Concept explainers

Videos

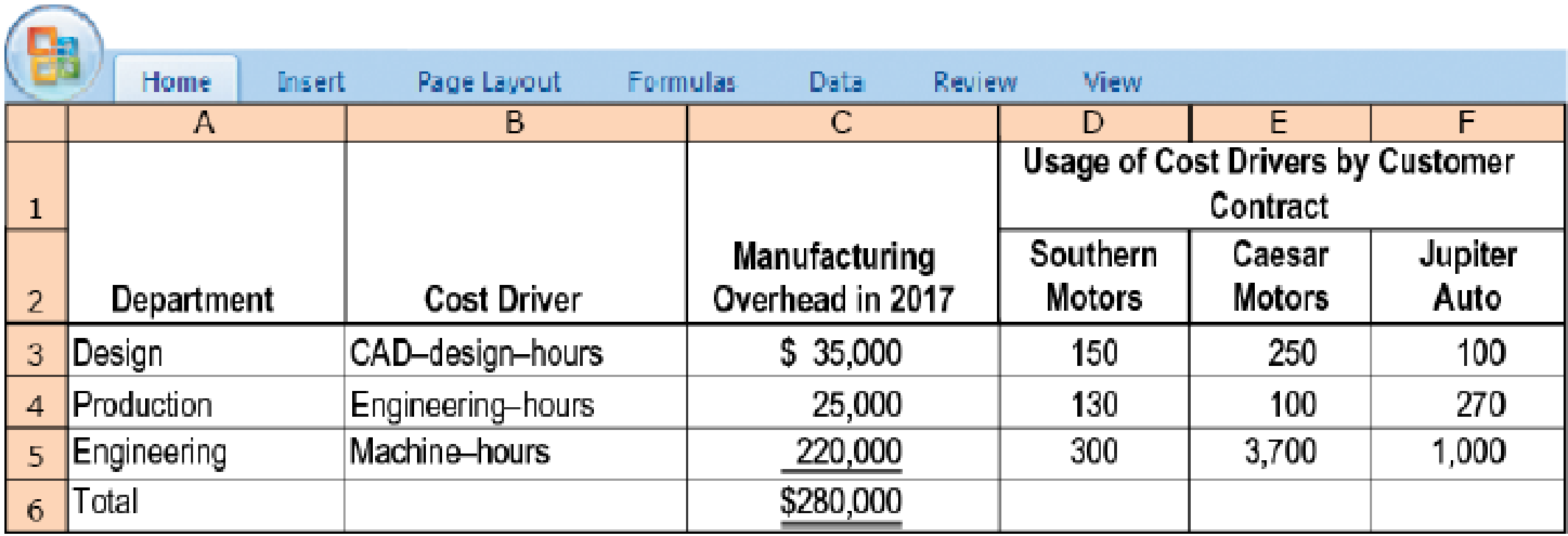

Plant-wide, department, and ABC Indirect cost rates. Roadster Company (RC) designs and produces automotive parts. In 2017, actual variable manufacturing

- 1. Compute the manufacturing overhead allocated to each customer in 2017 using the simple costing system that uses machine-hours as the allocation base.

Required

- 2. Compute the manufacturing overhead allocated to each customer in 2017 using department-based manufacturing overhead rates.

- 3. Comment on your answers in requirements 1 and 2. Which customer do you think was complaining about being overcharged in the simple system? If the new department-based rates are used to price contracts, which customer(s) will be unhappy? How would you respond to these concerns?

- 4. How else might RC use the information available from its department-by-department analysis of

manufacturing overhead costs ? - 5. RC’s managers are wondering if they should further refine the department-by-department costing system into an ABC system by identifying different activities within each department. Under what conditions would it not be worthwhile to further refine the department costing system into an ABC system?

Learn your wayIncludes step-by-step video

Chapter 5 Solutions

Horngren's Cost Accounting: A Managerial Emphasis (16th Edition)

Additional Business Textbook Solutions

Horngren's Cost Accounting: A Managerial Emphasis (16th Edition)

Operations Management

Operations Management

Corporate Finance (4th Edition) (Pearson Series in Finance) - Standalone book

Financial Accounting: Tools for Business Decision Making, 8th Edition

Intermediate Accounting (2nd Edition)

- The accounting equation helps keep financial records balanced. It shows that a company's assets are always equal to its liabilities plus stockholders' equity (Assets = Liabilities + Equity). This equation helps track how money moves in and out of a business. When a company buys or sells something, the equation makes sure everything is recorded correctly. Respond to the above paragrapharrow_forwardWhat is the role of the accounting equation in the analysis of business transactions?arrow_forwardExplain how this theory can help individuals in at least two fields (business, medical, education, etc.) better work in intercultural settings. Define the theory based on credible sources. Discuss the development of the theory: how it originated and came to its current status. Evaluate your scholarly sources, providing a brief comment on the theoretical aspects of each. Discuss the link(s) between your chosen theory and career field. Discuss the implications of your case on individuals, society, and the public. How does an increased intercultural understanding affect these different groups? In 8-10 pages in length. The paper should include support for the topic, your analyses and position(s) by citing course readings, and include at least five credible sources that you chose for your annotated bibliography. A credible source is defined as: a scholarly or peer-reviewed journal articlearrow_forward

- In a fully integrated standard costing system standards costs eventually flow into the: a. cost of goods sold account b. standard cost account c. selling and administrative expenses account d. sales accountarrow_forwardNet sales total $438,000. Beginning and ending accounts receivable are $35,000 and $37,000, respectively. Calculate days' sales in receivables. A.27 days B.30 days C.36 days D.31 daysarrow_forwardProvide correct answerarrow_forward

- For the system shown in figure below, the per unit values of different quantities are E-1.2, V 1, X X2-0.4. Xa-0.2 Determine whether the system is stable for a sustained fault. The fault is cleared at 8-60°. Is the system stable? If so find the maximum rotor swing. Find the critical clearing angle. E25 G X'd 08 CB X2 F CB V28 Infinite busarrow_forwardGeisner Inc. has total assets of $1,000,000 and total liabilities of $600,000. The industry average debt-to-equity ratio is 1.20. Calculate Geisner's debt-to-equity ratio and indicate whether the company's default risk is higher or lower than the average of other companies in the industry.arrow_forwardHy expert give me solution this questionarrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning