Concept explainers

Videos

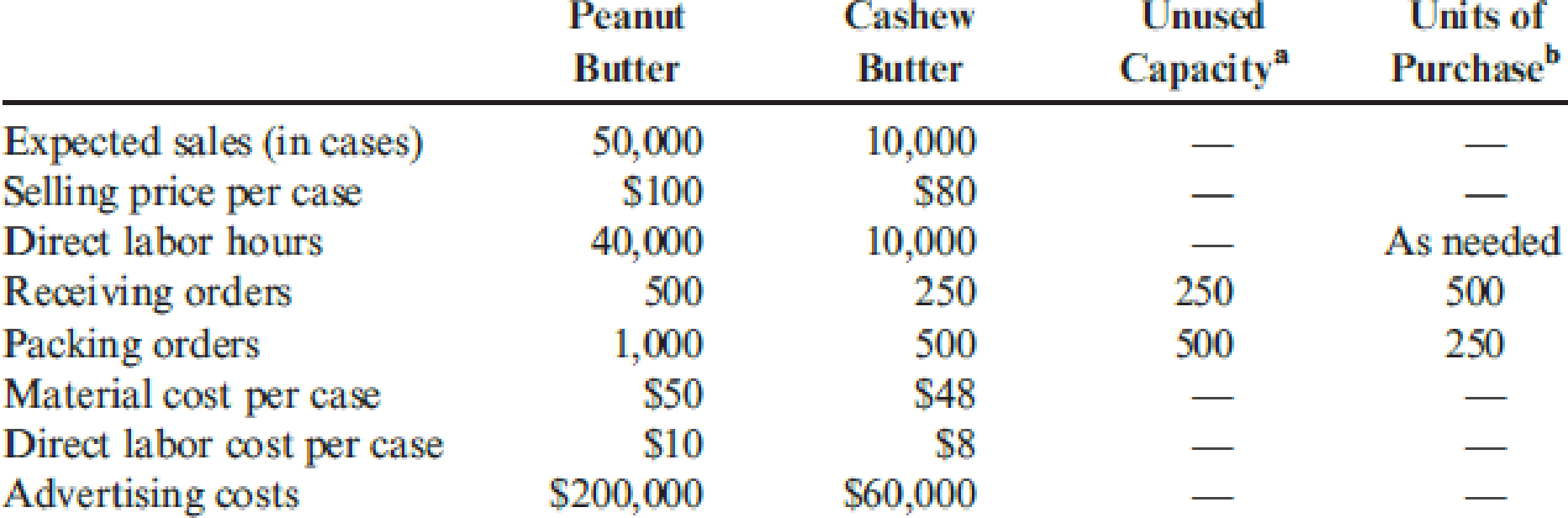

Nutterco, Inc., produces two types of nut butter: peanut butter and cashew butter. Of the two, peanut butter is the more popular. Cashew butter is a specialty line using smaller jars and fewer jars per case. Data concerning the two products follow:

aPractical capacity less expected usage (all unused capacity is permanent).

bIn some cases, activity capacity must be purchased in steps (whole units). These steps are provided as necessary. The cost per step is the fixed activity rate multiplied by the step units. The fixed activity rate is the expected fixed activity costs divided by practical activity capacity.

