Concept explainers

Videos

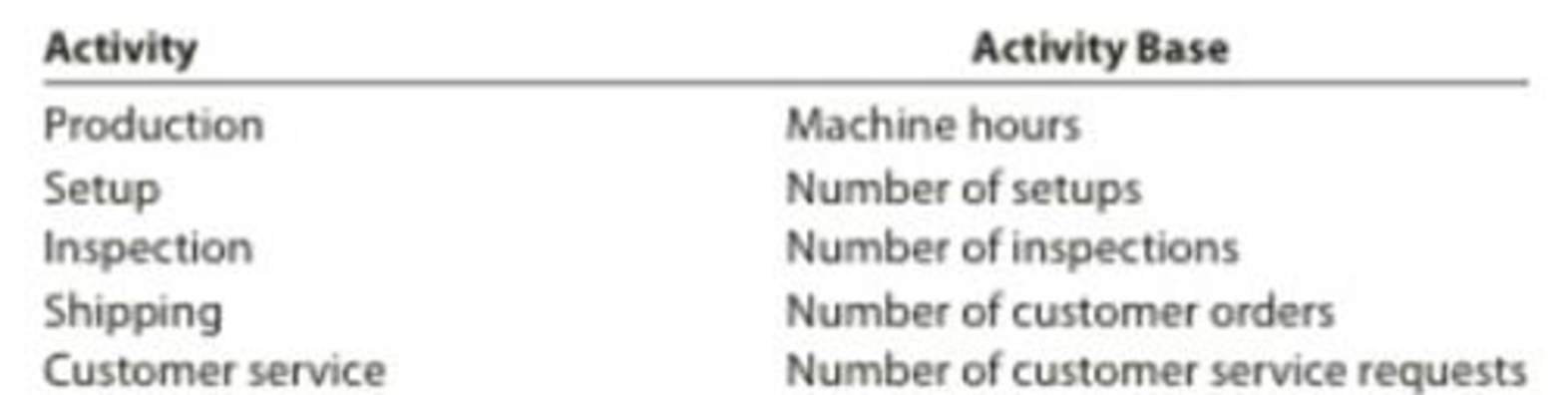

Activity-based product costing

Sweet Sugar Company manufactures three products (white sugar, brown sugar, and powdered sugar) in a continuous production process. Senior management has asked the controller to conduct an activity-based costing study. The controller identified the amount of factory

The activity bases identified for each activity are as follows:

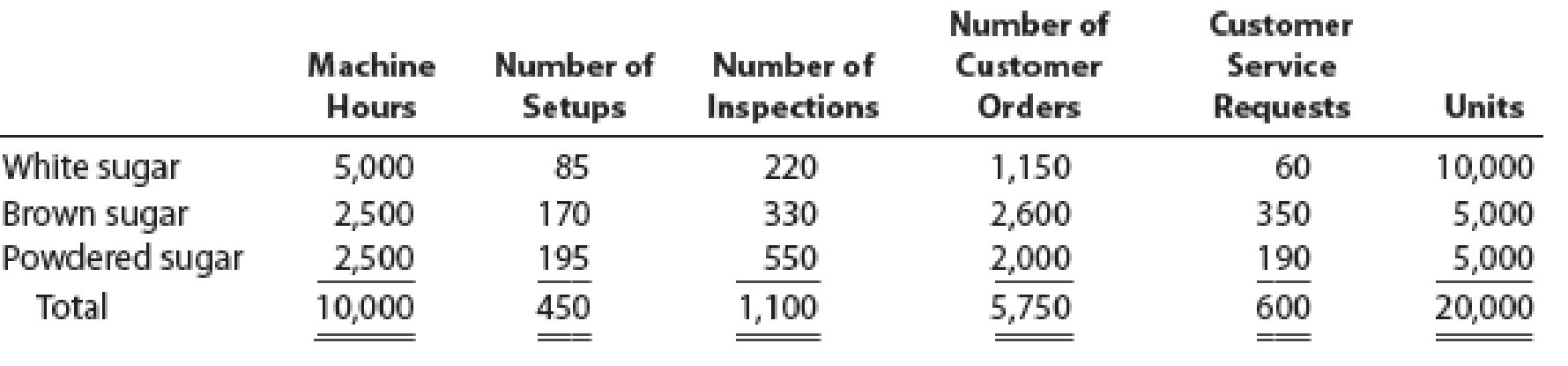

The activity-base usage quantities and units produced for the three products were determined from corporate records and are as follows:

Each product requires 0.5 machine hour per unit.

Instructions

Determine the activity rate for each activity.

Determine the total and per-unit activity cost for all three products. Round to nearest cent.

Why aren’t the activity unit costs equal across all three products since they require the same machine time per unit?

Want to see the full answer?

Check out a sample textbook solution

Chapter 4 Solutions

Managerial Accounting

- Please explain the correct approach for solving this general accounting question.arrow_forwardGlobal Fitness LLC reported a debt-to-equity ratio of 1.5 times at the end of 2024. If the firm's total assets at year-end were $36.8 million, how much of their assets are financed with equity?a. $14.72 millionb. $22.08 millionc. $9.2 milliond. $55.2 million i need helparrow_forwardPlease provide the accurate answer to this financial accounting problem using valid techniques.arrow_forward

- Can you help me solve this general accounting problem with the correct methodology?arrow_forwardGlobal Fitness LLC reported a debt-to-equity ratio of 1.5 times at the end of 2024. If the firm's total assets at year-end were $36.8 million, how much of their assets are financed with equity?a. $14.72 millionb. $22.08 millionc. $9.2 milliond. $55.2 million helparrow_forwardPlease help me solve this financial accounting problem with the correct financial process.arrow_forward

- Please provide answer accurate of this Financial Accounting Question without any problemarrow_forwardI need help finding the accurate solution to this general accounting problem with valid methods.arrow_forwardPlease provide the answer to this financial accounting question using the right approach.arrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning