Concept explainers

Videos

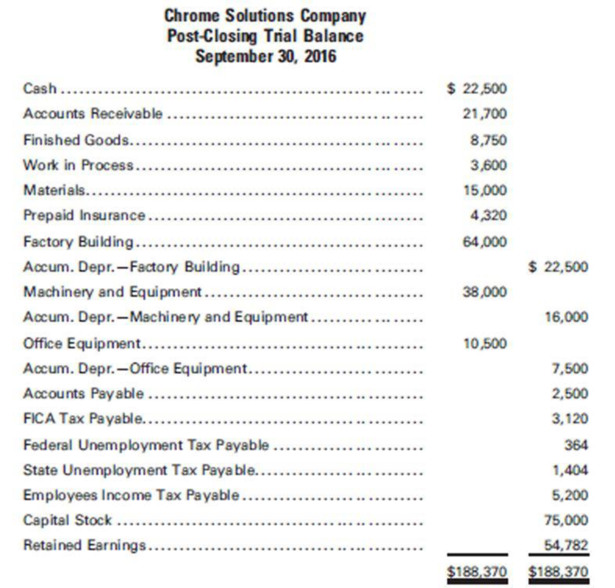

Chrome Solutions Company manufactures special chromed parts made to the order and specifications of the customer. It has two production departments, Stamping and Plating, and two service departments, Power and Maintenance. In any production department, the job in process is wholly completed before the next job is started.

The company operates on a fiscal year, which ends September 30. Following is the post-closing

Additional information:

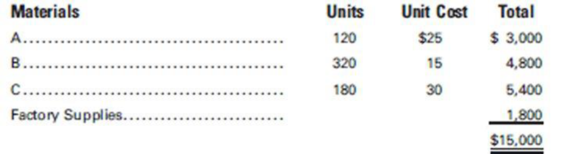

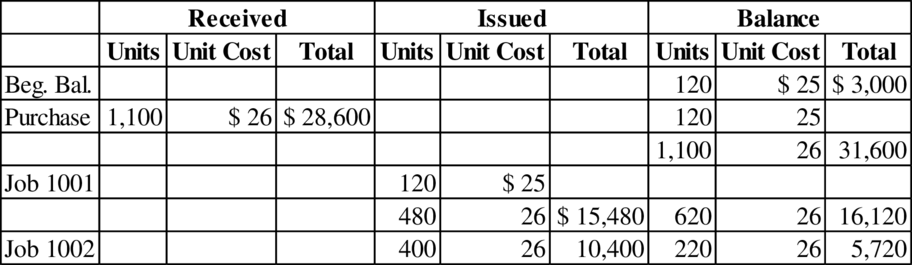

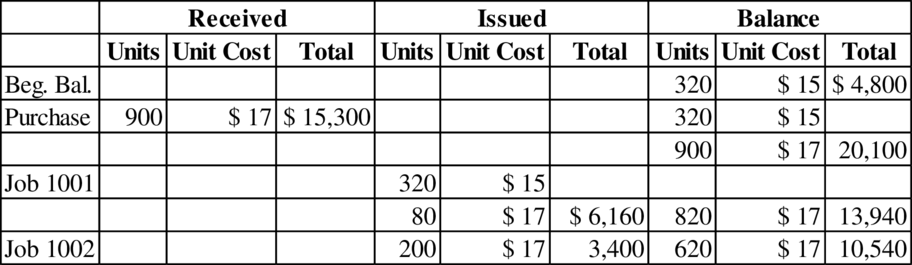

1. The balance of the materials account represents the following:

The company uses the FIFO method of accounting for all inventories. Material A is used in the Stamping Department, and materials B and C are used in the Plating Department.

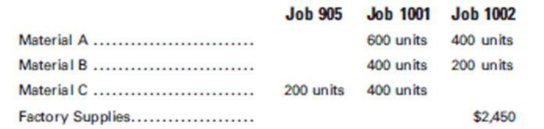

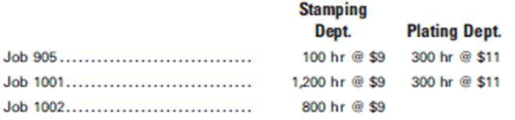

2. The balance of the work in process account represents the following costs that are applicable to Job 905. (The customer’s order is for 1,000 units of the finished product.)

3. The finished goods account reflects the cost of Job 803, which was finished at the end of the preceding month and is awaiting delivery orders from the customer.

4. At the beginning of the year, factory

In October, the following transactions were recorded:

a. Purchased the following materials and supplies on account:

b. The following materials were issued to the factory:

Customers’ orders covered by Jobs 1001 and 1002 are for 1,000 and 500 units of finished product, respectively.

c. Factory wages and office, sales, and administrative salaries are paid at the end of each month. (Assume FICA and federal income tax rates of 8% and 10%, respectively.) Record the company’s liability for state and federal

Wages of the supervisors, custodial personnel, etc., totaled $9,500; administrative salaries were $18,300.

d. Miscellaneous factory overhead incurred during October totaled $4,230. Miscellaneous selling and administrative expenses were $1,500. These items as well as the FICA tax and federal income tax withheld for September were paid. (See account balances on the post-closing trial balance for September 30.)

e. Annual

Factory buildings–5%

Machinery and equipment–20%

Office equipment–20%

f. The balance of the prepaid insurance account represents a three-year premium for a fire insurance policy covering the factory building and machinery. It was paid on the last day of the preceding month and became effective on October 1.

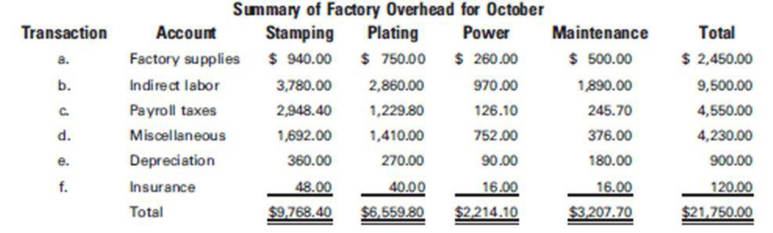

g. The summary of factory overhead prepared from the factory overhead ledger is reproduced here:

h. The total expenses of the Maintenance Department are distributed on the basis of floor space occupied by the Power Department (8,820 sq ft), Stamping Department (19,500 sq ft), and Plating Department (7,875 sq ft). The power department expenses are then allocated equally to the Stamping and Plating departments.

i. After the actual factory overhead expenses have been distributed to the departmental accounts and the applied factory overhead has been recorded and posted, any balances in the departmental accounts are transferred to Under- and Overapplied Overhead.

j. Jobs 905 and 1001 were finished during the month. Job 1002 is still in process at the end of the month.

k. During the month, Jobs 803 and 905 were sold with a mark-on percentage of 50% on cost.

l. Received $55,500 from customers in payment of their accounts.

m. Checks were issued in the amount of $43,706 for payment of the payroll.

Required

- 1. Set up the beginning trial balance in T-accounts.

- 2. Prepare materials inventory ledger cards and enter October 1 balances.

- 3. Prepare a Payroll Summary and Schedule of Earnings and Payroll Taxes for the month of October.

- 4. Set up

job cost sheets as needed. - 5. Record all transactions and related entries for October and post to T-accounts.

- 6. Prepare a service department expense distribution worksheet for October.

- 7. At the end of the month:

- a. Analyze the balance in the materials account, the work in process account, and the finished goods account.

- b. Prepare the statement of cost of goods manufactured for the month ended October 31.

1.

Prepare T-accounts for company C.

Explanation of Solution

Prepare T-accounts for company C:

| Cash | ||||||

| October.1 | 22,500 | October.31 | d. | 14,050 | ||

| 31 | l. | 55,500 | m. | 43,706 | ||

| Total | 78,000 | 57,756 | ||||

| 20,244 | ||||||

| Accounts receivable | ||||||

| October.1 | 21,700 | October.31 | l. | 55,500 | ||

| 31 | k. | 43,140 | ||||

| Total | 64,840 | |||||

| 9,340 | ||||||

| Finished Goods | ||||||

| October.1 | 8,750 | October.31 | k. | 28,760 | ||

| 31 | j. | 78,700 | ||||

| Total | 87,450 | |||||

| 58,690 | ||||||

| Work in Process | ||||||

| October.1 | 3,600 | October.31 | j. | 78,700 | ||

| 31 | b. | 52,600 | ||||

| c. | 25,500 | |||||

| i. | 22,000 | |||||

| Total | 103,700 | |||||

| 25,000 | ||||||

| Materials | ||||||

| October.1 | 15,000 | October.31 | b. | 55,050 | ||

| 31 | a. | 69,500 | ||||

| Total | 84,500 | |||||

| 29,450 | ||||||

| Prepaid Insurance | ||||||

| October.1 | 4,320 | October.31 | f. | 120 | ||

| Total | 4,320 | |||||

| 4,200 | ||||||

| Factory Building | ||||||

| October.1 | 64,000 | |||||

| Accumulated Depreciation—Factory Building | ||||||

| October.1 | 22,500 | |||||

| 31 | e. | 267 | ||||

| 22,767 | ||||||

| Machinery & Equipment | ||||||

| October.1 | 38,000 | |||||

| Accumulated Depreciation—Factory Building | ||||||

| October.1 | 16,000 | |||||

| 31 | e. | 633 | ||||

| 16,633 | ||||||

| Office Equipment | ||||||

| October.1 | 10,500 | |||||

| Accumulated Depreciation—Office Equipment | ||||||

| October.1 | 7,500 | |||||

| 31 | 175 | |||||

| 7,675 | ||||||

| Accounts Payable | ||||||

| October.1 | 2,500 | |||||

| 31 | a. | 69,500 | ||||

| 72,000 | ||||||

| FICA Tax Payable | ||||||

| October.31 | d. | 3,120 | October.1 | 3,120 | ||

| c. | 4,264 | |||||

| 31 | c. | 4,264 | ||||

| 11,648 | ||||||

| 8,528 | ||||||

| Federal Unemployment Tax Payable | ||||||

| October.1 | 364 | |||||

| 31 | c. | 533 | ||||

| 897 | ||||||

| State Unemployment Tax Payable | ||||||

| October.1 | 1,404 | |||||

| 31 | c. | 2,132 | ||||

| 3,536 | ||||||

| Employees Income Tax Payable | ||||||

| October.31 | d. | 5,200 | October.1 | 5,200 | ||

| 31 | c. | 5,330 | ||||

| 10,530 | ||||||

| 5,330 | ||||||

| Wages Payable | ||||||

| October.31 | m. | 43,706 | October.31 | 43,706 | ||

| Wages Payable | ||||||

| October.31 | m. | 43,706 | October.31 | 43,706 | ||

| Capital Stock | ||||||

| October.1 | 75,000 | |||||

| Retained Earnings | ||||||

| October.1 | 54,782 | |||||

| Factory Overhead | ||||||

| October.31 | b. | 2,450 | October.31 | g. | 21,750 | |

| c. | 9,500 | |||||

| c. | 4,550 | |||||

| d. | 4,230 | |||||

| e. | 900 | |||||

| f. | 120 | |||||

| 21,750 | 21,750 | |||||

| Factory Overhead—Stamping | ||||||

| October.31 | g. | 9,768.40 | October.31 | i. | 10,500 | |

| h. | 1,728.15 | i. | 2,494.42 | |||

| h. | 1,497.87 | |||||

| 12,994.42 | 12,994.42 | |||||

| Factory Overhead—Plating | ||||||

| October.31 | g. | 6,559.80 | October.31 | i. | 11,500 | |

| h. | 697.90 | |||||

| h. | 1,497.88 | |||||

| i. | 2,744.42 | |||||

| 11,500 | 11,500 | |||||

| Applied Factory Overhead—Stamping | ||||||

| October.31 | i. | 10,500 | October.31 | i. | 10,500 | |

| 10,500 | 10,500 | |||||

| Applied Factory Overhead—Plating | ||||||

| October.31 | i. | 11,500 | October.31 | i. | 11,500 | |

| 11,500 | 11,500 | |||||

| Factory Overhead—Power | ||||||

| October.31 | g. | 2,214.10 | October.31 | h. | 2,995.75 | |

| h. | 781.65 | |||||

| 2,995.75 | 2,995.75 | |||||

| Factory Overhead—Maintenance | ||||||

| October.31 | g. | 3,207.70 | October.31 | h. | 3,207.70 | |

| 3,207.70 | 3,207.70 | |||||

| Under- and Over-applied Overhead | ||||||

| October.31 | i. | 250.00 | ||||

| 250.00 | ||||||

| Sales | ||||||

| October.31 | k. | 43,140 | ||||

| 43,140 | ||||||

| Cost of Goods Sold | ||||||

| October.31 | k. | 28,760 | ||||

| 28,760 | ||||||

| Payroll | ||||||

| October.31 | c. | 53,300 | October.31 | c. | 53,300 | |

| 53,300 | 53,300 | |||||

| Salaries | ||||||

| October.31 | c. | 18,300 | ||||

| 18,300 | ||||||

| Payroll Tax Expense—Salaries | ||||||

| October.31 | c. | 2,379 | ||||

| 2,379 | ||||||

| Miscellaneous Selling & Administrative Expense | ||||||

| October.31 | d. | 1,500 | ||||

| 1,500 | ||||||

| Depreciation Expense—Office Equipment | ||||||

| October.31 | e. | 175 | ||||

| 175 | ||||||

2.

Prepare materials inventory ledger cards and enter October 1 balances.

Explanation of Solution

Prepare materials inventory ledger cards and enter October 1 balances:

For Material A:

Table (1)

For Material B:

Table (2)

For Material C:

Table (3)

Factory supplies:

| Particulars | Amounts ($) |

| Beginning balance | $ 1,800 |

| Purchases | $ 3,200 |

| Issued | ($ 2,450) |

| Ending balance | $ 2,550 |

Table (4)

Total direct materials issued are $52,600

3.

Prepare a Payroll Summary and Schedule of Earnings and Payroll Taxes for the month of October.

Explanation of Solution

Prepare a Payroll Summary and Schedule of Earnings and Payroll Taxes for the month of October:

Payroll Summary:

| Particulars | Factory Employees | Sales and Administrative Employees | Total |

| Gross Earnings (A) | $ 35,000 | $ 18,300 | $ 53,300 |

| Withholdings and deductions: | |||

| FICA tax | $ 2,800 | $ 1,464 | $ 4,264 |

| Income tax | $ 3,500 | $ 1,830 | $ 5,330 |

| Total (B) | $ 6,300 | $ 3,294 | $ 9,594 |

| Net earnings (A+B) | $ 28,700 | $ 15,006 | $ 43,706 |

Table (5)

Compute the amount of total factory labor:

| Particulars | Factory Employees |

| Job 905 | $4,200 |

| Job 1001 | 14,100 |

| Job 1002 | 7,200 |

| Total direct labor | $25,500 |

| Indirect labor | 9,500 |

| Total factory labor | 35,000 |

Table (6)

Schedule of Earnings and Payroll Taxes:

| Particulars | Gross Earnings | FICA | State | FUTA | Total Payroll Taxes |

| 8% | 4% | 1% | |||

| Non factory employees | $ 18,300 | $ 1,464 | $ 732 | $ 183 | $ 2,379 |

| Factory employees | 35,000 | 2,800 | 1,400 | 350 | 4,550 |

| Total | $ 53,300 | $ 4,264 | $ 2,132 | $ 533 | $ 6,929 |

Table (7)

4.

Prepare a job cost sheets as needed.

Explanation of Solution

Prepare a job cost sheets as needed:

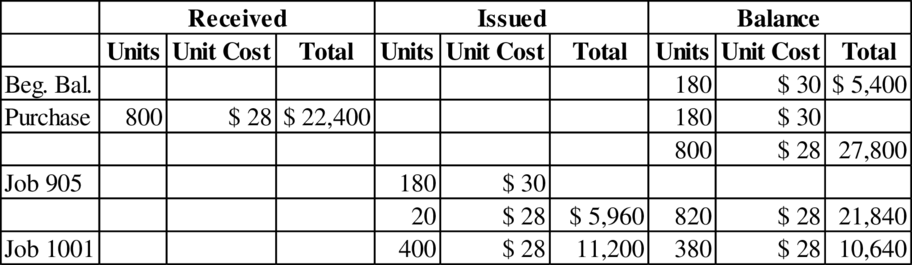

| Job Cost Sheet—Job 905 | ||||||

| Date | Material | Direct labor | Factory Overhead | |||

| October 1 | 1500 | 1200 | 900 | |||

| Material C | 5,960 | Stamping | 900 | 100 hr @5.00 | 500 | |

| Plating | 3,300 | 300 hr @19.167 | 5,750 | |||

| Totals | 7,460 | 5,400 | 7,150 | |||

| Job total | 20,010 | |||||

Table (8)

| Job Cost Sheet—Job 1001 | ||||||

| Date | Material | Direct labor | Factory Overhead | |||

| October 1 | Material A | 15,480 | ||||

| Material B | 6,160 | Stamping | 10,800 | 1,200 hr @5.00 | 6,000 | |

| Material C | 11,200 | Plating | 3,300 | 300 hr @19.167 | 5,750 | |

| Totals | 32,840 | 14,100 | 11,750 | |||

| Job total | 58,690 | |||||

Table (9)

| Job Cost Sheet—Job 1002 | ||||||

| Date | Material | Direct labor | Factory Overhead | |||

| October 1 | Material A | 10,400 | ||||

| Material B | 3,400 | Stamping | 7,200 | 800 hr @5.00 | 4,000 | |

| Totals | 13,800 | 7,200 | 4,000 | |||

| Job total | 25,000 | |||||

Table (10)

5.

Prepare journal entries for the given transactions for October.

Explanation of Solution

Prepare journal entries for the given transactions for October:

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| October | ||||

| a. | Materials | 69,500 | ||

| Accounts Payable | 69,500 | |||

| (To record the materials purchased) | ||||

| b. | Work in Process | 52,600 | ||

| Factory Overhead | 2,450 | |||

| Materials | 55,050 | |||

| (To record the issuance of materials to the factory) | ||||

| c. | Payroll | 53,300 | ||

| FICA Tax Payable | 4,264 | |||

| Employees Income Tax Payable | 5,330 | |||

| Wages Payable | 43,706 | |||

| (To record the wages payable) | ||||

| Work in Process | 25,500 | |||

| Factory Overhead | 9,500 | |||

| Salaries | 18,300 | |||

| Payroll | 53,300 | |||

| (To record the distribution of payroll to work in process and overhead) | ||||

| Factory Overhead | 4,550 | |||

| Payroll Tax Expense—Salaries | 2,379 | |||

| FICA Tax Payable | 4,264 | |||

| Federal Unemployment Tax Payable | 533 | |||

| State Unemployment Tax Payable |

2,132 | |||

| (To record the employer payroll taxes) | ||||

| d. | Factory Overhead | 4,230 | ||

| Miscellaneous, Selling & Administration Expense | 1,500 | |||

| FICA Tax Payable | 3,120 | |||

| Employees Income Tax Payable | 5,200 | |||

| Cash | 14,050 | |||

| (To record the payment made for expenses) | ||||

| e. | Factory Overhead | 900 | ||

| Depreciation Expense—Office Equipment | 175 | |||

| Accumulated Depreciation—Factory Building | 267 | |||

| Accumulated Depreciation—Machinery & Equipment | 633 | |||

| Accumulated Depreciation—Office Equipment | 175 | |||

| (To record the depreciation) | ||||

| f. | Factory Overhead | 120 | ||

| Prepaid Insurance | 120 | |||

| (To record the insurance expired) | ||||

| g. | Factory Overhead—Stamping | 9,768.40 | ||

| Factory Overhead—Plating | 6,559.80 | |||

| Factory Overhead—Power | 2,214.10 | |||

| Factory Overhead—Maintenance | 3,207.70 | |||

| Factory Overhead | 21,750 | |||

| (To record the distribution of factory overhead to other departments) | ||||

| h. | Factory Overhead—Stamping | 1,728.15 | ||

| Factory Overhead—Plating | 697.90 | |||

| Factory Overhead—Power | 781.65 | |||

| Factory Overhead—Maintenance | 3,207.70 | |||

| (To record the distribution of maintenance overhead to other departments) | ||||

| Factory Overhead—Stamping | 1,497.87 | |||

| Factory Overhead—Plating | 1,497.88 | |||

| Factory Overhead—Power | 2,995.75 | |||

| (To record the distribution of power overhead to producing departments) | ||||

| i. | Work in Process | 22,000 | ||

| Applied Factory Overhead—Stamping | 10,500 | |||

| Applied Factory Overhead—Plating | 11,500 | |||

| (To record the work in process) | ||||

| Applied Factory Overhead---Stamping | 10,500 | |||

| Applied Factory Overhead---Plating | 11,500 | |||

| Factory Overhead—Stamping | 10,500 | |||

| Factory Overhead----Plating | 11,500 | |||

| (To record the transfer of applied overhead to actual overhead) | ||||

| Factory Overhead—Plating | 2,744.42 | |||

| Factory Overhead—Stamping | 2,494.42 | |||

| Under- and Over applied Overhead | 250 | |||

|

(To record the transfer under- and over applied overhead to under- and over applied account) | ||||

| j. | Finished Goods | 78,700 | ||

| Work in Process | 78,700 | |||

| (To record the finished goods during October) | ||||

| k. | Accounts Receivable | 43,140 | ||

| Sales | 43,140 | |||

| Cost of Goods Sold | 28,760 | |||

| Finished Goods | 28,760 | |||

| (To record sales made and cost of goods sold) | ||||

| l. | Cash | 55,500 | ||

| Accounts Receivable | 55,500 | |||

| (To record the cash receipts) | ||||

| m. | Wages Payable | 43,706 | ||

| Cash | 43,706 | |||

| (To record wages paid) |

Table (11)

6.

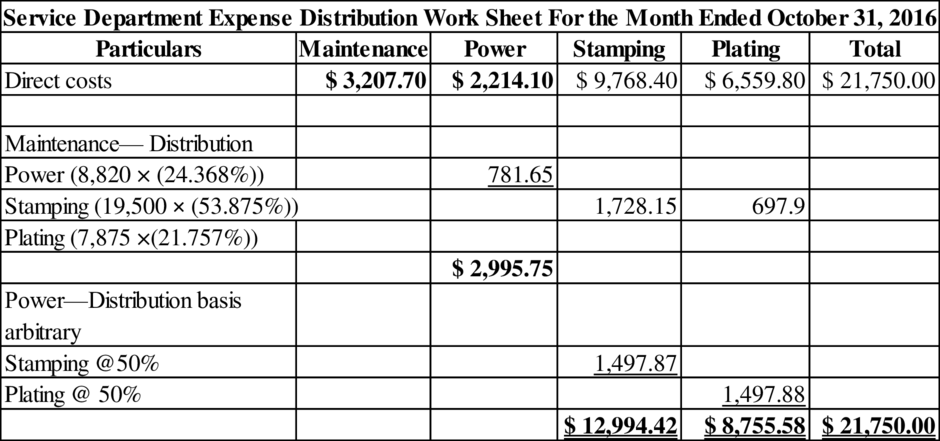

Prepare a service department expense distribution worksheet for October.

Explanation of Solution

Prepare a service department expense distribution worksheet for October:

Table (12)

7. a

Prepare a schedule to analyze the balance in the materials account, the work in process account, and the finished goods account.

Explanation of Solution

Prepare a schedule to analyze the balance in the materials account, the work in process account, and the finished goods account:

| Material Summary—October 31 | |||

| Particulars | Unit (a) | Unit Cost (b) | Total |

| Material | 220 | $ 26 | $ 5,720 |

| Material B | 620 | 17 | 10,540 |

| Material C | 380 | 26 | 10,640 |

| Factory Supplies | 2,550 | ||

| Total | $ 29,450 | ||

| Finished Goods Summary—October 31 | |||

| Job 1001 | $58,690 | ||

| Work in Process Summary—October 31 | |||

| Job 1002 | $25,000 | ||

Table (13)

7. b

Prepare the statement of cost of goods manufactured for the month ended October 31.

Explanation of Solution

Prepare the statement of cost of goods manufactured for the month ended October 31:

| Company C | |

| Statement of Cost of Goods Manufactured | |

| For the Month Ended October 31, 2016 | |

| Direct materials: | |

| Inventory, October 1 | $ 15,000 |

| Add: Purchases | 69,500 |

| Total cost of materials available | $ 84,500 |

| Less: Inventory, October 31 | 29,450 |

| Cost of materials used | $ 55,050 |

| Less: indirect materials used | 2,450 |

| Direct materials used | $ 52,600 |

| Direct labor | 25,500 |

| Applied factory overhead | 22,000 |

| Total manufacturing cost | $ 100,100 |

| Add: Work in process inventory, October 1 | 3,600 |

| Total | $ 103,700 |

| Less: work in process inventory, October 31 | 25,000 |

| Cost of goods manufactured | $ 78,700 |

Table (14)

Want to see more full solutions like this?

Chapter 4 Solutions

Principles of Cost Accounting

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning