Concept explainers

Videos

Inventory Costing Methods

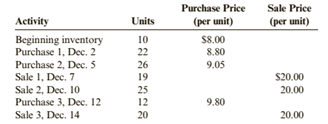

Anderson’s Department Store has the following data for inventory, purchases, and sales of merchandise for December.

Anderson’s uses a perpetual inventory system. All purchases and sales were for cash.

Required:

1. Compute cost of goods sold and the cost of ending inventory using FIFO.

2. Compute cost of goods sold and the cost of ending inventory using LIFO.

3. Compute cost of goods sold and the cost of ending inventory using the average cost method. ( Note: Use four decimal places for per-unit calculations.)

4. Prepare the

5. CONCEPTUAL CONNECTION Which method would result in the lowest amount paid for taxes?

(a)

Inventory costing methods:

FIFO, LIFO and average cost method, are those method which used for calculation of closing inventory and cost of goods sold.

The cost of ending inventory and the cost of goods sold using the FIFO.

Answer to Problem 67APSA

| Particular | |

| Cost of goods sold | |

| Closing inventory value |

Explanation of Solution

The given information is as follows:

Total available units are:

Calculation of Closing Inventory as per FIFO Method:

Under this method, which material purchased first, issued first for production. However closing inventory includes last purchased materials in stock. Due to latest purchase in closing inventory, higher value of latest purchase effects cost of goods sold as lower and profit margin will be high.

| Closing inventory | Cost of Goods sold | |

| Total |

(b)

Inventory costing methods:

FIFO, LIFO and average cost method, are those method which used for calculation of closing inventory and cost of goods sold.

The cost of ending inventory and the cost of goods sold using the LIFO.

Answer to Problem 67APSA

| Particular | |

| Cost of goods sold | |

| Closing inventory value |

Explanation of Solution

The given information is as follows:

Total available units are:

Calculation of closing inventory as per LIFO Method:

Under this method, which material purchased last, issued first for production. However closing inventory includes earliest purchased material in stock. Due to earliest purchase material in stock, lower value of earliest purchased effects cost of goods sold as high and profit margin will be lower.

| Ending Inventory | Cost of Goods sold | |

| Total |

(c)

Inventory costing methods:

FIFO, LIFO and average cost method, are those method which used for calculation of closing inventory and cost of goods sold.

The cost of ending inventory and the cost of goods sold using the average cost method.

Answer to Problem 67APSA

| Particular | |

| Cost of goods sold | |

| Closing inventory value |

Explanation of Solution

The given information is as follows:

Total available units are:

Calculation of closing inventory as per weighted average method:

Under this method, average cost per unit of inventory is calculated and closing inventory value is to be calculated on that basis. Average cost of inventory is changed on purchase high or low. However we follow indirect method of average cost to calculate closing inventory.

As the fist two sales are done only from two purchases and beginning inventory and the third sale is done including all purchases. Hence, there will requirement of two average cost for computing the cost of goods sold.

| Closing inventory | Cost of Goods sold | |

| Total |

(d)

Inventory costing methods:

FIFO, LIFO and average cost method, are those method which used for calculation of closing inventory and cost of goods sold.

The journal entries for recording the transaction on the basis of FIFO method.

Answer to Problem 67APSA

The journal entries of recording sales and purchases of the company for the Anderson Department Store recorded properly as per FIFO basis is as follows:

On cash purchases:

| Date | Particular | Debit $ | Credit $ |

| Inventory |

|||

| Cash | |||

| (To record transportation cost) |

On cash purchases:

| Date | Particular | Debit $ | Credit $ |

| Inventory |

|||

| Cash | |||

| (To record purchase entry) |

On cash sales:

| Date | Particular | Debit $ | Credit $ |

| Cash |

|||

| Sales Revenue | |||

| (To record cash sales) |

After above sales, cost of goods sold computed on FIFO basis:

| Date | Particular | Debit $ | Credit $ |

| Cost of Goods sold |

|||

| Inventory | |||

| (To record cost of goods sold) |

On cash sales:

| Date | Particular | Debit $ | Credit $ |

| Cash |

|||

| Sales Revenue | |||

| (To record cash sales) |

After above sales, cost of goods sold computed on FIFO basis:

| Date | Particular | Debit $ | Credit $ |

| Cost of Goods sold |

|||

| Inventory | |||

| (To record cost of goods sold) |

On cash purchases:

| Date | Particular | Debit $ | Credit $ |

| Inventory |

|||

| Cash | |||

| (To record purchase entry) |

On cash sales:

| Date | Particular | Debit $ | Credit $ |

| Cash |

|||

| Sales Revenue | |||

| (To record cash sales) |

After above sales, cost of goods sold computed on FIFO basis:

| Date | Particular | Debit $ | Credit $ |

| Cost of Goods sold |

|||

| Inventory | |||

| (To record cost of goods sold) |

Explanation of Solution

On cash purchases:

| Date | Particular | Debit $ | Credit $ |

| Inventory |

|||

| Cash | |||

| (To record transportation cost) |

On cash purchases:

| Date | Particular | Debit $ | Credit $ |

| Inventory |

|||

| Cash | |||

| (To record purchase entry) |

On cash sales:

| Date | Particular | Debit $ | Credit $ |

| Cash |

|||

| Sales Revenue | |||

| (To record cash sales) |

After above sales, cost of goods sold computed on FIFO basis

| Date | Particular | Debit $ | Credit $ |

| Cost of Goods sold |

|||

| Inventory | |||

| (To record cost of goods sold) |

On cash sales:

| Date | Particular | Debit $ | Credit $ |

| Cash |

|||

| Sales Revenue | |||

| (To record cash sales) |

After above sales, cost of goods sold computed on FIFO basis

| Date | Particular | Debit $ | Credit $ |

| Cost of Goods sold |

|||

| Inventory | |||

| (To record cost of goods sold) |

On cash purchases:

| Date | Particular | Debit $ | Credit $ |

| Inventory |

|||

| Cash | |||

| (To record purchase entry) |

On cash sales:

| Date | Particular | Debit $ | Credit $ |

| Cash |

|||

| Sales Revenue | |||

| (To record cash sales) |

After above sales, cost of goods sold computed on FIFO basis

| Date | Particular | Debit $ | Credit $ |

| Cost of Goods sold |

|||

| Inventory | |||

| (To record cost of goods sold) |

(e)

Inventory costing methods:

FIFO, LIFO and average cost method, are those method which used for calculation of closing inventory and cost of goods sold.

The method for determining the lowest amount paid for tax.

Answer to Problem 67APSA

The cost of goods sold of LIFO method is higher and value of closing inventory is lower than other methods which mean LIFO method provides lowest tax expenses in all methods.

Explanation of Solution

Comparison of closing inventory and Cost of goods sold as per above three methods:

| Particular | |||

| Cost of goods sold | |||

| Closing inventory value |

According the evaluation of the above table, it can be concluded that the lowest tax paid is provided by the LIFO method as the expense of cost of goods sold is highest which makes the income low and lower closing value of inventory also makes the income lower. Thus, the LIFO is the required method.

Want to see more full solutions like this?

Chapter 6 Solutions

Cornerstones of Financial Accounting

- I need help finding the accurate solution to this general accounting problem with valid methods.arrow_forwardI am looking for help with this general accounting question using proper accounting standards.arrow_forwardCan you solve this financial accounting problem using appropriate financial principles?arrow_forward

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning