Concept explainers

Videos

Statement of

• LO21–3, LO21–8

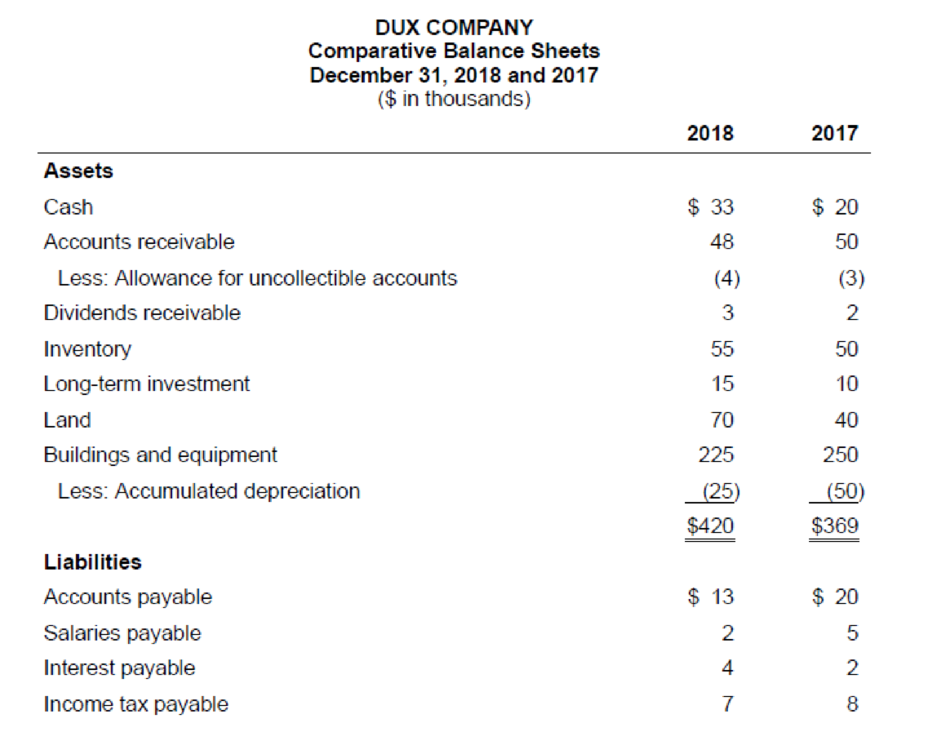

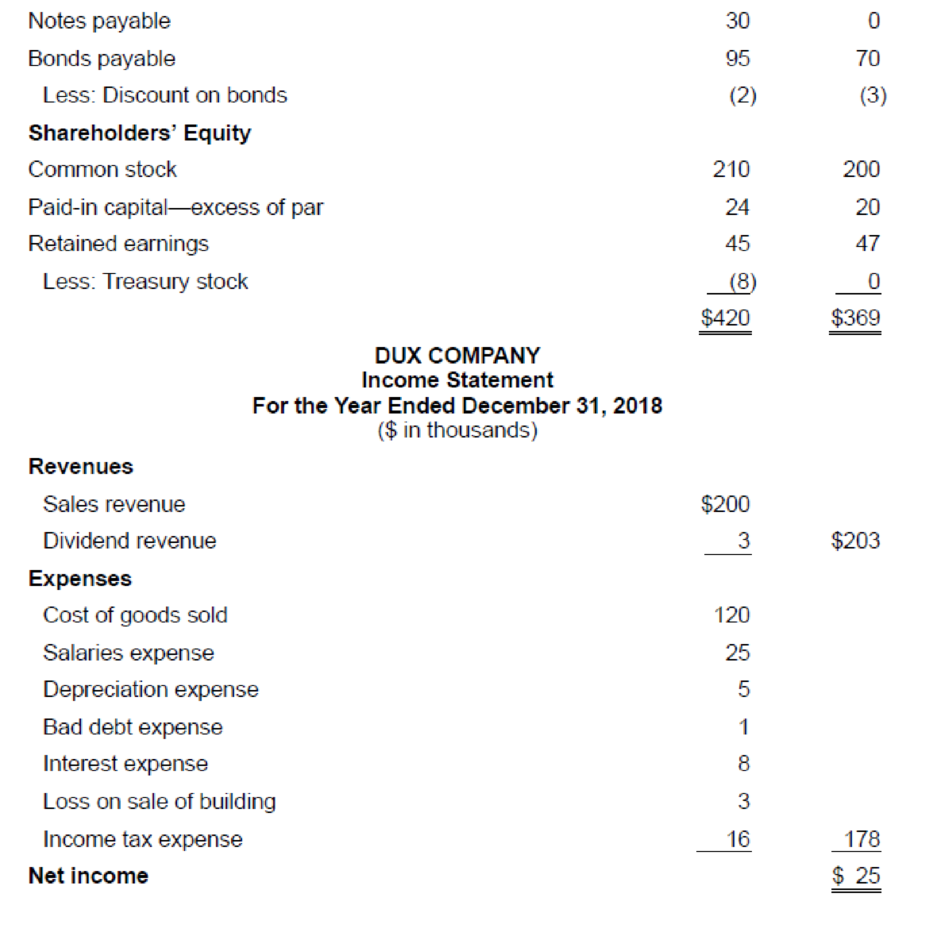

The comparative

Additional information from the accounting records:

a. A building that originally cost $40,000, and which was three-fourths

b. The common stock of Byrd Corporation was purchased for $5,000 as a long-term investment.

c. Property was acquired by issuing a 13%, seven-year, $30,000 note payable to the seller.

d. New equipment was purchased for $15,000 cash.

e. On January 1, 2018, bonds were sold at their $25,000 face value.

f. On January 19, Dux issued a 5% stock dividend (1,000 shares). The market price of the $10 par value common stock was $14 per share at that time.

g. Cash dividends of $13,000 were paid to shareholders.

h. On November 12, 500 shares of common stock were repurchased as

Required:

Prepare the statement of cash flows of Dux Company for the year ended December 31, 2018. Present cash flows from operating activities by the direct method. (You may omit the schedule to reconcile net income to cash flows from operating activities.)

Statement of cash flows: This statement reports all the cash transactions which are responsible for inflow and outflow of cash, and result of these transactions is reported as the ending balance of cash at the end of the accounting period.

Direct method:

This method uses the basis of cash for preparing the cash flows of statement.

Operating activities:

Operating activities refer to the normal activities of a company to carry out the business. The examples for operating activities are purchase of inventory, payment of salary, sales, and others.

Investing activities:

Investing activities refer to the activities carried out by a company for acquisition of long term assets. The examples for investing activities are purchase of equipment, long term investment, sale of land, and others.

Financing activities:

Financing activities refer to the activities carried out by a company to mobilize funds to carry out the business activities. The examples for financing activities are purchase of bonds, issuance of common shares, and others.

To prepare: The statement of cash flow of Company D under direct method for the year ended December 31, 2018.

Explanation of Solution

Spreadsheet:

The spreadsheet is a supplementary device which helps to prepare the adjusting entries and the statement of cash flows easier. The spreadsheet is a working tool of the accountant but it is not a permanent accounting record.

Spreadsheet for the Statement of cash flows of DUX Company:

| DUX Company | ||||

| Spreadsheet for the Statement of Cash Flows | ||||

| Amount in Millions | ||||

| Particulars | December 31,2017 Amount ($) | Changes | December 31,2018 Amount ($) | |

| Debit ($) | Credit ($) | |||

| Assets | ||||

| Assets | ||||

| Cash | 20 | (17) 13 | 33 | |

| Accounts receivable | 50 | (1) 2 | 48 | |

| Less: Allowance | (3) | (1) 1 | (4) | |

| Dividends receivable | 2 | (2) 1 | 3 | |

| Inventory | 50 | (3) 5 | 55 | |

| Long term investment | 10 | (10) 5 | 15 | |

| Land | 40 | (11) 30 X | 70 | |

| Buildings and equipment | 250 | (12) 15 | (7) 40 | 225 |

| Less: Acc. depreciation | (50) | (7) 30 | (5) 5 | (25) |

| Total assets | 369 | 420 | ||

| Liabilities and Stockholders’ Equity | ||||

| Liabilities | ||||

| Accounts payable | 20 | (3) 7 | 13 | |

| salaries payable | 5 | (4) 3 | 2 | |

| Interest payable | 2 | (6) 2 | 4 | |

| Income tax payable | 8 | (8) 1 | 7 | |

| Notes payable | 0 | X (11) 30 | 30 | |

| Bonds payable | 70 | (13) 25 | 95 | |

| Less: Discount on bonds | (3) | (6) 1 | (2) | |

| Stockholders’ equity | ||||

| Common Stock | 200 | (14) 10 | 210 | |

| Paid in capital –ex of par | 20 | (14) 4 | 24 | |

| Retained Earnings | 47 | (14) 14 | ||

| (15) 13 | (9) 25 | 45 | ||

| Less: Treasury stock | 0 | (16) 8 | (8) | |

| Total liabilities and stockholders’ equity | 369 | 420 | ||

| Income Statement | ||||

| Revenues | ||||

| Sales revenue | (1) 200 | 200 | ||

| Dividend revenue | (2) 3 | 3 | ||

| Expenses | ||||

| Cost of goods sold | (3) 120 | (120) | ||

| Salaries expense | (4) 25 | (25) | ||

| Depreciation expense | (5) 5 | (5) | ||

| Bad debt expense | (1) 1 | (1) | ||

| Interest expenses | (6) 8 | (8) | ||

| Loss on sale of building | (7) 3 | (3) | ||

| Income tax expense | (8) 16 | (16) | ||

| Net income | (9) 25 | 25 | ||

| Statement of Cash Flows | ||||

| Operating activities: | ||||

| Cash Inflows: | ||||

| From customers | (1) 202 | |||

| From dividends received | (2) 2 | |||

| Cash Outflows: | ||||

| To suppliers of goods | (3) 132 | |||

| To employees | (4) 28 | |||

| For interest | (6) 5 | |||

| For income taxes | (8) 17 | |||

| Net cash flows | 22 | |||

| Investing activities: | ||||

| Sale of building | (7) 7 | |||

| Purchase of long term investment | (10) 5 | |||

| Purchase of equipment | (12) 15 | |||

| Net cash flows | (13) | |||

| Financing activities: | ||||

| Sale of bonds payable | (13) 25 | |||

| Payment of cash dividends | (15) 13 | |||

| Purchase of treasury stock | (16) 8 | |||

| Net cash flows | 4 | |||

| Net increase in cash | (17) 13 | 13 | ||

| Total | 584 | 584 | ||

Table (1)

Note (X):

Purchase $30,000 worth of land by issuing a 13%, 7-year note is considered as non cash investing and financing activities.

The spreadsheet of Company D shows the analysis of cash flows in the reporting year 2018:

| DUX Company | ||

| Statement of Cash Flows (Direct Method) | ||

| Year Ended December 31, 2018 | ||

| Details | Amount ($) | Amount ($) |

| Cash flows from operating activities: | ||

| Cash inflows: | ||

| From customers | 202 | |

| From dividends received | 2 | |

| Cash outflows: | ||

| To suppliers of goods | (132) | |

| To employees | (28) | |

| For interest | (5) | |

| For income taxes | (17) | |

| Net cash flows from operating activities | 22 | |

| Cash flows from investing activities: | ||

| Sale of building | 7 | |

| Purchase of long-term investment | (5) | |

| Purchase of equipment | (15) | |

| Net cash flows from investing activities | (13) | |

| Cash flows from financing activities: | ||

| Sale of bonds payable | 25 | |

| Purchase of treasury stock | (8) | |

| Payment of cash dividends | (13) | |

| Net cash flows from financing activities | 4 | |

| Net increase in cash | 13 | |

| Cash balance, January 1, | 20 | |

| Cash balance, December 31, | 33 | |

Table (2)

Note (X):

| Schedule of Non Cash Investing and Financing Activities: | ||

| Purchase of land issuing notes payable | $30 |

Table (3)

Hence, the opening cash balance is $20 million and closing cash balance is $33 million.

Want to see more full solutions like this?

Chapter 21 Solutions

INTERMEDIATE ACCOUNTING (LL) W/CONNECT

- account questionsarrow_forwardcompared to the individual risks of constituting assets. Question 5 (6 marks) The common shares of Almond Beach Inc, have a beta of 0.75, offer a return of 9%, and have an historical standard deviation of return of 17%. Alternatively, the common shares of Palm Beach Inc. have a beta of 1.25, offer a return of 10%, and have an historical standard deviation of return of 13%. Both firms have a marginal tax rate of 37%. The risk-free rate of return is 3% and the expected rate of return on the market portfolio is 9½%. 1. Which company would a well-diversified investor prefer to invest in? Explain why and show all calculations. 2. Which company Would an investor who can invest in the shares of only one firm prefer to invest in? Explain why. RELEASED BY THE CI, MGMT2023, MARCH 2, 2025 5 Use the following template to organize and present your results: Theoretical CAPM Actual offered prediction for expected return (%) return (%) Standard deviation of return (%) Beta Almond Beach Inc. Palm Beach…arrow_forwardprovide correct answerarrow_forward

- Please solve. The screen print is kind of split. Please look carefully.arrow_forwardCoronado Fire, Inc. manufactures steel cylinders and nozzles for two models of fire extinguishers: (1) a home fire extinguisher and (2) a commercial fire extinguisher. The home model is a high-volume (54,000 units), half-gallon cylinder that holds 2 1/2 pounds of multi- purpose dry chemical at 480 PSI. The commercial model is a low-volume (10,200 units), two-gallon cylinder that holds 10 pounds of multi-purpose dry chemical at 390 PSI. Both products require 1.5 hours of direct labor for completion. Therefore, total annual direct labor hours are 96,300 or [1.5 hours x (54,000+10,200)]. Estimated annual manufacturing overhead is $1,566,090. Thus, the predetermined overhead rate is $16.26 or ($1,566,090 ÷ 96,300) per direct labor hour. The direct materials cost per unit is $18.50 for the home model and $26.50 for the commercial model. The direct labor cost is $19 per unit for both the home and the commercial models. The company's managers identified six activity cost pools and related…arrow_forwardCoronado Fire, Inc. manufactures steel cylinders and nozzles for two models of fire extinguishers: (1) a home fire extinguisher and (2) a commercial fire extinguisher. The home model is a high-volume (54,000 units), half-gallon cylinder that holds 2 1/2 pounds of multi- purpose dry chemical at 480 PSI. The commercial model is a low-volume (10,200 units), two-gallon cylinder that holds 10 pounds of multi-purpose dry chemical at 390 PSI. Both products require 1.5 hours of direct labor for completion. Therefore, total annual direct labor hours are 96,300 or [1.5 hours x (54,000+ 10,200)]. Estimated annual manufacturing overhead is $1,566,090. Thus, the predetermined overhead rate is $16.26 or ($1,566,090 ÷ 96,300) per direct labor hour. The direct materials cost per unit is $18.50 for the home model and $26.50 for the commercial model. The direct labor cost is $19 per unit for both the home and the commercial models. The company's managers identified six activity cost pools and related…arrow_forward

- The completed Payroll Register for the February and March biweekly pay periods is provided, assuming benefits went into effect as anticipated. Required: Using the payroll registers, complete the General Journal entries as follows: February 10 Journalize the employee pay. February 10 Journalize the employer payroll tax for the February 10 pay period. Use 5.4 percent SUTA and 0.6 percent FUTA. No employees will exceed the FUTA or SUTA wage base. February 14 Issue the employee pay. February 24 Journalize the employee pay. February 24 Journalize the employer payroll tax for the February 24 pay period. Use 5.4 percent SUTA and 0.6 percent FUTA. No employee will exceed the FUTA or SUTA wage base. February 28 Issue the employee pay. February 28 Issue payment for the payroll liabilities. March 10 Journalize the employee pay. March 10 Journalize the employer payroll tax for the March 10 pay period. Use 5.4 percent SUTA and 0.6 percent FUTA. No employees will exceed the FUTA or SUTA wage base.…arrow_forwardPlease given step by step explanation general accounting questionarrow_forwardDon't use ai solution please given answer general accountingarrow_forward

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning Financial Reporting, Financial Statement Analysis...FinanceISBN:9781285190907Author:James M. Wahlen, Stephen P. Baginski, Mark BradshawPublisher:Cengage Learning

Financial Reporting, Financial Statement Analysis...FinanceISBN:9781285190907Author:James M. Wahlen, Stephen P. Baginski, Mark BradshawPublisher:Cengage Learning Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning