Videos

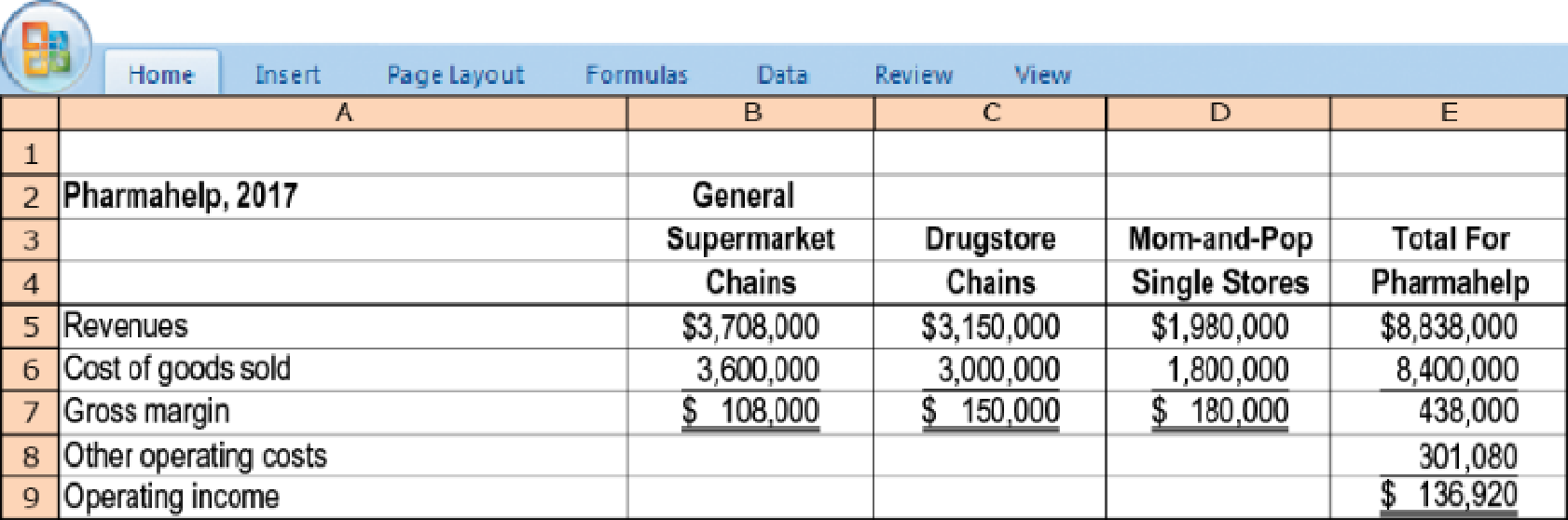

Activity-based costing, merchandising. Pharmahelp, Inc., a distributor of special pharmaceutical products, operates at capacity and has three main market segments:

- a. General supermarket chains

- b. Drugstore chains

- c. Mom-and-pop single-store pharmacies

Rick Flair, the new controller of Pharmahelp, reported the following data for 2017.

For many years, Pharmahelp has used gross margin percentage

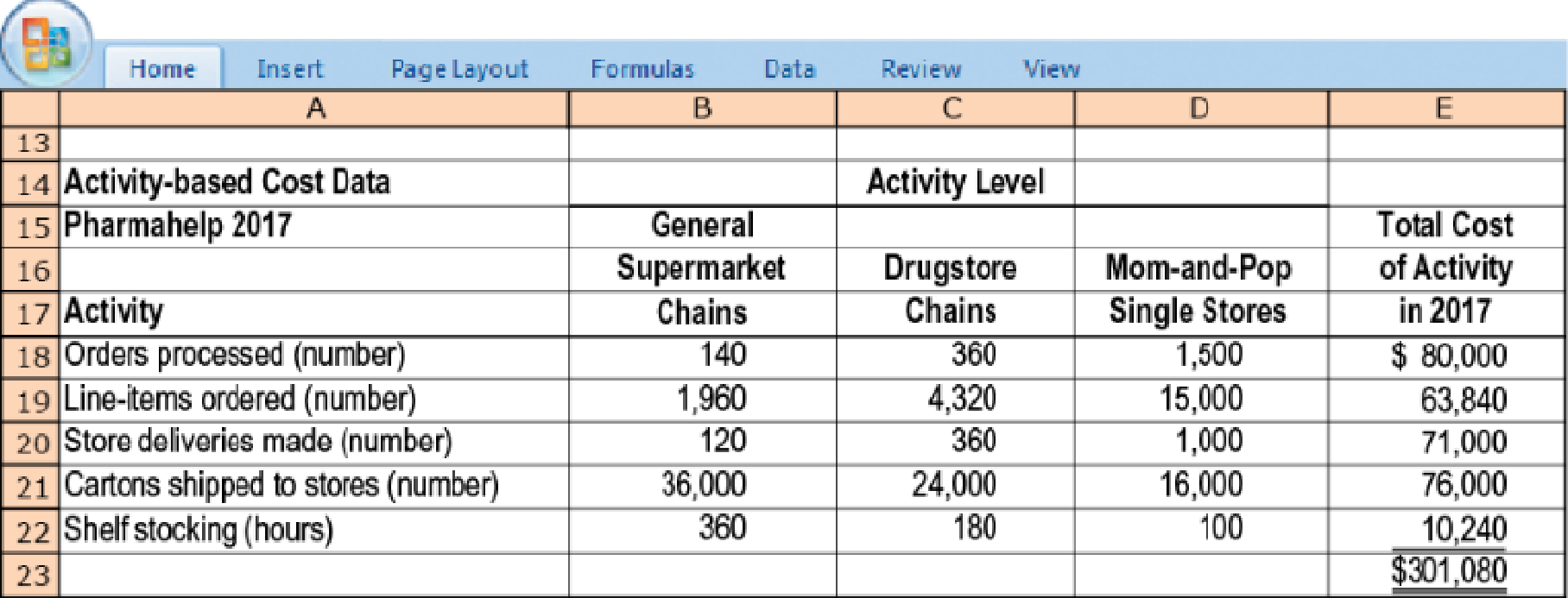

[(Revenue– Cost of goods sold) ÷ Revenue] to evaluate the relative profitability of its market segments. But Flair recently attended a seminar on activity-based costing and is considering using it at Pharmahelp to analyze and allocate “other operating costs.” He meets with all the key managers and several of his operations and sales staff, and they agree that there are five key activities that drive other operating costs at Pharmahelp:

| Activity Area | Cost Driver |

| Order processing | Number of customer purchase orders |

| Line-item processing | Number of line items ordered by customers |

| Delivering to stores | Number of store deliveries |

| Cartons shipped to store | Number of cartons shipped |

| Stocking of customer store shelves | Hours of shelf-stocking |

Each customer order consists of one or more line items. A line item represents a single product (such as Extra-Strength Tylenol Tablets). Each product line item is delivered in one or more separate cartons. Each store delivery entails the delivery of one or more cartons of products to a customer. Pharmahelp’s staff stacks cartons directly onto display shelves in customers’ stores. Currently, there is no additional charge to the customer for shelf-stocking and not all customers use Pharmahelp for this activity. The level of each activity in the three market segments and the total cost incurred for each activity in 2017 is as follows:

- 1. Compute the 2017 gross-margin percentage for each of Pharmahelp’s three market segments.

Required

- 2. Compute the cost driver rates for each of the five activity areas.

- 3. Use the activity-based costing information to allocate the $301,080 of “other operating costs” to each of the market segments. Compute the operating income for each market segment.

- 4. Comment on the results. What new insights are available with the activity-based costing information?

Want to see the full answer?

Check out a sample textbook solution

Chapter 5 Solutions

Horngren's Cost Accounting, Student Value Edition (16th Edition)

- Please answer the following requirements a and b on these general accounting questionarrow_forwardGeneral Accountingarrow_forwardHarper, Incorporated, acquires 40 percent of the outstanding voting stock of Kinman Company on January 1, 2023, for $210,000 in cash. The book value of Kinman's net assets on that date was $400,000, although one of the company's buildings, with a $60,000 carrying amount, was actually worth $100,000. This building had a 10-year remaining life. Kinman owned a royalty agreement with a 20-year remaining life that was undervalued by $85,000. Kinman sold Inventory with an original cost of $60,000 to Harper during 2023 at a price of $90,000. Harper still held $15,000 (transfer price) of this amount in Inventory as of December 31, 2023. These goods are to be sold to outside parties during 2024. Kinman reported a $40,000 net loss and a $20,000 other comprehensive loss for 2023. The company still manages to declare and pay a $10,000 cash dividend during the year. During 2024, Kinman reported a $40,000 net income and declared and paid a cash dividend of $12,000. It made additional inventory sales…arrow_forward

- Solve this general accounting question not use aiarrow_forwardPlease provide solution this general accounting questionarrow_forwardMichael McDowell Co. establishes a $108 million liability at the end of 2025 for the estimated site-cleanup costs at two of its manufacturing facilities. All related closing costs will be paid and deducted on the tax return in 2026. Also, at the end of 2025, the company has $54 million of temporary differences due to excess depreciation for tax purposes, $7.56 million of which will reverse in 2026. The enacted tax rate for all years is 20%, and the company pays taxes of $34.56 million on $172.80 million of taxable income in 2025. McDowell expects to have taxable income in 2026. Assuming that the only deferred tax account at the beginning of 2025 was a deferred tax liability of $5,400,000, draft the income tax expense portion of the income statement for 2025, beginning with the line "Income before income taxes." (Hint: You must first compute (1) the amount of temporary difference underlying the beginning $5,400,000 deferred tax liability, then (2) the amount of temporary differences…arrow_forward

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning