Managerial Accounting

7th Edition

ISBN: 9781337116008

Author: Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher: South Western Educational Publishing

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 10, Problem 70P

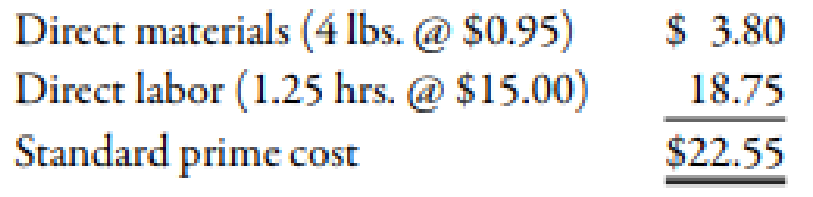

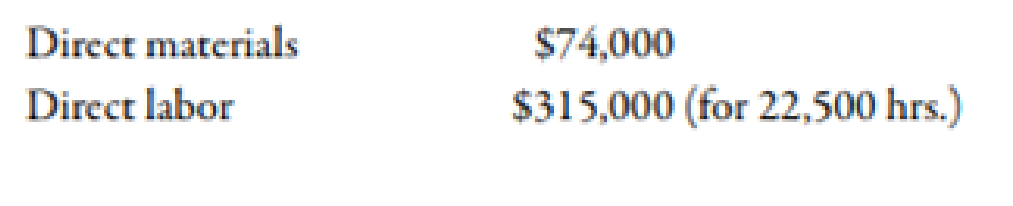

Botella Company produces plastic bottles. The unit for costing purposes is a case of 18 bottles. The following standards for producing one case of bottles have been established:

During December, 78,000 pounds of materials were purchased and used in production. There were 15,000 cases produced, with the following actual prime costs:

Required:

- 1. Compute the materials variances.

- 2. Compute the labor variances.

- 3. CONCEPTUAL CONNECTION What are the advantages and disadvantages that can result from the use of a

standard costing system?

Expert Solution & Answer

Trending nowThis is a popular solution!

Students have asked these similar questions

Huron Company produces a commercial cleaning compound known as Zoom. The direct materials and direct labor standards for one unit of Zoom are given below: Standard quantity or hours of direct materials: 7.40 pounds, standard price or rate of direct materials is 2.60 per pound. Standard cost of direct materials is 19.24. Standard quality or hours of direct labor is 0.45. Standard price or rate of direct labor is 8.00 per pound. Standard cost is 3.60. During the most recent month, the following activity was recorded: 12,100 pounds of material were purchased at a cost of 2.50 per pound. All of the material purchased was used to produce 1,500 units of the product. 575 hours of direct labor time were recorded at a total labor cost of 5,750. Compute the materials price variance and the materials quantity variance for the month. Complete the labor rate variance and efficiency variance for the month.

1. Complete the standard cost card for each product, showing the standard cost of direct materials and direct labor.

2. Compute the materials price and quantity variances for each material.

3. Compute the labor rate and efficiency variances for each operation.

The controller of Ferrence Company estimates the amount of materials handling overhead cost that should be allocated to the company's two products using the data that are given below:

The total materials handling cost for the year is expected to be $16,486.40.

If the materials handling cost is allocated on the basis of material moves, how much of the total materials handling cost should be allocated to the specialty windows? (Round off your answer to the nearest whole dollar.)

Question 12 options:

$3,266

$9,274

$8,243

$6,595

Chapter 10 Solutions

Managerial Accounting

Ch. 10 - Discuss the dirrerence between budgets and...Ch. 10 - Describe the relationship that unit standards have...Ch. 10 - Why is historical experience often a poor basis...Ch. 10 - Prob. 4DQCh. 10 - Explain why standard costing systems adopted.Ch. 10 - How does standard costing improve the control...Ch. 10 - Discuss the differences among actual costing,...Ch. 10 - Prob. 8DQCh. 10 - The budget variance for variable production costs...Ch. 10 - When should a standard cost variance be...

Ch. 10 - What are control limits, and how are they set?Ch. 10 - Explain why the materials price variance is often...Ch. 10 - The materials usage variance is always the...Ch. 10 - The labor rate variance is never controllable. Do...Ch. 10 - Prob. 15DQCh. 10 - What is kaizen costing? On which part of the value...Ch. 10 - What is target costing? Describe how costs are...Ch. 10 - Prob. 18DQCh. 10 - The variable overhead efficiency variance has...Ch. 10 - Describe the difference between the variable...Ch. 10 - What is the cause of an unfavorable volume...Ch. 10 - Does the volume variance convey any meaningful...Ch. 10 - Which do you think is more important for control...Ch. 10 - Prob. 1MCQCh. 10 - A currently attainable standard is one that a....Ch. 10 - An ideal standard is one that a. uses only...Ch. 10 - The underlying details for the standard cost per...Ch. 10 - The standard quantity of materials allowed is...Ch. 10 - The standard direct labor hours allowed is...Ch. 10 - Investigating variances from standard is a. always...Ch. 10 - Prob. 8MCQCh. 10 - The materials price variance is usually computed...Ch. 10 - Responsibility for the materials usage variance is...Ch. 10 - Responsibility for the labor rate variance...Ch. 10 - Responsibility for the labor efficiency variance...Ch. 10 - (Appendix 10A) Which of the following items...Ch. 10 - (Appendix 10A) Which of the following is true...Ch. 10 - The total variable overhead variance is the...Ch. 10 - A variable overhead spending variance can occur...Ch. 10 - The total variable overhead variance can be...Ch. 10 - The total fixed overhead variance is a. the...Ch. 10 - The total fixed overhead variance can be expressed...Ch. 10 - An unfavorable volume variance can occur because...Ch. 10 - Prob. 21BEACh. 10 - Control Limits During the last 6 weeks, the actual...Ch. 10 - Use the following information to complete Brief...Ch. 10 - Use the following information to complete Brief...Ch. 10 - Use the following information to complete Brief...Ch. 10 - Use the following information to complete Brief...Ch. 10 - Rath Company showed the following information for...Ch. 10 - Variable Overhead Spending and Efficiency...Ch. 10 - Performance Report for Variable Variances Humo...Ch. 10 - Total Fixed Overhead Variance Bradshaw Company...Ch. 10 - Fixed Overhead Spending and Volume Variances,...Ch. 10 - Prob. 32BEBCh. 10 - Control Limits During the last 6 weeks, the actual...Ch. 10 - Prob. 34BEBCh. 10 - Use the following information to complete Brief...Ch. 10 - Use the following information to complete Brief...Ch. 10 - Use the following information to complete Brief...Ch. 10 - Mulliner Company showed the following information...Ch. 10 - Variable Overhead Spending and Efficiency...Ch. 10 - Performance Report for Variable Variances Potter...Ch. 10 - Bulger Company provided the following data:...Ch. 10 - Fixed Overhead Spending and Volume Variances,...Ch. 10 - Standard Quantities of Labor and Materials...Ch. 10 - Sommers Company uses the following rule to...Ch. 10 - Use the following information for Exercises 10-45...Ch. 10 - Refer to the information for Cinturon Corporation...Ch. 10 - Refer to the information for Cinturon Corporation...Ch. 10 - Materials Variances Manzana Company produces apple...Ch. 10 - Labor Variances Verde Company produces wheels for...Ch. 10 - At the beginning of the year, Craig Company had...Ch. 10 - Jackie Iverson was furious. She was about ready to...Ch. 10 - 10-52 Materials and Labor Variances Refer to the...Ch. 10 - Refer to the information for Deporte Company...Ch. 10 - Esteban Products produces instructional aids,...Ch. 10 - Escuchar Products, a producer of DVD players, has...Ch. 10 - Use the following information for Exercises 10-56...Ch. 10 - Refer to the information for Rostand Inc. above....Ch. 10 - At the beginning of the year, Lopez Company had...Ch. 10 - Zepol Company is planning to produce 600,000 power...Ch. 10 - Last year, Gladner Company had planned to produce...Ch. 10 - Anker Company had the data below for its most...Ch. 10 - Cabanarama Inc. designs and manufactures...Ch. 10 - Basuras Waste Disposal Company has a long-term...Ch. 10 - Tom Belford and Tony Sorrentino own a small...Ch. 10 - Mantenga Company provides routine maintenance...Ch. 10 - Buenolorl Company produces a well-known cologne....Ch. 10 - The management of Golding Company has determined...Ch. 10 - Phono Company manufactures a plastic toy cell...Ch. 10 - Botella Company produces plastic bottles. The unit...Ch. 10 - The Lubbock plant of Morrils Small Motor Division...Ch. 10 - Moleno Company produces a single product and uses...Ch. 10 - The Lubbock plant of Morrils Small Motor Division...Ch. 10 - Extrim Company produces monitors. Extrims plant in...Ch. 10 - Lynwood Company produces surge protectors. To help...Ch. 10 - Shumaker Company manufactures a line of high-top...Ch. 10 - Paul Golding and his wife, Nancy, established...Ch. 10 - Prob. 79CCh. 10 - Prob. 1MTCCh. 10 - The Two Cost Systems Sacred Heart Hospital (SHH)...Ch. 10 - Prob. 3MTCCh. 10 - Prob. 4MTCCh. 10 - The Two Cost Systems Sacred Heart Hospital (SHH)...Ch. 10 - Prob. 6MTCCh. 10 - Prob. 7MTCCh. 10 - Prob. 8MTCCh. 10 - Prob. 9MTCCh. 10 - Sacred Heart Hospital (SHH) faces skyrocketing...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Evans, Inc., has a unit-based costing system. Evanss Miami plant produces 10 different electronic products. The demand for each product is about the same. Although they differ in complexity, each product uses about the same labor time and materials. The plant has used direct labor hours for years to assign overhead to products. To help design engineers understand the assumed cost relationships, the Cost Accounting Department developed the following cost equation. (The equation describes the relationship between total manufacturing costs and direct labor hours; the equation is supported by a coefficient of determination of 60 percent.) Y=5,000,000+30X,whereX=directlaborhours The variable rate of 30 is broken down as follows: Because of competitive pressures, product engineering was given the charge to redesign products to reduce the total cost of manufacturing. Using the above cost relationships, product engineering adopted the strategy of redesigning to reduce direct labor content. As each design was completed, an engineering change order was cut, triggering a series of events such as design approval, vendor selection, bill of materials update, redrawing of schematic, test runs, changes in setup procedures, development of new inspection procedures, and so on. After one year of design changes, the normal volume of direct labor was reduced from 250,000 hours to 200,000 hours, with the same number of products being produced. Although each product differs in its labor content, the redesign efforts reduced the labor content for all products. On average, the labor content per unit of product dropped from 1.25 hours per unit to one hour per unit. Fixed overhead, however, increased from 5,000,000 to 6,600,000 per year. Suppose that a consultant was hired to explain the increase in fixed overhead costs. The consultants study revealed that the 30 per hour rate captured the unit-level variable costs; however, the cost behavior of other activities was quite different. For example, setting up equipment is a step-fixed cost, where each step is 2,000 setup hours, costing 90,000. The study also revealed that the cost of receiving goods is a function of the number of different components. This activity has a variable cost of 2,000 per component type and a fixed cost that follows a step-cost pattern. The step is defined by 20 components with a cost of 50,000 per step. Assume also that the consultant indicated that the design adopted by the engineers increased the demand for setups from 20,000 setup hours to 40,000 setup hours and the number of different components from 100 to 250. The demand for other non-unit-level activities remained unchanged. The consultant also recommended that management take a look at a rejected design for its products. This rejected design increased direct labor content from 250,000 hours to 260,000 hours, decreased the demand for setups from 20,000 hours to 10,000 hours, and decreased the demand for purchasing from 100 component types to 75 component types, while the demand for all other activities remained unchanged. Required: 1. Using normal volume, compute the manufacturing cost per labor hour before the year of design changes. What is the cost per unit of an average product? 2. Using normal volume after the one year of design changes, compute the manufacturing cost per hour. What is the cost per unit of an average product? 3. Before considering the consultants study, what do you think is the most likely explanation for the failure of the design changes to reduce manufacturing costs? Now use the information from the consultants study to explain the increase in the average cost per unit of product. What changes would you suggest to improve Evanss efforts to reduce costs? 4. Explain why the consultant recommended a second look at a rejected design. Provide computational support. What does this tell you about the strategic importance of cost management?arrow_forwardLarsen, Inc., produces two types of electronic parts and has provided the following data: There are four activities: machining, setting up, testing, and purchasing. Required: 1. Calculate the activity consumption ratios for each product. 2. Calculate the consumption ratios for the plantwide rate (direct labor hours). When compared with the activity ratios, what can you say about the relative accuracy of a plantwide rate? Which product is undercosted? 3. What if the machine hours were used for the plantwide rate? Would this remove the cost distortion of a plantwide rate?arrow_forwardSilven Company has identified the following overhead activities, costs, and activity drivers for the coming year: Silven produces two models of cell phones with the following expected activity demands: 1. Determine the total overhead assigned to each product using the four activity drivers. 2. Determine the total overhead assigned to each model using the two most expensive activities. The costs of the two relatively inexpensive activities are allocated to the two expensive activities in proportion to their costs. 3. Using ABC as the benchmark, calculate the percentage error and comment on the accuracy of the reduced system. Explain why this approach may be desirable.arrow_forward

- Box Springs. Inc., makes two sizes of box springs: queen and king. The direct material for the queen is $35 per unit and $55 is used in direct labor, while the direct material for the king is $55 per unit, and the labor cost is $70 per unit. Box Springs estimates it will make 4,300 queens and 3,000 kings in the next year. It estimates the overhead for each cost pool and cost driver activities as follows: How much does each unit cost to manufacture?arrow_forwardPatterson Company produces wafers for integrated circuits. Data for the most recent year are provided: aCalculated using number of dies as the single unit-level driver. bCalculated by multiplying the consumption ratio of each product by the cost of each activity. Required: 1. Using the five most expensive activities, calculate the overhead cost assigned to each product. Assume that the costs of the other activities are assigned in proportion to the cost of the five activities. 2. Calculate the error relative to the fully specified ABC product cost and comment on the outcome. 3. What if activities 1, 2, 5, and 8 each had a cost of 650,000 and the remaining activities had a cost of 50,000? Calculate the cost assigned to Wafer A by a fully specified ABC system and then by an approximately relevant ABC approach. Comment on the implications for the approximately relevant approach.arrow_forwardMedical Tape makes two products: Generic and Label. It estimates it will produce 423,694 units of Generic and 652,200 of Label, and the overhead for each of its cost pools is as follows: It has also estimated the activities for each cost driver as follows: How much is the overhead allocated to each unit of Generic and Label?arrow_forward

- The controller of the South Charleston plant of Ravinia, Inc., monitored activities associated with materials handling costs. The high and low levels of resource usage occurred in September and March for three different resources associated with materials handling. The number of moves is the driver. The total costs of the three resources and the activity output, as measured by moves for the two different levels, are presented as follows: Required: 1. Determine the cost behavior formula of each resource. Use the high-low method to assess the fixed and variable components. 2. Using your knowledge of cost behavior, predict the cost of each item for an activity output level of 9,000 moves. 3. Construct a cost formula that can be used to predict the total cost of the three resources combined. Using this formula, predict the total materials handling cost if activity output is 9,000 moves. In general, when can cost formulas be combined to form a single cost formula?arrow_forwardJameson Company produces paper towels. The company has established the following direct materials and direct labor standards for one case of paper towels: During the first quarter of the year, Jameson produced 45,000 cases of paper towels. The company purchased and used 135,700 pounds of paper pulp at 0.38 per pound. Actual direct labor used was 91,000 hours at 12.10 per hour. Required: 1. Calculate the direct materials price and usage variances. 2. Calculate the direct labor rate and efficiency variances. 3. Prepare the journal entries for the direct materials and direct labor variances. 4. Describe how flexible budgeting variances relate to the direct materials and direct labor variances computed in Requirements 1 and 2.arrow_forwardApril Industries employs a standard costing system in the manufacturing of its sole product, a park bench. They purchased 60,000 feet of raw material for $300,000, and it takes S feet of raw materials to produce one park bench. In August, the company produced 10,000 park benches. The standard cost for material output was $100,000, and there was an unfavorable direct materials quantity variance of $6,000. A. What is April Industries standard price for one unit of material? B. What was the total number of units of material used to produce the August output? C. What was the direct materials price variance for August?arrow_forward

- Koontz Company manufactures a number of products. The standards relating to one of these products are shown below, along with actual cost data for May. Direct materials: Standard: 1.80 feet at $2.20 per foot Actual: 1.75 feet at $2.40 per foot Direct labor: Standard: 0.90 hour at $14.00 per hour Actual: 0.95 hour at $13.40 per hour Variable overhead: Standard: 0.90 hour at $5.00 per hour Actual: 0.95 hour at $4.60 per hour Total cost per unit Excess of actual cost over standard cost per unit Required 1 Standard Cost per Unit $3.96 Required 2 12.60 Required 3 4.50 Complete this question by entering your answers in the tabs below. $ 21.06 1a. Materials price variance 1a. Materials quantity variance 1b. Labor rate variance 1b. Labor efficiency variance 1c. Variable overhead rate variance 1c. Variable overhead efficiency variance The production superintendent was pleased when he saw this report and commented: "This $0.24 excess cost is well within the 5 percent limit management has set for…arrow_forwardLast month, Bugsby Corporation purchased and used the same quantity of material in producing its product, speed bumps for traffic control. FE(Click the icon to view the table.) Complete the following table. (Round your answers to two decimal places.) Direct materials information Standard pounds per unit Standard price per pound Actual quantity purchased and used per unit Actual price paid for material per pound Direct materials price variance Direct materials quantity variance Total direct material variance Number of units produced $ $ $ $ Medium speed bump 10 1.00 1.80 1.280 U 400 F 200 S speed bump $ $ $ Large 1.50 12 2.30 2,880 U 2,430 U 300 Data table Direct materials information Standard pounds per unit. Standard price per pound.. Actual quantity purchased and used per unit Actual price paid for material per pound.. Direct materials price variance.. Direct materials quantity variance. Total direct material variance.. Number of units produced Print Medium speed Large speed bump…arrow_forwardMaxey & Sons manufactures two types of storage cabinets-Type A and Type B—and applies manufacturing overhead to all units at the rate of $140 per machine hour. Production information follows. Descriptions Anticipated volume (units) Direct-material cost per unit Direct-labor cost per unit Descriptions The controller, who is studying the use of activity-based costing, has determined that the firm's overhead can be identified with three activities: manufacturing setups, machine processing, and product shipping. Data on the number of setups, machine hours, and outgoing shipments, which are the activities' three respective cost drivers, follow. Setups Machine hours Outgoing shipments Туре А 160 56,000 200 Туре А 28,000 $38 43 Required 1 Required 2 Required 3 Туре В Unit manufacturing costs 120 78,750 150 The firm's total overhead of $18,865,000 is subdivided as follows: manufacturing setups, $4,116,000; machine processing, $11,319,000 and product shipping, $3,430,000. Required: 1. Compute…arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Managerial Accounting: The Cornerstone of Busines...

Accounting

ISBN:9781337115773

Author:Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...

Accounting

ISBN:9781305970663

Author:Don R. Hansen, Maryanne M. Mowen

Publisher:Cengage Learning

Principles of Accounting Volume 2

Accounting

ISBN:9781947172609

Author:OpenStax

Publisher:OpenStax College

What is variance analysis?; Author: Corporate finance institute;https://www.youtube.com/watch?v=SMTa1lZu7Qw;License: Standard YouTube License, CC-BY