Concept explainers

Videos

Paul Golding and his wife, Nancy, established Crunchy Chips in 1938. Over the past 60 years, the company has established distribution channels in 11 western states, with production facilities in Utah, New Mexico, and Colorado. In 1980, Paul’s son, Edward, took control of the business. By 2017, it was clear that the company’s plants needed to gain better control over production costs to stay competitive. Edward hired a consultant to install a

The manufacturing process for potato chips begins when the potatoes are placed into a large vat in which they are automatically washed. After washing, the potatoes flow directly to an automatic peeler. The peeled potatoes then pass by inspectors, who manually cut out deep eyes or other blemishes. After inspection, the potatoes are automatically sliced and dropped into the cooking oil. The frying process is closely monitored by an employee. After the chips are cooked, they pass under a salting device and then pass by more inspectors, who sort out the unacceptable finished chips (those that are discolored or too small). The chips then continue on the conveyor belt to a bagging machine that bags them in 1-pound bags. After bagging, the bags are placed in a box and shipped. The box holds 15 bags.

The raw potato pieces (eyes and blemishes), peelings, and rejected finished chips are sold to animal feed producers for $0.16 per pound. The company uses this revenue to reduce the cost of potatoes. We would like this reflected in the price standard relating to potatoes.

Crunchy Chips purchases high-quality potatoes at a cost of $0.245 per pound. Each potato averages 4.25 ounces. Under efficient operating conditions, it takes four potatoes to produce one 16-ounce bag of plain chips. Although we label bags as containing 16 ounces, we actually place 16.3 ounces in each bag. We plan to continue this policy to ensure customer satisfaction. In addition to potatoes, other raw materials are the cooking oil, salt, bags, and boxes. Cooking oil costs $0.04 per ounce, and we use 3.3 ounces of oil per bag of chips. The cost of salt is so small that we add it to

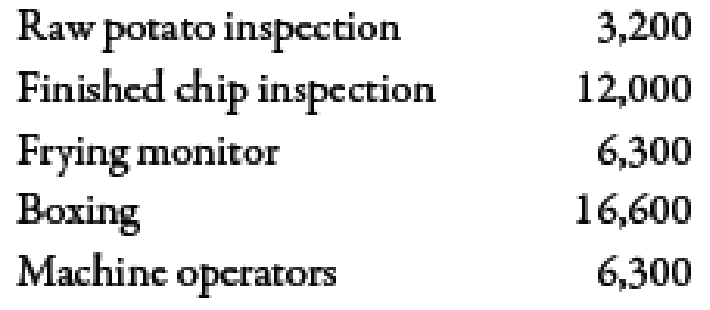

Our plant produces 8.8 million bags of chips per year. A recent engineering study revealed that we would need the following direct labor hours to produce this quantity if our plant operates at peak efficiency:

I’m not sure that we can achieve the level of efficiency advocated by the study. In my opinion, the plant is operating efficiently for the level of output indicated if the hours allowed are about 10% higher.

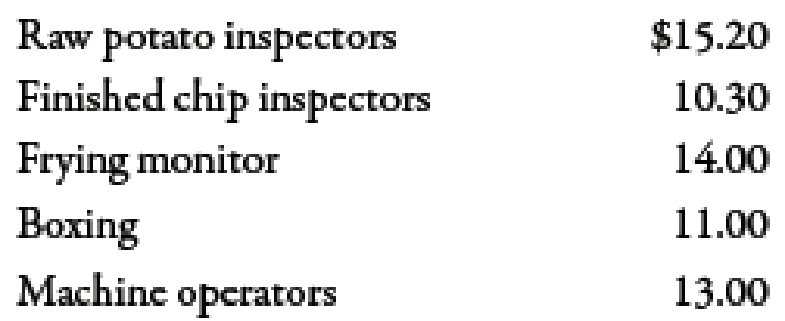

The hourly labor rates agreed upon with the union are:

Overhead is applied on the basis of direct labor dollars. We have found that variable overhead averages about 116% of our direct labor cost. Our fixed overhead is budgeted at $1,135,216 for the coming year.

Required:

- 1. Discuss the benefits of a standard costing system for Crunchy Chips.

- 2. Discuss the president’s concern about using the result of the engineering study to set the labor standards. What standard would you recommend?

- 3. Form a group with two or three other students. Develop a standard cost sheet for Crunchy Chips’ plain potato chips. Round all computations to four decimal places.

- 4. Suppose that the level of production was 8.8 million bags of potato chips for the year as planned. If 9.5 million pounds of potatoes were used, compute the materials usage variance for potatoes.

1.

Explain the benefits of a standard costing for Company CC.

Explanation of Solution

Variance:

The amount obtained when actual cost is deducted from budgeted cost is known as variance. Variance is calculated to find whether the cost is over applied or under applied.

The benefits of standard costing system for Company CC are explained below:

- Company CC is able to increase the control of its manufacturing inputs by using the standard costing.

- Company CC is able to evaluate the price and usage variances with the help of the price and quantity variances.

- Company CC is able to enhance its information by using the standard costing.

2.

Explain the concern of president about using the result of the engineering study to set the labor standards. Also, identify the best standard for the company.

Explanation of Solution

The concern of president is that whether the company is able to achieve its labor standards or not. If company is giving pressure on its workers for achieving the perfect standards, then it gives negative impact on the production of the workers. As a result, the outcome of the work of the workers is negative or unsatisfactory because workers get irritated and lower their performance. The best standard for the company is ideal standard because ideal standard is the most desired, highest quality or best standard that could easily achieve.

3.

Prepare a standard cost sheet for Company CC.

Explanation of Solution

Standard cost sheet for one box of chips:

| Particulars |

Quantity (Q) |

Price (P) ($) |

Amount ($) |

| Direct materials | |||

| Potatoes | 15.93751 | 0.238 | 3.7931 |

| Cooking oil | 49.5 | 0.04 | 1.9800 |

| Bags | 15 | 0.11 | 1.6500 |

| Boxes | 1 | 0.52 | 0.5200 |

| Total | 7.9431 |

Table (1)

Standard cost sheet of direct labor:

| Particulars |

Quantity (Q) |

Price (P) ($) |

Amount ($) |

| Direct labor | |||

| Potato inspection | 0.0062 | 15.20 | 0.0912 |

| Chip inspection | 0.02253 | 10.30 | 0.2318 |

| Frying monitor | 0.01184 | 14.00 | 0.1652 |

| Boxing | 0.03115 | 11.00 | 0.3421 |

| Machine operators | 0.01186 | 13.00 | 0.1534 |

| Variable overhead | 0.9837 | 1.16 | 1.1411 |

| Fixed overhead | 0.9837 | 1.96717 | 1.9350 |

| Direct material | 7.9431 | ||

| Total(A) | 12.0029 | ||

| Units of bags(B) | 15 | ||

|

Cost per bag | 0.8002 |

Table (2)

Working Note:

1.

Calculation of quantity of potatoes:

2.

Calcualtion of hours of potato inspection:

For calcualting the hours of potato inspection, first need to calculate the number of boxes per hour:

3.

Calcualtion of hours of Chips inspection:

4.

Calcualtion of hours of frying monitor:

5.

Calcualtion of hours of boxing:

6.

Calcualtion of hours of machine operators:

7.

Calculation of Fixed overhead rate:

4.

Calculate the material usage variances for potatoes.

Explanation of Solution

Use the following formula to calculate material usage variance of potato:

Substitute $9,500,000 for actual quantity, $9,350,000 for standard quantity and $0.238 for standard price in the above formula.

Therefore, the material usage variance is $37,500 (U).

Working Note:

1.

Calculation of standard quantity:

Want to see more full solutions like this?

Chapter 10 Solutions

Managerial Accounting: The Cornerstone of Business Decision-Making

- During the year, Company A had sales of $2,400,000. The cost of goods sold, and depreciation expense were $1,860,000 and $490,000 respectively. The company had a net interest expense of $215,000 and a tax rate of 35%. What is Company A's net income?arrow_forwardThe carrying amount of the trademarks on 30 june 2018, is:arrow_forwardI want to correct answer general accountingarrow_forward

- Do fast answer of this accounting questionsarrow_forward??arrow_forwarda. Determine the following variances for November. Note: Do not use negative signs with your answers. a. Total material price variance b. Total material usage (quantity) variance c. Labor rate variance d. Labor efficiency variance e. Variable overhead spending variance f. Variable overhead efficiency variance g. Fixed overhead spending variance h. Volume variance i. Budget variance cost accountingarrow_forward

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,