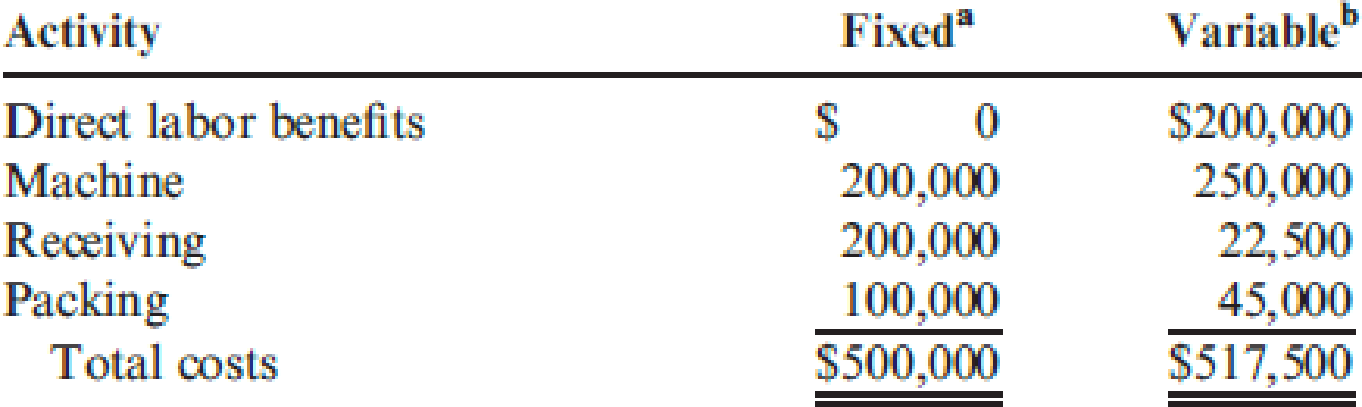

Annual overhead costs are listed below. These costs are classified as fixed or variable with respect to the appropriate activity driver.

aCosts associated with practical activity capacity. The machine fixed costs are all

bThese costs are for the actual levels of the cost driver.

Required:

- 1. Prepare a traditional segmented income statement, using a unit-level overhead rate based on direct labor hours. Using this approach, determine whether the cashew butter product line should be kept or dropped.

- 2. Prepare an activity-based segmented income statement. Repeat the keep-or-drop analysis using an ABC approach.

1.

Prepare a traditional segmented income statement of company N, under a unit-level overhead rate and state whether the cashew butter product line should be kept or dropped.

Explanation of Solution

Tactical decision making: Tactical decision making is a process in which the company can choose the correct alternative based on the profitability. In tactical decision making, offer price of a product is compared with the normal selling price and offer price less than the normal selling price of product is considered as the idle capacity for decision making.

| Particulars | Peanut Butter (A) (1) | Cashew Butter (2) (B) |

Total |

| Revenues | $5,000,000 | $800,000 | $5,800,000 |

| Less: variable expenses | |||

| Direct materials | 2,500,000 | 480,000 | 2,980,000 |

| Direct labor | 500,000 | 80,000 | 580,000 |

| Variable overhead | 360,000 | 90,000 | 450,000 |

| Contribution margin | $1,640,000 | $150,000 | $1,790,000 |

| Less: Direct fixed expenses | $200,000 | $60,000 | $260,000 |

| Product margin | $1,440,000 | $90,000 | $1,530,000 |

| Less: Common fixed expenses | 567,500 (4) | ||

| Segment margin | $962,500 |

Table (1)

Working note (1):

Compute the amounts of revenues and expenses of Peanut Butter:

| Particulars | Costs per cases for Peanut butter (A) | Sales units (B) | Peanut Butter |

| Revenues | $100 | 50,000 | $5,000,000 |

| Less: variable expenses | |||

| Direct materials | $50 | 50,000 | $2,500,000 |

| Direct labor | $10 | 50,000 | 500,000 |

| Variable overhead | $9 (2) | 40,000 | 360,000 |

Table (2)

Working note (2):

Compute the variable overhead rate:

Working note (3):

Compute the amounts of revenues and expenses of Peanut Butter:

| Particulars | Costs per cases for cashew butter (A) | Sales units (B) | Cashew Butter |

| Revenues | $80 | 10,000 | $800,000 |

| Less: variable expenses | |||

| Direct materials | $48 | 10,000 | $480,000 |

| Direct labor | $8 | 10,000 | 80,000 |

| Variable overhead | $9 (2) | 10,000 | 90,000 |

Table (3)

Working note (4):

Compute the common fixed expenses:

Therefore, the company should not drop the cashew butter because the segment margin is positive.

2.

Prepare an activity-based segmented income statement of company N, under ABC approach and state whether the cashew butter product line should be kept or dropped.

Explanation of Solution

Prepare an activity-based segmented income statement of company N, under ABC approach and state whether the cashew butter product line should be kept or dropped as follows:

| Particulars | Peanut Butter (A) (1) | Cashew Butter (2) (B) | Total |

| Revenues | $5,000,000 | $800,000 | $5,800,000 |

| Less: variable expenses | |||

| Direct materials | 2,500,000 | 480,000 | 2,980,000 |

| Direct labor | 500,000 | 80,000 | 580,000 |

| Variable overhead | 360,000 | 90,000 | 450,000 |

| Contribution margin | $1,640,000 | $150,000 | $1,790,000 |

| Less: Traceable expenses | |||

| Advertising | $200,000 | $60,000 | $260,000 |

| Receiving | 115,000 (7) | 57,500 (8) | 172,500 |

| Packing | 80,000 (11) | 40,000 (12) | 120,000 |

| Product margin | $1, 245,000 | $(7,500) | $1,237,500 |

| Less: Unused activity expenses | 567,500 | ||

| Receiving (13) | 50,000 | ||

| Packing (14) | 25,000 | ||

| Less: Machine depreciation expenses | (200,000) | ||

| Segment margin | $962,500 |

Table (4)

From the above calculation it is clear that dropping the cashew butter line is better because the product margin of the cashew butter is showing a negative margin of $7,500.

Working note (5):

Compute the fixed receiving rate:

Working note (6):

Compute the variable receiving rate:

Working note (7):

Compute the receiving expenses of peanut butter:

Working note (8):

Compute the receiving expenses of cashew butter:

Working note (9):

Compute the fixed packaging rate:

Working note (10):

Compute the variable packaging rate:

Working note (11):

Compute the packaging expenses of peanut butter:

Working note (12):

Compute the packaging expenses of cashew butter:

Working note (13):

Compute the unused receiving expenses:

Working note (14):

Compute the unused packing expenses:

Want to see more full solutions like this?

Chapter 17 Solutions

Cornerstones of Cost Management (Cornerstones Series)

- If DF sells three Masoline for each Aldernite, how many doors of each type would it produce and sell? What would be the total contribution margin?arrow_forwardThe following Information applies to the products of Baird Company. Selling price per unit Variable cost per unit Identify the product that should be produced or sold under each of the following constraints. Consider each constraint separately. Required a. One unit of Product A requires 4 hours of labor to produce, and one unit of Product B requires 10 hours of labor to produce. Due to labor constraints, demand is higher than the company's capacity to make both products. b. The products are sold to the public in retail stores. The company has limited floor space and cannot stock as many products as it would like. Display space is available for only one of the two products. Expected sales of Product A and Product B are 12,000 units and 10,000 units, respectively. c. The maximum number of machine hours available is 38,000. Product A uses 2 machine hours, and Product B uses 5 machine hours. The company can sell all the products it produces. Required A Product A $ 16 12 Complete this…arrow_forwardThe Conti Company is decentralized, and divisions are considered investment contors. Con has one division that manufactures oak dining room chairs with upholstered seat cushions. The Chair Division cuts, assembles, and finishes the cak chairs and then purchases and attaches the seat cushions (Click the icon to view additional information) Read the requirements Requirement 3. Assume the Chair Division purchases the 900 cushions needed from the Cushion Division at its current variable cost. What is the total contribution margin for each division and the company? (Enter "0" for any zero amounts) Number of units Contribution margin per unt Total contribution margin Cushion Division Total Requirement 4. Review your answers for Requirements 1, 2, and 3. What is the best option for Con Company? The best option for Cois in total contribution margin than if the duson purchanchons inveraly By having the Chair Division purchase the cushions from a in outside vendor, the company would get…arrow_forward

- The Cycle Division of Sheffield Company has the following unit data related to its most recent cycle, the Roadbuster. Selling price Variable cost of goods sold Body frame Other variable costs Contribution margin (a) Your answer is correct. (b) $330 990 Presently, the Cycle Division buys its body frames from an outside supplier. However Sheffield has another division, FrameBody, that makes body frames for other cycle companies. The Cycle Division believes that FrameBody's product is suitable for its new Roadbuster cycle. Presently, FrameBody sells its frames for $385 per frame. The variable cost for FrameBody is $291. The Cycle Division is willing to pay $299 to purchase the frames from FrameBody. Assume that FrameBody has excess capacity and is able to meet all of the Cycle Division's needs. If the Cycle Division buys 1,100 frames from FrameBody, determine the following: (Enter negative amounts using either a negative sign preceding the number e.g. -45 or parentheses e.g. (45).) (2)…arrow_forwardBurger Office Equipment produces two types of desks, standard and deluxe. Deluxe desks have oak tops and more expensive hardware and require additional time for finishing and polishing. After reviewing the hardware and labor required along with the profit for each model, Burger Office Equipment found the following linear optimization model for profit, where S is the number of standard desks produced and D is the number of deluxe desks produced. Implement the linear optimization model on a spreadsheet and use Solver to find an optimal solution. Interpret the optimal solution, identify the binding constraints, and verify the values of the slack variables. Maximize Profit=240 S+350 D 65 S+45 D≤6000 20 D≤ 800 (Availability of pine) 9 S+18 D≤500 S≥0 and D≥0 (Availability of oak) (Availability of labor) Implement the linear optimization model and find an optimal solution. Interpret the optimal solution. The optimal solution is to produce standard desks and deluxe desks. This solution gives…arrow_forwardPart A KM Sdn. Bhd. (KM) produces two different types of high quality handbags, Luxury and Superior. Each design is made in small batches. The bags are all made on the same special equipment that is expected to operate at capacity. The equipment must be switched over to a new design and set up to prepare for the production of each batches of products. When completed, each batch of products is immediately shipped to a wholesaler. Shipping costs vary with the number of shipments. KM uses activity-based costing and provides the following budgeted information for the year ended 31 December 2017: Luxury (RM) Total (RM) Superior (RM) 412,920 120,000 Direct material Direct labour Manufacturing overhead: Set up Shipping Design Plant utilities and administration Total 379,290 98,000 792,210 218,000 65,930 73,910 166,000 243,000 1,559,050 Other information follows: Luxury 6,050 1,450 130 Superior 3,350 2,600 60 Total Number of bags Hours of production Number of batches Number of designs 9,400…arrow_forward

- a) Classify each cost element as either fixed, variable, or mixed b) Calculate:i) the variable production cost per unit and the total fixed production overhead.ii) The total variable cost per unit and the total fixed costs Hint: Use the high-low method to separate mixed costs into their fixed and variable components.arrow_forwardCopdogarrow_forwardHaving trouble with some questions from the last chapter.arrow_forward

- Good Scent, Inc., produces two colognes: Rose and Violet. Of the two, Rose is more popular. Data concerning the two products follow: Rose Violet Expected sales (in cases) Selling price per case Direct labor hours Machine hours Receiving orders Packing orders Material cost per case Direct labor cost per case $9 The company uses a conventional costing system and assigns overhead costs to products using direct labor hours. Annual overhead costs follow. They are classified as fixed or variable with respect to direct labor hours. Fixed Direct labor benefits Machine costs Receiving department Packing department Total costs * All depreciation 55,000 11,000 $101 36,650 5,550 10,350 3,200 $ 50 - 97 $49 $82 27 53 Variable $215,220 218,500* 291,180 241,000 126,000 $585,500 $506,400 $42 $6 Required: 1. Using the conventional approach, compute the number of cases of Rose and the number of cases of Violet that must be sold for the company to break even. In your computations, round variable unit cost…arrow_forwardAn automated turning machine is the current constraint at Jordison Corporation. Three products use this constrained resource. Data concerning those products appear below: Selling price per unit Variable cost per unit Minutes on the constraint Multiple Choice O Rank the products in order of their current profitability from most profitable to least profitable. In other words, rank the products in the order in which they should be emphasized. (Round your intermediate calculations to 2 decimal places.) O JQ, RQ, LN RQ, LN, JQ RQ, JQ, LN LN $160.46 $ 106.40 3.40 LN, JQ, RQ JQ $ 346.18 $ 281.70 5.20 RQ $ 409.29 $ 311.25 8.60arrow_forwardRakesharrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning