Concept explainers

Videos

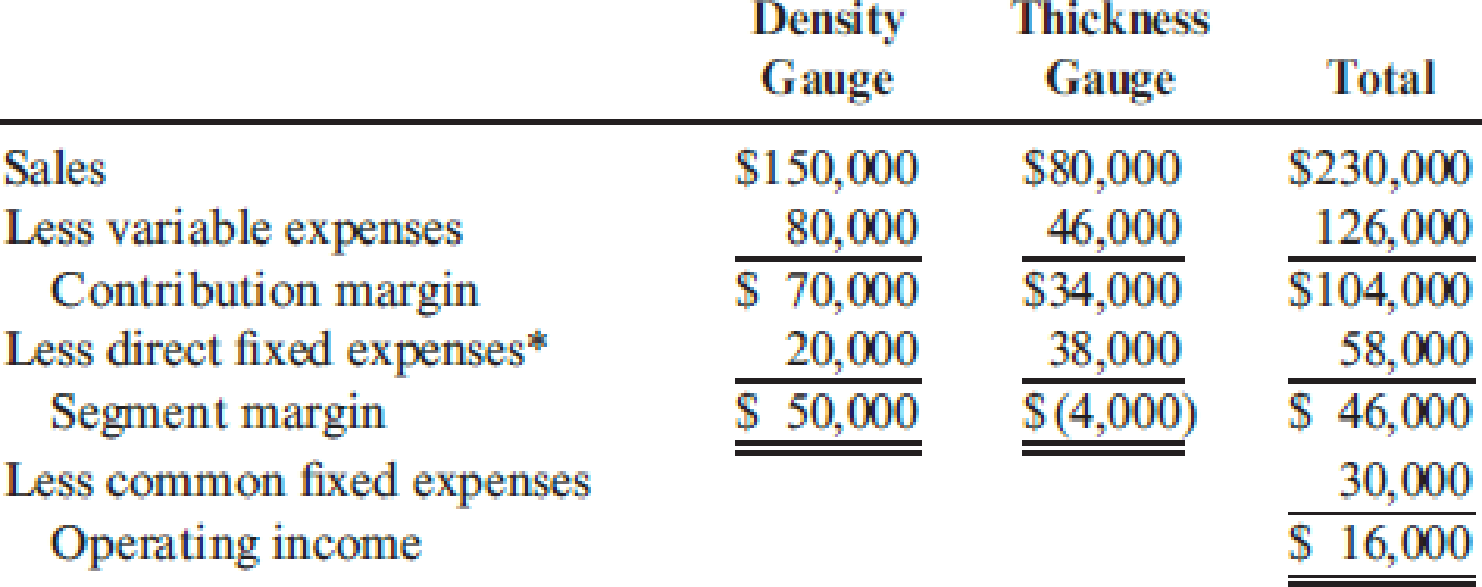

Morrill Company produces two different types of gauges: a density gauge and a thickness gauge. The segmented income statement for a typical quarter follows.

*Includes

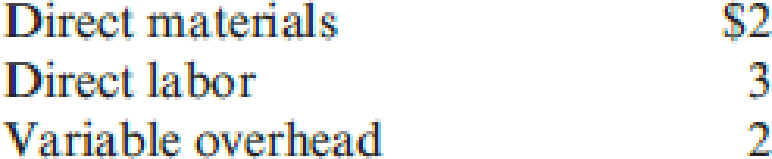

The density gauge uses a subassembly that is purchased from an external supplier for $25 per unit. Each quarter, 2,000 subassemblies are purchased. All units produced are sold, and there are no ending inventories of subassemblies. Morrill is considering making the subassembly rather than buying it. Unit-level variable

No significant non-unit-level costs are incurred.

Morrill is considering two alternatives to supply the productive capacity for the subassembly.

- 1. Lease the needed space and equipment at a cost of $27,000 per quarter for the space and $10,000 per quarter for a supervisor. There are no other fixed expenses.

- 2. Drop the thickness gauge. The equipment could be adapted with virtually no cost and the existing space utilized to produce the subassembly. The direct fixed expenses, including supervision, would be $38,000, $8,000 of which is depreciation on equipment. If the thickness gauge is dropped, sales of the density gauge will not be affected.

Required:

- 1. Should Morrill Company make or buy the subassembly? If it makes the subassembly, which alternative should be chosen? Explain and provide supporting computations.

- 2. Suppose that dropping the thickness gauge will decrease sales of the density gauge by 10 percent. What effect does this have on the decision?

- 3. Assume that dropping the thickness gauge decreases sales of the density gauge by 10 percent and that 2,800 subassemblies are required per quarter. As before, assume that there are no ending inventories of subassemblies and that all units produced are sold. Assume also that the per-unit sales price and variable costs are the same as in Requirement 1. Include the leasing alternative in your consideration. Now, what is the correct decision?

1.

Describe whether company M should make or buy the subassembly. Assume that the company has to choose the making decision, state the alternative that should be chosen and provide the supporting calculations.

Explanation of Solution

Tactical decision making: Tactical decision making is a process in which the company can choose the correct alternative based on the profitability. In tactical decision making, offer price of a product is compared with the normal selling price and offer price less than the normal selling price of product is considered as the idle capacity for decision making.

Indicate whether company M should make or buy the subassembly:

| Particulars | Lease and make | Buy |

| Purchase cost (1) | $0 | $50,000 |

| Variable manufacturing cost (2) | $14,000 | $0 |

| Lease expense | $27,000 | $0 |

| Supervisor salary | $10,000 | $0 |

| Total relevant cost | $51,000 | $51,000 |

Table (1)

If company has chosen the make decision, which alternative should be chosen:

| Particulars | Drop thickness gauge and make |

| Purchase cost (1) | $0 |

| Variable manufacturing cost (2) | $14,000 |

| Lost contribution margin | $34,000 |

| Total relevant cost | $48,000 |

Table (2)

Note: The direct fixed expense is same for all alternatives.

In this case, the company should choose the making decision because the subassembly would produce more income than the thickness gauge.

Working note (1):

Calculate the purchase cost of subassembly.

Working note (2):

Calculate the variable manufacturing cost.

2.

State the effect of the given decision; assume that dropping the thickness gauge decreases the sale of density gauge by 10%.

Explanation of Solution

State the effect of the decision if dropping in thickness gauge will decreases the sale of density gauge by 10% as follows:

| Particulars | Make | Buy |

| Lost sales for density gauge (3) | $15,000 | $0 |

| Cost of making component (4) | $12,600 | $0 |

| Less: Reduction of other variable costs (5) | ($3,000) | $0 |

| Purchase cost (1) | $34,000 | $50,000 |

| Total relevant cost | $58,600 | $50,000 |

Table (3)

If company is choose buy alternative, then the sales volume is not reduced and the same number of components would be needed for the production process.

Working note (3):

Calculate the lost sales for density gauge.

Working note (4):

Calculate the cost of making component.

Working note (5):

Calculate the other variable cost.

3.

Indicate the correct decision for the given situation.

Explanation of Solution

Indicate the correct decision for the given situation as follows:

| Particulars | Lease and make | Buy |

| Purchase cost (6) | $0 | $70,000 |

| Variable manufacturing cost (7) | $19,600 | $0 |

| Lease expense | $27,000 | $0 |

| Supervisor salary | $10,000 | $0 |

| Total relevant cost | $56,600 | $70,000 |

Table (4)

If the dropping the thickness gauge decreases the sales of density gauge by 10%:

| Particulars | Drop thickness gauge and make |

| Purchase cost | $0 |

| Lost sales from density gauge (3) | $15,000 |

| Variable manufacturing cost (8) | $17,640 |

| Less: Other variable cost (9) | ($1,000) |

| Lost contribution margin | $34,000 |

| Total relevant cost | $65,640 |

Table (5)

Note: The direct fixed expense is same for all alternatives.

In this case, the company should make the component because the total relevant cost of making decision ($56,600) is less than the buying decision ($70,000) and dropping the thickness gauges ($65,640).

Working note (6):

Calculate the purchase cost of subassembly.

Working note (7):

Calculate the variable manufacturing cost.

Working note (8):

Calculate the cost of making component.

Working note (9):

Calculate the other variable cost.

Want to see more full solutions like this?

Chapter 17 Solutions

Cornerstones of Cost Management (Cornerstones Series)

- Petoskey Company produces three products: Alanson, Boyne, and Conway. A segmented income statement, with amounts given in thousands, follows: Direct fixed expenses consist of depreciation and plant supervisory salaries. All depreciation on the equipment is dedicated to the product lines. None of the equipment can be sold. Refer to the information for Petoskey Company from Exercise 8-44. Assume that 20% of the Alanson customers choose to buy from Petoskey because it offers a full range of products, including Conway. If Conway were no longer available from Petoskey, these customers would go elsewhere to purchase Alanson. Required: Conceptual Connection Estimate the impact on profit that would result from dropping Conway. Explain why Petoskey should keep or drop Conway.arrow_forwardLowwater Sailmakers manufactures sails for sailboats. The company has the capacity to produce 25,000 sails per year, but is currently producing and selling 20,.000 sails per year, The following information relates to current production. If a special sales order is accepted for 2,000 sails at a price of $87 per unit, and fixed costs increase by $20,000, how would operating income be affected? (NOTE: Assume regular sales are not affected by the special order.) Sale price per unit $150 Variable costs unit: per Manufacturing Marketing and administrative $60 $20 Total fixed costs: Manufacturing Marketing and administrative S600,000 $200 000 Increase by S14,000 Decrease by S4,000 ) Decrease by S14,000 ) Decrease by S6,000 () Increase by S6,000 ()arrow_forwardCox Electric makes electronic components and has estimated the following for a new design of one of its products. Fixed cost = $23,750 • Material cost per unit = $0.17 • Labor cost per unit = $0.11 • Revenue per unit = $0.66 Note that fixed cost is incurred regardless of the amount produced. Per-unit material and labor cost together make up the variable cost per unit. Assuming that Cox Electric sells all that it produces, profit is calculated by subtracting the fixed cost and total variable cost from total revenue. Construct an appropriate spreadsheet model to find the profit based on a given production level and use the spreadsheet model to answer these questions. (a) Construct a one-way data table with production volume as the column input and profit as the output. Breakeven occurs when profit goes from a negative to a positive value; that is, breakeven is when total revenue = the total cost, yielding a profit of zero. Vary production volume from 0 to 100,000 in increments of 10,000.…arrow_forward

- The process-control division expects to sell 1,250 process-control units this year. From the viewpoint of Sierra Inc. as a whole, should 1,250 Xcel-chips be transferred to the process-control division to replace circuit boards? Show your computations.arrow_forwardTasty, Inc., is a producer of potato chips. A single production process at Tasty, Inc., yields potato chips as the main product and a byproduct that can also be sold as snack. Both products are fully processed by the splitoff point, and there are no separable costs. For September 2022, the cost of operation is $300,000. Production and sales data are as follows: Main Product: Potato Chips Byproduct Production (in pounds) Sales (in pounds) Main products: Byproducts: 80,000 8,000 72,000 6,000 Selling Price per Pound There were no beginning inventories on September 1, 2022. What are the inventory costs reported in the balance sheet on September 30, 2022, for the main product and byproduct under the production method and the sales method of byproduct accounting? The production method $20 $5 The sales methodarrow_forwardThis Little Light, Inc. is a manufacturer of lamps. Little Light makes 40,000 units per year of a part that it uses in the manufacturing of each lamp. At this activity level, the unit production cost is $7.17. Of this amount, $4.71 is for unit variable production costs. The remainder is for fixed production costs and equals $98,400. Little Light has identified an outsider supplier who sells the needed part. If the part is purchased from the outsider supplier, 15% of Little Light's fixed manufacturing costs will be eliminated. Assume Little Light will need 50,000 of the part next year and that the freed up capacity can be rented out to another company for $31,740. At what purchase price will Little Light be economically indifferent between making the part and buying the part? $4.70 $4.86 $5.97 $5.50 $5.64arrow_forward

- Jonfran Company manufactures three different models of paper shredders including the waste container, which serves as the base. While the shredder heads are different for all three models, the waste container is the same. The number of waste containers that Jonfran will need during the following years is estimated as follows: The equipment used to manufacture the waste container must be replaced because it is broken and cannot be repaired. The new equipment would have a purchase price of 945,000 with terms of 2/10, n/30; the companys policy is to take all purchase discounts. The freight on the equipment would be 11,000, and installation costs would total 22,900. The equipment would be purchased in December 20x4 and placed into service on January 1, 20x5. It would have a five-year economic life and would be treated as three-year property under MACRS. This equipment is expected to have a salvage value of 12,000 at the end of its economic life in 20x9. The new equipment would be more efficient than the old equipment, resulting in a 25 percent reduction in both direct materials and variable overhead. The savings in direct materials would result in an additional one-time decrease in working capital requirements of 2,500, resulting from a reduction in direct material inventories. This working capital reduction would be recognized at the time of equipment acquisition. The old equipment is fully depreciated and is not included in the fixed overhead. The old equipment from the plant can be sold for a salvage amount of 1,500. Rather than replace the equipment, one of Jonfrans production managers has suggested that the waste containers be purchased. One supplier has quoted a price of 27 per container. This price is 8 less than Jonfrans current manufacturing cost, which is as follows: Jonfran uses a plantwide fixed overhead rate in its operations. If the waste containers are purchased outside, the salary and benefits of one supervisor, included in fixed overhead at 45,000, would be eliminated. There would be no other changes in the other cash and noncash items included in fixed overhead except depreciation on the new equipment. Jonfran is subject to a 40 percent tax rate. Management assumes that all cash flows occur at the end of the year and uses a 12 percent after-tax discount rate. Required: 1. Prepare a schedule of cash flows for the make alternative. Calculate the NPV of the make alternative. 2. Prepare a schedule of cash flows for the buy alternative. Calculate the NPV of the buy alternative. 3. Which should Jonfran domake or buy the containers? What qualitative factors should be considered? (CMA adapted)arrow_forwardYum, Inc. is a producer of potato chips. A single production process at Yum, Inc., yields potato chips as the main product, as well as a byproduct that can be sold as a snack. Both products are fully processed by the splitoff point, and there are no separable costs. For September 2020, the cost of operations is $485,000. Production and sales data are as follows: Note: There were no beginning inventories on September 1, 2020. Requirements Dialog content starts 1. What is the gross margin forbYum,Inc., under the production method and the sales method of byproduct accounting? 2. What are the inventory costs reported in the balance sheet on September 30, 2020, for the main product and byproduct under the two methods of byproduct accounting in requirement 1? 3. Prepare the journal entries to record the byproduct activities under (a) the production method and (b) the sales method. Briefly discuss the effects on the financial statements.arrow_forwardCox Electric makes electronic components and has estimated the following for a new design of one of its products: Fixed cost = $10,000 Material cost per unit = $ 0.15 Labor cost per unit = $ 0.10 Revenue per unit = $ 0.65 These data are given in the file CoxElectric. Note that fixed cost is incurred regardless of the amount produced. Per-unit material and labor cost together make up the variable cost per unit. Assuming Cox Electric sells all that it produces, profit is calculated by subtracting the fixed cost and total variable cost rom total revenue. Create a spreadsheet model and construct a 1-way table and determine the breakeven point (use intervals of 10,000 units). Group of answer choices 20,000 - 30,000 10,000 - 20,000 30,000 - 40,000 25,000 30,000 20,000arrow_forward

- Parker Pottery produces a line of vases and a line of ceramic figurines. Each line uses the sameequipment and labor; hence, there are no traceable fixed costs. Common fixed cost equals$30,000. Parker’s accountant has begun to assess the profitability of the two lines and has gathered the following data for last year: Required:1. Compute the number of vases and the number of figurines that must be sold for thecompany to break even.2. Parker Pottery is considering upgrading its factory to improve the quality of its products.The upgrade will add $5,260 per year to total fixed cost. If the upgrade is successful, theprojected sales of vases will be 1,500, and figurine sales will increase to 1,000 units. Whatis the new break-even point in units for each of the products?arrow_forwardCrispy, Inc. is a producer of potato chips. A single production process at Crispy, Inc., yields potato chips as the main product, as well as a byproduct that can be sold as a snack. Both products are fully processed by the splitoff point, and there are no separable costs. For September 2020, the cost of operations is $520,000. Production and sales data are as follows: (Click the icon to view the production and sales data.) Data table Potato Chips Byproduct Production (in pounds) Sales (in pounds) 46,000 8,200 Deduct value of byproduct production Print 34,960 $ 5,000 $ Done Selling Price per pound 26 5 X There were no beginning inventories on September 1, 2020. Read the requirements. Requirements 1. What is the gross margin for Crispy, Inc., under the production method and the sales method of byproduct accounting? 2. What are the inventory costs reported in the balance sheet on September 30, 2020, for the main product and byproduct under the two methods of byproduct accounting in…arrow_forwardCox Electric makes electronic components and has estimated the following for a new design of one of its products. Fixed cost = $12,350 • Material cost per unit = $0.16 •Labor cost per unit = $0.12 •Revenue per unit = $0.66 Note that fixed cost is incurred regardless of the amount produced. Per-unit material and labor cost together make up the variable cost per unit. Assuming that Cox Electric sells all that it produces, profit is calculated by subtracting the fixed cost and total variable cost from total revenue. Construct an appropriate spreadsheet model to find the profit based on a given production level and use the spreadsheet model to answer these questions. (a) Construct a one-way data table with production volume as the column input and profit as the output. Breakeven occurs when profit goes from a negative to a positive value; that is, breakeven is when total revenue = the total cost, yielding a profit of zero. Vary production volume from 0 to 100,000 in increments of 10,000.…arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning