Videos

"I know headquarters wants us to add that new product line.” said Dell Havasi, manager of Billings Company's Office Products Division. "But I want to see the numbers before I make any move. Our division's return on investment (ROI) has led the company for three years, and I don't want any letdown".

Billings Company is a decentralized wholesaler with five autonomous divisions. The divisions are evaluated on the basis of ROI, with year-end bonuses given to the divisional managers who have the highest ROLs. Operating results for the company's Office Products Division for this year are given below:

The company had an overall return on investment [ROI) of 15% this year [considering all divisions). Next year the Office Products Division has an opportunity to add a new product line that would require an additional investment that would increase average operating assets by $1,000,000. The cost and revenue characteristics of the new product line per year would be: Required:

Required:

1. Compute the Office Products Division's ROI for this year.

7. Compute the Office Products Division's ROI for the new product line by itself.

3. Compute the Office Products Division's ROI for next year assuming that it performs the same as this year and adds the new product line.

4. If you were in Dell Havasi's position, would you accept or reject the new product line? Explain.

5. Why do you suppose headquarters is anxious for the Office Products Division to add the new product line?

6. Suppose that the company's minimum required

a. Compute the Office Products Division's residual income for this year.

b. Compute the Office Products Division's residual income for the new product line by itself.

c. Compute the Office Products Division's residual income for next year assuming that it performs the same as this year and adds the new product line.

d. Using the residual income approach, if you were in Dell Havasi's position, would you accept or reject the new product line? Explain.

1)

Return on Investment, Margin and Turnover:

Return on Investment is calculated as Margin divided by Turnover. Here Margin refers to the Sales Margin and Turnover refers to the Capital Turnover Ratio.

Return on Investment calculations are important from a business standpoint as they help in evaluation of new investment proposals, make or buy decisions, capital expenditure projects and whether to invest in a particular company or not.

Return on Investment for the year

Answer to Problem 18P

Solution:

The Return on Investment for the year is 3.2%

Explanation of Solution

- Given:

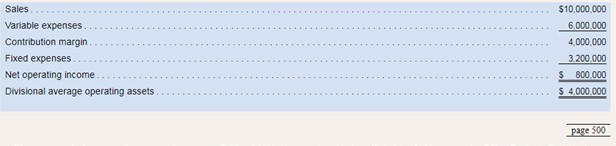

Sales = $10,000,000

Variable Expense = $6,000,000

Fixed Expenses=$3,200,000

Cost of capital = 15%

Average Operating Assets = $4,000,000

Calculations:

Hence it can be seen that the Return on Investment is calculated as Margin divided by Turnover.

2)

Return on Investment, Margin and Turnover

Return on Investment is calculated as Margin divided by Turnover. Here Margin refers to the Sales Margin and Turnover refers to the Capital Turnover Ratio.

Return on Investment calculations are important from a business standpoint as they help in evaluation of new investment proposals, make or buy decisions, capital expenditure projects and whether to invest in a particular company or not.

Return on Investment for the product line

Answer to Problem 18P

Solution:

The Return on Investment for the product line is 4%

Explanation of Solution

- Given: Sales = $2,000,000

Variable Expense = $1,200,000

Fixed Expenses=$640,000

Cost of capital = 15%

Average Operating Assets = $1,000,000

- Formulae used:

Calculations:

- Margin is the percentage of Profit earned by an entity in a given reporting period. Profit is calculated as Revenues less Cost of Goods Sold and Indirect Expenses.

- Margin is Profit expressed in terms of Sales as a percentage.

- Turnover is the capital turnover ratio. This is calculated by dividing the sales by the average operating assets for the year.

- Return on Investment is calculated as Margin divided by Turnover.

- Return on Investment calculations are important from a business standpoint as they help in evaluation of new investment proposals, make or buy decisions, capital expenditure projects and whether to invest in a particular company or not.

Hence it can be seen that the Return on Investment is calculated as Margin divided by Turnover.

3)

Return on Investment, Margin and Turnover

Return on Investment is calculated as Margin divided by Turnover. Here Margin refers to the Sales Margin and Turnover refers to the Capital Turnover Ratio.

Return on Investment calculations are important from a business standpoint as they help in evaluation of new investment proposals, make or buy decisions, capital expenditure projects and whether to invest in a particular company or not.

Return on Investment for the year with new product.

Answer to Problem 18P

Solution:

The Return on Investment for the year is 3.33%

Explanation of Solution

- Given: Sales = $12,000,000 [$10,000,000 + $2,000,000]

Variable Expense = $7,200,000 [ $6,000,000 + $1,200,000]

Fixed Expenses=$3,840,000 [$3,200,000 + $640,000]

Cost of capital = 15%

Average Operating Assets = $5,000,000 [$4,000,000 + $1,000,000]

- Formulae used:

- Calculations:

- Margin is the percentage of Profit earned by an entity in a given reporting period. Profit is calculated as Revenues less Cost of Goods Sold and Indirect Expenses.

- Margin is Profit expressed in terms of Sales as a percentage.

- Turnover is the capital turnover ratio. This is calculated by dividing the sales by the average operating assets for the year.

- Return on Investment is calculated as Margin divided by Turnover.

- Return on Investment calculations are important from a business standpoint as they help in evaluation of new investment proposals, make or buy decisions, capital expenditure projects and whether to invest in a particular company or not.

Hence it can be seen that the Return on Investment is calculated as Margin divided by Turnover.

4)

Return on Investment, Margin and Turnover

Return on Investment is calculated as Margin divided by Turnover. Here Margin refers to the Sales Margin and Turnover refers to the Capital Turnover Ratio.

Return on Investment calculations are important from a business standpoint as they help in evaluation of new investment proposals, make or buy decisions, capital expenditure projects and whether to invest in a particular company or not.

Whether to accept to reject the new product line.

Answer to Problem 18P

Solution:

The new product line must be accepted.

Explanation of Solution

- The return on investment of the company before the introduction of the product line is 3.2%.

- The return on investment of the new product is 4%

- Combined return on investment of the company after the introduction of the product is 3.33%

- The return on investment of the new product is greater than the return on investment of the company

- After introduction of the new product, sales, revenues and operating assets of the company all increase and consequently so does the return on investment.

- Hence since the return on investment is increasing, the new product may be accepted.

Hence the new product line may be accepted as the return on investment of the product is positive and the return on investment of the company increases after the new product line is accepted.

5)

Return on Investment, Margin and Turnover

Return on Investment is calculated as Margin divided by Turnover. Here Margin refers to the Sales Margin and Turnover refers to the Capital Turnover Ratio.

Return on Investment calculations are important from a business standpoint as they help in evaluation of new investment proposals, make or buy decisions, capital expenditure projects and whether to invest in a particular company or not.

Why the company is eager to add the new product line.

Answer to Problem 18P

Solution:

The company is eager to add the new product line since the roi of the company increases, after introduction of the new product line.

Explanation of Solution

- The return on investment of the company before the introduction of the product line is 3.2%.

- The return on investment of the new product is 4%

- Combined return on investment of the company after the introduction of the product is 3.33%

- The return on investment of the new product is greater than the return on investment of the company

- After introduction of the new product, sales, revenues and operating assets of the company all increase and consequently so does the return on investment

- Return on investment as an investment measure seeks to accept any investment proposal that generates positive returns.

- In the given instance, the return on investment of the new product line results in a boost in the return on investment of the company and hence the eagerness of the company to add the new product line is justified.

Hence it can be seen that the new product line is profitable and hence the company is eager to add the same to its operations.

6)

a)

Residual Income

In investment accounting, residual income is the income over the minimum expected rate of return or cost of capital. Hence residual income is calculated as Net Operating Income for the year less the cost of capital.

Net Operating Income is the net operating income for the year and Cost of capital is Minimum rate of return expected from average operating assets for the year.

Residual Income for the year

Answer to Problem 18P

Solution:

Residual Income is $320000.

Explanation of Solution

- Given: Sales = $10,000,000

Variable Expense = $6,000,000

Fixed Expenses=$3,200,000

Cost of capital = 12%

Average Operating Assets = $4,000,000

Formulae used:

- Calculations:

- In any organization, the capital invested carries a cost. This cost can be in the form of dividends on shareholder capital.

- To evaluate the investment proposal, the residual income approach is used. Under this approach, the Residual income is calculated as Net Operating Income for the year less the Cost of capital for the year.

- Cost of capital is calculated as Average Operating Assets x Minimum rate of return expected and is expressed as an amount in value.

- Net Operating Income for the year is calculated as Revenues for the year less Cost of goods sold and indirect expenses such as administrative expenses, selling and distribution expenses etc.

- Residual Income is therefore the remainder of the Net Operating Income for the year after deducting the Cost of Equity capital.

Hence the residual income is calculated for the previous year.

6)

b)

Residual Income

In investment accounting, residual income is the income over the minimum expected rate of return or cost of capital. Hence residual income is calculated as Net Operating Income for the year less the cost of capital.

Net Operating Income is the net operating income for the year and Cost of capital is Minimum rate of return expected from average operating assets for the year.

Residual Income for the product line

Answer to Problem 18P

Solution:

Residual Income is $40,000.

Explanation of Solution

- Given: Sales = $2,000,000

Variable Expense = $1,200,000

Fixed Expenses=$640,000

Cost of capital = 12%

Average Operating Assets = $1,000,000

Formulae used:

- Calculations:

- In any organization, the capital invested carries a cost. This cost can be in the form of dividends on shareholder capital.

- To evaluate the investment proposal, the residual income approach is used. Under this approach, the Residual income is calculated as Net Operating Income for the year less the Cost of capital for the year.

- Cost of capital is calculated as Average Operating Assets x Minimum rate of return expected and is expressed as an amount in value.

- Net Operating Income for the year is calculated as Revenues for the year less Cost of goods sold and indirect expenses such as administrative expenses, selling and distribution expenses etc.

- Residual Income is therefore the remainder of the Net Operating Income for the year after deducting the Cost of Equity capital.

Hence the residual income is calculated for the product line.

6)

c)

Residual Income

In investment accounting, residual income is the income over the minimum expected rate of return or cost of capital. Hence residual income is calculated as Net Operating Income for the year less the cost of capital.

Net Operating Income is the net operating income for the year and Cost of capital is Minimum rate of return expected from average operating assets for the year.

Residual Income for the company after introduction of the product line

Answer to Problem 18P

Solution:

Residual Income is $360,000.

Explanation of Solution

- Given: Sales = $12,000,000 [$10,000,000 + $2,000,000]

Variable Expense = $7,200,000 [ $6,000,000 + $1,200,000]

Fixed Expenses=$3,840,000 [$3,200,000 + $640,000]

Cost of capital = 12%

Average Operating Assets = $5,000,000 [$4,000,000 + $1,000,000

Formulae used:

- In any organization, the capital invested carries a cost. This cost can be in the form of dividends on shareholder capital.

- To evaluate the investment proposal, the residual income approach is used. Under this approach, the Residual income is calculated as Net Operating Income for the year less the Cost of capital for the year.

- Cost of capital is calculated as Average Operating Assets x Minimum rate of return expected and is expressed as an amount in value.

- Net Operating Income for the year is calculated as Revenues for the year less Cost of goods sold and indirect expenses such as administrative expenses, selling and distribution expenses etc.

- Residual Income is therefore the remainder of the Net Operating Income for the year after deducting the Cost of Equity capital.

Hence the residual income is calculated for the previous year for the combined product lines of the company.

6)

d)

Residual Income as a tool for performance measurement.

In investment accounting, residual income is the income over the minimum expected rate of return or cost of capital. Hence residual income is calculated as Net Operating Income for the year less the cost of capital.

Net Operating Income is the net operating income for the year and Cost of capital is Minimum rate of return expected from average operating assets for the year.

Whether to accept or reject the product line based on residual income

Answer to Problem 18P

Solution:

The product line must be accepted as the residual income is positive.

Explanation of Solution

- In any organization, the capital invested carries a cost. This cost can be in the form of dividends on shareholder capital.

- To evaluate the investment proposal, the residual income approach is used. Under this approach, the Residual income is calculated as Net Operating Income for the year less the Cost of capital for the year.

- Cost of capital is calculated as Average Operating Assets x Minimum rate of return expected and is expressed as an amount in value.

- Net Operating Income for the year is calculated as Revenues for the year less Cost of goods sold and indirect expenses such as administrative expenses, selling and distribution expenses etc.

- Residual Income is therefore the remainder of the Net Operating Income for the year after deducting the Cost of Equity capital.

- In the given instance, the residual income of the new product line as well as the combined product lines of the entity after introduction of the new product line are positive.

- This means that the revenue from new product line exceeds the minimum return required from operating assets.

- Hence since the new product line is profitable, based on the residual income earned, the new product line must be accepted.

Hence the usage of residual income approach to evaluate investment opportunities can be seen.

Want to see more full solutions like this?

Chapter 10 Solutions

INTRO MGRL ACCT LL W CONNECT

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,