Videos

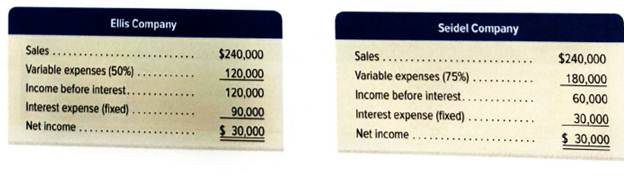

Shown here are condensed income statements for two different companies (both are organized as LLCs and pay no income taxes).

Required

- Compute times interest earned for Ellis Company.

- Compute times interest earned for Seidel Company.

- What happens to each company’s net income if sales increase by 10%?

- What happens to each company’s net income if sales increase by 40%?

- What happens to each company’s net income if sales increase by 90%?

- What happens to each company’s net income if sales decrease by 20%?

- What happens to each company’s net income if sales decrease by 50%?

- What happens to each company’s net income if sales decrease by 80%? Analysis Component

- Comment on the results from parts 3 through 8 in relation to the fixed-cost strategies of the two companies and the ratio values you computed in parts 1 and 2.

1.

Introduction: The times interest earned refer to the ratio of income before interest and taxes to interest earned.

To calculate: Times interest earned for company E.

Explanation of Solution

Computation of times interest earned for company E:

2.

Introduction: The times interest earned refer to the ratio of income before interest and taxes to interest earned.

To calculate: Times interest earned for company S.

Explanation of Solution

Computation of times interest earned for company S:

3.

Introduction: The net income refers to that part of income which is generated after subtracting all expenses such as cost of goods sold and other non-operating expenses, depreciation and taxes.

To calculate: The net income of each company if the sales increased by 10%.

Explanation of Solution

If sales increased by 10% for each company,

For company E;

For company S:

Computing net income for company E:

| Particular | Amount |

| Sales | $264,000 |

| Less: variable expense (50%) | (132,000) |

| Income before interest | 132,000 |

| Less: Interest expense(fixed) | (90,000) |

| Net income | $42,000 |

Computing net income for company S:

| Particular | Amount |

| Sales | $264,000 |

| Less: variable expense (75%) | (180,000) |

| Income before interest | 84,000 |

| Less: Interest expense(fixed) | (30,000) |

| Net income | $54,000 |

4.

Introduction: The net income refers to that part of income which is generated after subtracting all expenses such as cost of goods sold and other non-operating expenses, depreciation and taxes.

To calculate: The net income of each company if the sales increased by 40%.

Explanation of Solution

If sales increased by 40% for each company,

For company E;

For company S:

Computing net income for company E:

| Particular | Amount |

| Sales | $336,000 |

| Less: variable expense (50%) | (168,000) |

| Income before interest | 168,000 |

| Less: Interest expense(fixed) | (90,000) |

| Net income | $78,000 |

Computing net income for company S:

| Particular | Amount |

| Sales | $336,000 |

| Less: variable expense (75%) | (252,000) |

| Income before interest | 84,000 |

| Less: Interest expense(fixed) | (30,000) |

| Net income | $54,000 |

5.

Introduction: The net income refers to that part of income which is generated after subtracting all expenses such as cost of goods sold and other non-operating expenses, depreciation and taxes.

To calculate: The net income of each company if the sales increased by 90%.

Explanation of Solution

If sales increased by 90% for each company,

For company E;

For company S:

Computing net income for company E:

| Particular | Amount |

| Sales | $456,000 |

| Less: variable expense (50%) | (228,000) |

| Income before interest | 228,000 |

| Less: Interest expense(fixed) | (90,000) |

| Net income | $138,000 |

Computing net income for company S:

| Particular | Amount |

| Sales | $456,000 |

| Less: variable expense (75%) | (342,000) |

| Income before interest | 114,000 |

| Less: Interest expense(fixed) | (30,000) |

| Net income | $84,000 |

6.

Introduction: The net income refers to that part of income which is generated after subtracting all expenses such as cost of goods sold and other non-operating expenses, depreciation and taxes.

To calculate: The net income of each company if the sales decreased by 20%.

Explanation of Solution

If sales decreased by 20% for each company,

For company E;

For company S:

Computing net income for company E:

| Particular | Amount |

| Sales | $192,000 |

| Less: variable expense (50%) | (96,000) |

| Income before interest | 96,000 |

| Less: Interest expense(fixed) | (90,000) |

| Net income | $6,000 |

Computing net income for company W:

| Particular | Amount |

| Sales | $192,000 |

| Less: variable expense (75%) | (144,000) |

| Income before interest | 48,000 |

| Less: Interest expense(fixed) | (30,000) |

| Net income | $18,000 |

7.

Introduction: The net income refers to that part of income which is generated after subtracting all expenses such as cost of goods sold and other non-operating expenses, depreciation and taxes.

To calculate: The net income of each company if the sales decreased by 50%.

Explanation of Solution

If sales decreased by 50% for each company,

For company E;

For company S:

Computing net income for company E:

| Particular | Amount |

| Sales | $120,000 |

| Less: variable expense (50%) | (60,000) |

| Income before interest | 60,000 |

| Less: Interest expense(fixed) | (90,000) |

| Net income | ($30,000) |

Computing net income for company S:

| Particular | Amount |

| Sales | $120,000 |

| Less: variable expense (75%) | (90,000) |

| Income before interest | 30,000 |

| Less: Interest expense(fixed) | (30,000) |

| Net income | $0 |

8.

Introduction: The net income refers to that part of income which is generated after subtracting all expenses such as cost of goods sold and other non-operating expenses, depreciation and taxes.

To calculate: The net income of each company if the sales decreased by 80%.

Explanation of Solution

If sales decreased by 80% for each company,

For company E;

For company S:

Computing net income for company M:

| Particular | Amount |

| Sales | $48,000 |

| Less: variable expense (50%) | (24,000) |

| Income before interest | 24,000 |

| Less: Interest expense(fixed) | (90,000) |

| Net income | ($74,000) |

Computing net income for company W:

| Particular | Amount |

| Sales | $48,000 |

| Less: variable expense (75%) | (36,000) |

| Income before interest | 12,000 |

| Less: Interest expense(fixed) | (30,000) |

| Net loss | ($18,000) |

9.

Introduction: The net income refers to that part of income which is generated after subtracting all expenses such as cost of goods sold and other non-operating expenses, depreciation and taxes.

The time's interest earned refers to the ratio of income before interest and taxes to interest earned.

To comment: On the result for interest earned by both the companies and for part 3 to 8.

Explanation of Solution

Comments on times interest earned by both the companies are:

For company E:

The time's interest earned by company E is 1.3 times which is lesser than 2.5 times this indicates that it is difficult for the company to meet its debt and to invest in the company is riskier from the investor's point of view.

For company S:

The time's interest earned by company E is 2times which lesser than 2.5 times but the situation is better than company S, this indicates the riskier to invest in the company from an investor point of view.

Comments on the fixed cost strategies for the company The company fixed cost does not affect the net income as the sales increase but when sales start decreasing the net income is falling down and lead to losses for the company. Thus the company should increase sales or maintain sales to generate profit for the firm.

Want to see more full solutions like this?

Chapter 9 Solutions

Loose Leaf for Financial Accounting: Information for Decisions

- The following information concerns production in the Baking Department for August. All direct materials are placed in process at the beginning of production. Date Item Debit Credit BalanceDebit BalanceCredit August 1 Bal., 6,300 units, 4/5 completed 16,884 31 Direct materials, 113,400 units 226,800 243,684 31 Direct labor 64,390 308,074 31 Factory overhead 36,212 344,286 31 Goods finished, 114,900 units 332,958 11,328 31 Bal., ? units, 2/5 completed 11,328 a. Based on the above data, determine each cost listed below. Round "cost per equivalent unit" answers to the nearest cent. Line Item Description Amount 1. Direct materials cost per equivalent unit $fill in the blank 1 2. Conversion cost per equivalent unit $fill in the blank 2 3. Cost of the beginning work in process completed during August $fill in the blank 3 4. Cost of units started and completed during August $fill in the blank 4 5. Cost of the ending work in…arrow_forwardWaiting for your solution general accounting questionarrow_forwardPlease see an attachment for details general accounting questionarrow_forward

- I want to this question answer general accounting questionarrow_forwardHave you ever noted facework or saving face techniques being used in US-based companies (ones you have worked for or encountered in everyday life)? Explain and offer examples in your initial posting.arrow_forwardNeed correct answer general accountingarrow_forward

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning