range Target Costs (b) |

Variance | |

| Prevention costs: | ||||

| Fixed: | ||||

| Quality planning | $150,000 | $0 | $150,000 | U |

| Quality training | $20,000 | (9)$112,500 | ($92,500) | F |

| Quality improvement | $100,000 | $0 | $100,000 | U |

| Quality reporting | $12,000 | (10)$26,250 | ( $14,250) | F |

| Total prevention costs | $282,000 | $138,750 | $143,250 | U |

| Appraisal costs: | ||||

| Variable: | ||||

| Proofreading | (2)$650,000 | (11)$187,500 | $462,500 | U |

| Other inspection | (3) $75,000 | (12)$48,750 | $26,250 | U |

| Total appraisal costs | $725,000 | $236,250 | $488,750 | U |

| Failure costs: | ||||

| Variable: | ||||

| Correction of typos | (4)$206,250 | $0 | $206,250 | U |

| Rework | (5)$95,000 | $0 | $95,000 | U |

| Plate revisions | (6)$72,500 | $0 | $72,500 | U |

| Press downtime | (7)$127,500 | $0 | $127,500 | U |

| Waste | (8) $170,000 | $0 | $170,000 | U |

| Total failure costs | $671,250 | $0 | $671,250 | U |

| Total quality costs | $1,678,250 | $375,000 | $1,303,250 | U |

Table (4)

Note: Apart from for prevention costs, which is a fixed cost, actual costs of 20x5, are adjusted to a sales level of $15 million.

Workings notes:

(2)Calculate the proofreading costs:

(3)Calculate the other inspection costs:

(4)Calculate the correction of typos costs:

(5)Calculate the rework costs:

(6)Calculate the plate revision costs:

(7)Calculate the press downtime costs:

(8)Calculate the cost of waste:

(9)Calculate the long-range target costs for quality training:

(10)Calculate the long-range target costs for quality reporting:

(11)Calculate the long-range target costs for proofreading:

(12)Calculate the long-range target costs for other inspection:

(13)Calculate the amount of total quality costs:

Want to see more full solutions like this?

Chapter 14 Solutions

Cornerstones of Cost Management (Cornerstones Series)

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning

Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning