Principles Of Economics 2e

2nd Edition

ISBN: 9781680920864

Author: Timothy Taylor, Steven A. Greenlaw, David Shapiro

Publisher: MCGRAW-HILL HIGHER EDUCATION

expand_more

expand_more

format_list_bulleted

Textbook Question

Chapter 12, Problem 11SCQ

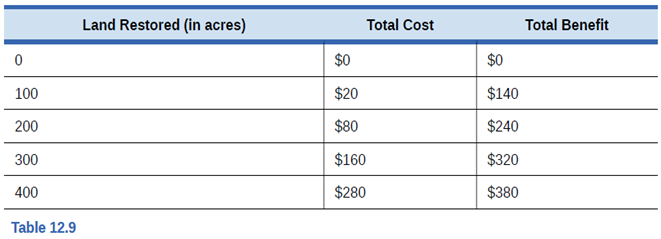

The state of Colorado requires oil and gas companies who use fracking techniques to retune the land to its original condition after the oil and gas extractions. Table 12.9 shows the total cost and total benefits (in dollars) of this policy.

- Calculate the marginal cost and the marginal benefit at each quantity (acre) of land restored. See Production. Costs and Industry Structure if you need a refresher on how to calculate marginal costs and benefits.

- If we apply marginal analysis, what is the optimal amount of land to be restored?

Expert Solution & Answer

Trending nowThis is a popular solution!

Students have asked these similar questions

Only human experts solved it. Direction: Do a total of 5 of this, instruction and the topic is provided in the picture. Strictly write this in bond paper.

NOTE: strictly use nautical almanac. This is about maritime navigation.

not use ai please

Use the following table to work Problems 5 to 9.

Minnie's Mineral Springs, a single-price monopoly,

faces the market demand schedule:

Price

Quantity demanded

(dollars per bottle)

10

8

(bottles per hour)

0

1

6

2

4

3

2

4

0

5

5. a. Calculate Minnie's total revenue schedule.

b. Calculate its marginal revenue schedule.

6. a. Draw a graph of the market demand curve

and Minnie's marginal revenue curve.

b. Why is Minnie's marginal revenue less than

the price?

7. a. At what price is Minnie's total revenue maxi-

mized?

b. Over what range of prices is the demand for

water from Minnie's Mineral Springs elastic?

8. Why will Minnie not produce a quantity at which

the market demand for water is inelastic?

Chapter 12 Solutions

Principles Of Economics 2e

Ch. 12 - Identify the following situations as an example of...Ch. 12 - Identify whether the market supply curve will...Ch. 12 - For each of your answers to Exercise 12.2, will...Ch. 12 - Table 12.5 provides the supply and demand...Ch. 12 - Consider two approaches to reducing emissions of...Ch. 12 - Classify the following pollution-control policies...Ch. 12 - An emissions tax on a quantity of emissions from a...Ch. 12 - Four films called Elm, Maple, Oak, and (Shelly,...Ch. 12 - The rows in Table 12.7 show three market-oriented...Ch. 12 - Suppose a city releases 16 million gallons of raw...

Ch. 12 - The state of Colorado requires oil and gas...Ch. 12 - Consider the case of global environmental problems...Ch. 12 - A country called Sherwood is very heavily covered...Ch. 12 - What is an externality?Ch. 12 - Give an example of a positive externality and an...Ch. 12 - What is the difference between private costs and...Ch. 12 - In a market without environmental regulations,...Ch. 12 - What is command-and-control environmental...Ch. 12 - What are the three problems that economists have...Ch. 12 - What is a pollution charge and what incentive does...Ch. 12 - What is a marketable permit and what incentive...Ch. 12 - What are better-defined property rights and what...Ch. 12 - As the extent of environmental protection expands,...Ch. 12 - As the extent of environmental protection expands,...Ch. 12 - What are the economic tradeoffs between low-income...Ch. 12 - What arguments d0 low-income countries make in...Ch. 12 - In the tradeoff between economic output and...Ch. 12 - What does a point inside the production...Ch. 12 - Suppose you want to put a dollar value on the...Ch. 12 - Would environmentalists favor command-and-control...Ch. 12 - Consider two ways of protecting elephants from...Ch. 12 - Will a system of marketable permits work with...Ch. 12 - Is zero pollution possible under a marketable...Ch. 12 - Is zero pollution an optimal goal? Way or why not?Ch. 12 - From an economic perspective, is it sound policy...Ch. 12 - Recycling is a relatively inexpensive solution to...Ch. 12 - Can extreme levels of pollution hurt the economic...Ch. 12 - How can high-income countries benefit from...Ch. 12 - Technological innovations shift the production...Ch. 12 - Show the market for cigarettes in equilibrium,...Ch. 12 - Refer to Table 12.2. The externality created by...Ch. 12 - Table 12.12, shows the supply and demand...Ch. 12 - A city currently emits 15 million gallons (MG) of...Ch. 12 - In the Land of Purity, there is only one form of...

Additional Business Textbook Solutions

Find more solutions based on key concepts

Whether the stocks outperform, underperform or have the same return as a buy and hold strategy. Introduction: A...

Corporate Finance (4th Edition) (Pearson Series in Finance) - Standalone book

5. Which inventory costing method results in the lowest net income during a period of rising inventory costs?

W...

Horngren's Financial & Managerial Accounting, The Financial Chapters (Book & Access Card)

To what does the lifetime value of the customer refer, and how is it calculated?

MARKETING:REAL PEOPLE,REAL CHOICES

11-13. Discuss how your team is going to identify the existing competitors in your chosen market. Based on the ...

Business Essentials (12th Edition) (What's New in Intro to Business)

E6-14 Using accounting vocabulary

Learning Objective 1, 2

Match the accounting terms with the corresponding d...

Horngren's Accounting (12th Edition)

What is a qualitative forecasting model, and when is its use appropriate?

Operations Management

Knowledge Booster

Similar questions

- Not use ai pleasearrow_forwardThe Firm's Output Decision (Study Plan 12.2) Use the following table to work Problems 4 to 6. Pat's Pizza Kitchen is a price taker. Its costs are Output (pizzas per hour) Total cost (dollars per hour) 0 10 1 21 2 30 3 41 4 54 5 69 4. Calculate Pat's profit-maximizing output and economic profit if the market price is (i) $14 a pizza. (ii) $12 a pizza. (iii) $10 a pizza. 5. What is Pat's shutdown point and what is Pat's economic profit if it shuts down temporarily? 6. Derive Pat's supply curve.arrow_forwardUse the following table to work Problems 27 and 28. ProPainters hires students at $250 a week to paint houses. It leases equipment at $500 a week. The table sets out its total product schedule. Labor (students) 1 Output (houses painted per week) 2 23 5 3 9 4 12 5 14 6 15 27. If ProPainters paints 12 houses a week, calculate its total cost, average total cost, and marginal cost. At what output is average total cost a minimum? 28. Explain why the gap between ProPainters' total cost and total variable cost is the same no matter how many houses are painted.arrow_forward

- Use the following table to work Problems 17 to 20. The table shows the production function of Jackie's Canoe Rides. Labor Output (rides per day) (workers per day) Plant 1 Plant 2 Plant 3 Plant 4 10 20 40 55 65 20 40 60 75 85 30 65 75 90 100 40 75 85 100 110 Canoes 10 20 30 40 Jackie's pays $100 a day for each canoe it rents and $50 a day for each canoe operator it hires. 19. a. On Jackie's LRAC curve, what is the average cost of producing 40, 75, and 85 rides a week? b. What is Jackie's minimum efficient scale?arrow_forwardPlease solve this questions step by step handwritten solution and do not use ai thank youarrow_forwardPlease solve questions 3 and 4 step by step handwritten solution and no ai toolsarrow_forward

- Please solve questions 1 and 2 step by step handwritten solution and no ai toolsarrow_forwardNot use ai pleasearrow_forward1. Riaz has a limited income and consumes only Apple and Bread. His current consumption choice is 3 apples and 5 bread. The price of apple is $3 each, and the price of bread is $2.5 each. The last apple added 5 units to Sadid's utility, while the last bread added 7 units. Is Riaz making the utility-maximizing choice? Why or why not? Do you suggest any adjustment in Riaz's consumption bundle? Why or why not? Give reasons in support of your answer. State the condition for a consumer's utility maximizing choice and illustrate graphically. 2. Consider the following table of long-run total costs for three different firms: Quantity Total Cost ($) Firm A Firm B Firm C 1 60 11 21 2 70 24 34 3 80 39 49 4 90 56 66 5 100 75 85 6 110 96 106 7 120 119 129 Does each of these firms experience economies of scale or diseconomies of scale? Explain your answer with necessary calculations.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Microeconomics: Private and Public Choice (MindTa...EconomicsISBN:9781305506893Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning

Microeconomics: Private and Public Choice (MindTa...EconomicsISBN:9781305506893Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning Macroeconomics: Private and Public Choice (MindTa...EconomicsISBN:9781305506756Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning

Macroeconomics: Private and Public Choice (MindTa...EconomicsISBN:9781305506756Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning Economics: Private and Public Choice (MindTap Cou...EconomicsISBN:9781305506725Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning

Economics: Private and Public Choice (MindTap Cou...EconomicsISBN:9781305506725Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning Principles of Economics 2eEconomicsISBN:9781947172364Author:Steven A. Greenlaw; David ShapiroPublisher:OpenStax

Principles of Economics 2eEconomicsISBN:9781947172364Author:Steven A. Greenlaw; David ShapiroPublisher:OpenStax Economics (MindTap Course List)EconomicsISBN:9781337617383Author:Roger A. ArnoldPublisher:Cengage Learning

Economics (MindTap Course List)EconomicsISBN:9781337617383Author:Roger A. ArnoldPublisher:Cengage Learning

Microeconomics: Private and Public Choice (MindTa...

Economics

ISBN:9781305506893

Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. Macpherson

Publisher:Cengage Learning

Macroeconomics: Private and Public Choice (MindTa...

Economics

ISBN:9781305506756

Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. Macpherson

Publisher:Cengage Learning

Economics: Private and Public Choice (MindTap Cou...

Economics

ISBN:9781305506725

Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. Macpherson

Publisher:Cengage Learning

Principles of Economics 2e

Economics

ISBN:9781947172364

Author:Steven A. Greenlaw; David Shapiro

Publisher:OpenStax

Economics (MindTap Course List)

Economics

ISBN:9781337617383

Author:Roger A. Arnold

Publisher:Cengage Learning