Concept explainers

Videos

Salem Electronics currently produces two products: a programmable calculator and a tape recorder. A recent marketing study indicated that consumers would react favorably to a radio with the Salem brand name. Owner Kenneth Booth was interested in the possibility. Before any commitment was made, however, Kenneth wanted to know what the incremental fixed costs would be and how many radios must be sold to cover these costs.

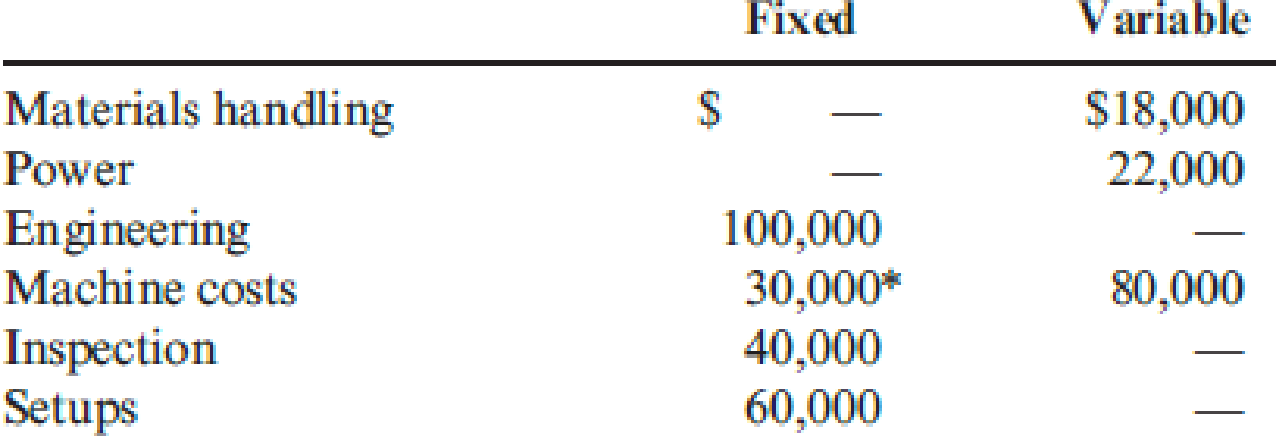

In response, Betty Johnson, the marketing manager, gathered data for the current products to help in projecting overhead costs for the new product. The overhead costs based on 30,000 direct labor hours follow. (The high-low method using direct labor hours as the independent variable was used to determine the fixed and variable costs.)

*All

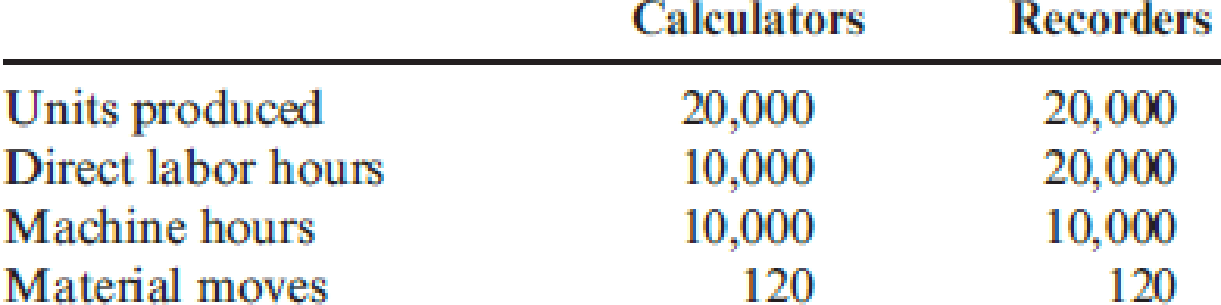

The following activity data were also gathered:

Betty was told that a plantwide overhead rate was used to assign overhead costs based on direct labor hours. She was also informed by engineering that if 20,000 radios were produced and sold (her projection based on her marketing study), they would have the same activity data as the recorders (use the same direct labor hours, machine hours, setups, and so on).

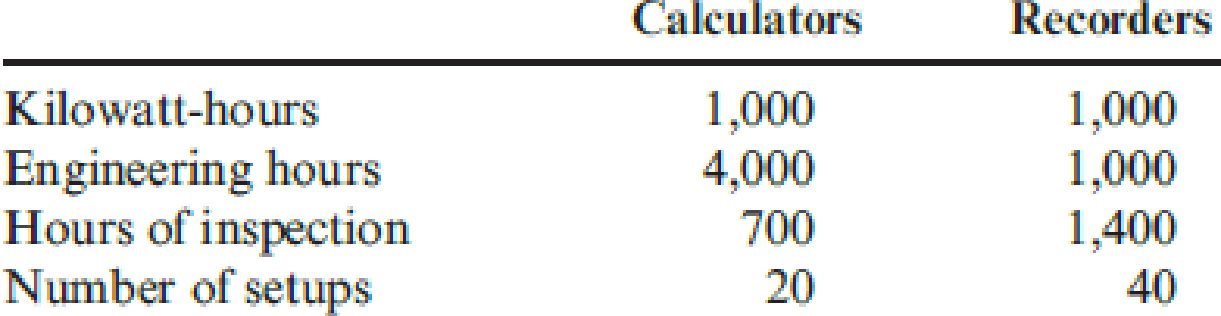

Engineering also provided the following additional estimates for the proposed product line:

Upon receiving these estimates, Betty did some quick calculations and became quite excited. With a selling price of $26 and just $18,000 of additional fixed costs, only 4,500 units had to be sold to break even. Since Betty was confident that 20,000 units could be sold, she was prepared to strongly recommend the new product line.

Required:

- 1. Reproduce Betty’s break-even calculation using conventional cost assignments. How much additional profit would be expected under this scenario, assuming that 20,000 radios are sold?

- 2. Use an activity-based costing approach, and calculate the break-even point and the incremental profit that would be earned on sales of 20,000 units.

- 3. Explain why the CVP analysis done in Requirement 2 is more accurate than the analysis done in Requirement 1. What recommendation would you make?

1.

Ascertain the break-even point and the additional profit for the given proposal.

Explanation of Solution

Contribution Margin Ratio: The contribution margin ratio shows the amount of difference in the actual sales value and the variable expenses in percentage. This margin indicates that percentage which is available for sale above the fixed costs and the profit. The formula for variable cost ratio is shown below:

Break-Even Point: The break-even point refers to the point of sales at which the firm neither earns a profit nor suffers a loss. It is also known as the point of sales or sales value at which the firm recovers the entire cost of fixed and variable nature.

Break-Even in sales revenue: The break-even in sales revenue refers to the sales volume required to cover the fixed and variable costs and left out with neither profit nor loss.

Compute the variable overhead rate:

The variable overhead rate per direct labor hour is $4.

Compute the unit variable cost:

The variable cost per unit is $22.

Compute the break-even units:

The break-even unit is 4,500 units.

Compute the additional profit:

The additional profit is $62,000.

2.

Compute the break-even point and the incremental profit using the activity based costing.

Explanation of Solution

Compute the unit-based variable overhead cost per unit:

| Particulars | Amount ($) |

| Unit-based variable costs: | |

| Materials handling | $18,000 |

| Power | $22,000 |

| Machine costs | $80,000 |

| Total | $120,000 |

| Machine hours | 20000 |

| Pool rate | $6 |

Table (1)

Compute the unit variable cost:

The unit-based variable overhead cost per unit is $21 (X1).

Compute the non-unit-based variable overhead cost per unit:

| Particulars | Calculations | Amount ($) |

| Non-unit-based variable costs: | ||

| Engineering (X2) | $20.00 | |

| Inspection (X3) | 19.05 | |

| Setups (X4) | $1,000 |

Table (2)

Compute the break-even units:

Substitute the values found in the below equation to compute the break-even point.

The break-even unit is 20,934 units.

The activity based costing is based on the assumptions that:

- The expected variable cost is realized.

- The depreciation is a fixed cost.

If the depreciation represents no salvage and the expected production is achieved, then the variable cost per unit will increase by $0.90

Compute the new break-even units:

The new break-even unit is 21,122 units.

3.

Describe the reasons for the greater accuracy of CVP analysis done in Requirement 2 than in the CVP analysis done in Requirement 1.

Explanation of Solution

Cost Volume Profit Analysis (CVP Analysis): The Cost volume profit (CVP) analysis is helpful in determining how any type of change in cost determines company’s income.

The reasons for differences in accuracy are:

- The Requirement 2 takes into consideration all the associated costs of the support activities which are ignored by the conventional method.

- The non-unit related costs are viewed as fixed costs in Requirement 1.

- Once these support activity costs are added the analysis tends to be more accurate.

Want to see more full solutions like this?

Chapter 16 Solutions

Cornerstones of Cost Management (Cornerstones Series)

- Hudson Corporation is considering three options for managing its data warehouse: continuing with its own staff, hiring an outside vendor to do the managing, or using a combination of its own staff and an outside vendor. The cost of the operation depends on future demand. The annual cost of each option (in thousands of dollars) depends on demand as follows: If the demand probabilities are 0.2, 0.5, and 0.3, which decision alternative will minimize the expected cost of the data warehouse? What is the expected annual cost associated with that recommendation? Construct a risk profile for the optimal decision in part (a). What is the probability of the cost exceeding $700,000?arrow_forwardAhlia Company, a nanufacturer of computer games, is in the process of introducing a new game to the narket and has nndertaken market research to find out abont customers' views on the valne of the product, as well as to obtain a conparison with competitors' products. The results of this research have been nsed to establish a target selling price of $80. This is the price that the company thinks it will have to sell the product at to achieve the required sales vohume, Cost estinmates have been prepared based on the proposed product specification. Manufacturing cost 2$ Direct material 4.25 Direct labour 23.08 Direct machinery costs 1.05 Ordering and receiving 0.28 Quality assurance 4.8 Non-manufacturing costs Marketing 8.19 Distribution 3.27 The target profit margin for the game is 45% of the target selling price. Instructions: Calculate the target cost of the new game and the target cost gap. %24arrow_forwardThe Chromosome Manufacturing Company produces two products, X and Y. The company president, Gene Mutation, is concerned about the fierce competition in the market for product X. He notes that competitors are selling X for a price well below Chromosome's price of P12.70. At the same time, he notes that competitors are pricing product Y almost twice as high as Chromosome's price of P12.50. Mr. Mutation has obtained the following data for a recent time period: PRODUCT X PRODUCT Y Number of Units 11,000 3,000 Direct Materials Cost Per Unit 3.23 3.09 Direct Labor Cost Per Unit 2.22 2.10 Direct Labor Hours 10,000 2,500 Machine Hours 2,100 2,800 Inspection Hours 80 100 Purchase Orders 10 10 Mr. Mutation has learned that overhead costs are assigned to products on the basis of direct labor hours. The overhead costs for his time period consisted of the following items: Overhead Cost Item Amount Inspecting Costs…arrow_forward

- Zodiac Sound Company manufactures audio systems, both made-to-order and mass-produced systems that are typically sold to large- scale manufacturers of electronics equipment. For competitive reasons, the company is trying to increase its manufacturing cycle efficiency (MCE) measure. As a strategy for improving its MCE performance, the company is considering a switch to JIT manufacturing. While the company managers have a fairly good feel for the costs of implementing JIT, they are unsure about the benefits of such a move, both in financial and nonfinancial terms. To help inform the ultimate decision regarding a move to a JIT system, you've been asked to provide some input. Fortunately, you've recently attended a continuing professional education (CPE) workshop on the costs and benefits of moving to JIT and therefore feel comfortable responding to management's request. Required: 3. Given the estimated data below, calculate the MCE for both the current manufacturing process and the…arrow_forwardZodiac Sound Company manufactures audio systems, both made-to-order and mass-produced systems that are typically sold to large- scale manufacturers of electronics equipment. For competitive reasons, the company is trying to increase its manufacturing cycle efficiency (MCE) measure. As a strategy for improving its MCE performance, the company is considering a switch to JIT manufacturing. While the company managers have a fairly good feel for the costs of implementing JIT, they are unsure about the benefits of such a move, both in financial and nonfinancial terms. To help inform the ultimate decision regarding a move to a JIT system, you've been asked to provide some input. Fortunately, you've recently attended a continuing professional education (CPE) workshop on the costs and benefits of moving to JIT and therefore feel comfortable responding to management's request. Required: 3. Given the estimated data below, calculate the MCE for both the current manufacturing process and the…arrow_forwardValencia Products makes automobile radar detectors and assembles two models: LaserStop and SpeedBuster. Both models use the same electronic components. After reviewing the components required and the profit for each model, the firm found the following linear optimization model for profit, where L is the number of LaserStop models produced and S is the number of SpeedBuster models produced. Implement the linear optimization model on a spreadsheet and use Solver to find an optimal solution. Interpret the optimal solution, identify the binding constraints, and verify the values of the slack variables. Maximize Profit 123 L+ 137 S 18 L+11 S≤ 5000 6L+8S≤4500 L≥0 and S≥0 (Availability of component A) (Availability of component B) Implement the linear optimization model and find an optimal solution. Interpret the optimal solution. The optimal solution is to produce LaserStop models and SpeedBuster models. This solution gives the (Type integers or decimals rounded to two decimal places as…arrow_forward

- As a start-up company, Oriole Enterprises encourages its employees to think through the entire value chain to estimate whether it might be worthwhile to take a risk on new products. As part of that program, Sharon is reviewing a product concept that her intern presented to her. The basic idea is to use a common process, which would result in two intermediate products. One product could be sold right away (X). The other product (Y) would have no immediate sales value but after further processing would yield a very high- value product. Sharon is intrigued enough to dig further into her intern's quantitative analysis, as follows. Sales value of X immediately after the joint process Sales value of Y after further processing Product X's share of the joint process cost Proportion of joint cost allocated to Product Y (a) Your answer is correct. (b) Based on this information, determine which joint cost allocation method the intern must have used when allocating the joint costs to these…arrow_forwardPremium Corporation believes that there is a market for a portable electronic toothbrush that can be easily carried by business travelers. Premium's market research department has surveyed the features and prices of electronic brushes currently on the market. Based on this research, Premium believes that $75 would be about the right price. At this price, marketing believes that about 78,000 new portable brushes can be sold over the product's life cycle. It will cost about $1,170,000 to design and develop the portable brush. Premium has a target profit of 25% of sales. Requirement 1. Determine the total and unit target cost to manufacture, sell, distribute, and service the portable brushes. Requirement 1. Determine the total and unit target cost to manufacture, sell, distribute, and service the portable brushes. Begin by computing the total target cost to manufacture, sell, distribute, and service the portable brushes, then compute the unit target cost to manufacture, sell, distribute,…arrow_forwardEastman Publishing Company is considering publishing an electronic textbook about spreadsheet applications for business. The fixed cost of manuscript preparation, textbook design, and web site construction is estimated to be $171,000. Variable processing costs are estimated to be $8 per book. The publisher plans to sell single-user access to the book for $41. Through a series of web-based experiments, Eastman has created a predictive model that estimates demand as a function of price. The predictive model is demand = 4,000 − 6p, where p is the price of the e-book. (a) Construct an appropriate spreadsheet model for calculating the profit/loss at a given single-user access price taking into account the above demand function. What is the profit estimatedarrow_forward

- The jarvis corporation produces bucket loader assemblies for the tractor industry. The product has a long term life expectancy. Jarvis has a traditional manufacturing and inventory system. Jarvis is considering the installation of a just-in-time inventory system to improve its cost structure. In doing a full study using its manufacturing engineering team as well as consulting with industry JIT experts and the main vendors and suppliers of the components Jarvis uses to manufacture the bucket loader assemblies, the following incremental cost-benefit relevant information is available for analysis: The Jarvis cost of investment capital hurdle rate is 15%. One time cost to rearrange the shop floor to create the manufacturing cell workstations is $275,000. One time cost to retrain the existing workforce for the JIT required skills is $60,000. Anticipated defect reduction is 40%. Currently there is a cost of quality defect assessment listed as $150,000 per year. The setup time for…arrow_forwardAlyssa Stuart is thinking of starting a store that specializes in handmade Viennese style bentwood chairs. Before opening her store, Alyssa is curious about how her profit, revenue, and variable costs will change depending on the amount she charges for the chairs. Alyssa would like you to perform the work required for this analysis and has given you the data. Here are a few things to consider while you perform your analysis: Current competitive prices for Viennese style bentwood chairs are between $225 and $275 a chair. Variable costs will be either $100 or $150 a chair depending on the types of material Alyssa chooses to use. Fixed costs are $10,000 a month. Create an Excel file containing the following information: Alyssa's chairs - Price One Alyssa's chairs - Price Two Chair Price $ 225 Chair Price $ 275 Variable Cost per chair $ 125 Variable Cost per chair $ 150 Fixed Cost $ 10,000 Fixed Cost $…arrow_forwardAs a start-up company, Blue Enterprises encourages its employees to think through the entire value chain to estimate whether it might be worthwhile to take a risk on new products. As part of that program, Laura is reviewing a product concept that her intern presented to her. The basic idea is to use a common process, which would result in two intermediate products. One product could be sold right away (X). The other product (Y) would have no immediate sales value but after further processing would yield a very high- value product. Laura is intrigued enough to dig further into her intern's quantitative analysis, as follows. Sales value of X immediately after the joint process Sales value of Y after further processing Product X's share of the joint process cost Proportion of joint cost allocated to Product Y (a) Your answer is correct. $53,750 $406,000 $20,000 87.5% Based on this information, determine which joint cost allocation method the intern must have used when allocating the joint…arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning

Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning