Gross Profit Shelly Corporation is an importer and wholesaler. Its merchandise is purchased from several suppliers and is warehoused by Shelly until sold to consumers. In conducting her audit for the year ended June 30, 2019, the corporation’s CPA determined that the system of internal control was good. Accordingly, she observed the physical inventory at an interim date, May 31, 2019, instead of at year-end. The CPA obtained the following information from the general ledger: The CPA’s audit disclosed the following information: Required: In audit engagements in which interim physical inventories are observed, a frequently used auditing procedure is to test the reasonableness of the year-end inventory by the application of gross profit ratios. Prepare in good form the following schedules: 1. Computation of the gross profit ratio for 11 months ended May 31, 2019 2. Computation by the gross profit ratio method of cost of goods sold during June 2019 3. Computation by the gross profit ratio method of June 30, 2019 inventory

Gross Profit Shelly Corporation is an importer and wholesaler. Its merchandise is purchased from several suppliers and is warehoused by Shelly until sold to consumers. In conducting her audit for the year ended June 30, 2019, the corporation’s CPA determined that the system of internal control was good. Accordingly, she observed the physical inventory at an interim date, May 31, 2019, instead of at year-end. The CPA obtained the following information from the general ledger: The CPA’s audit disclosed the following information: Required: In audit engagements in which interim physical inventories are observed, a frequently used auditing procedure is to test the reasonableness of the year-end inventory by the application of gross profit ratios. Prepare in good form the following schedules: 1. Computation of the gross profit ratio for 11 months ended May 31, 2019 2. Computation by the gross profit ratio method of cost of goods sold during June 2019 3. Computation by the gross profit ratio method of June 30, 2019 inventory

Solution Summary: The author calculates the gross profit ratio for 11 months ended May 31, 2019 by using the following formula. Gross profit is the difference between the total revenues and cost of goods sold.

Shelly Corporation is an importer and wholesaler. Its merchandise is purchased from several suppliers and is warehoused by Shelly until sold to consumers. In conducting her audit for the year ended June 30, 2019, the corporation’s CPA determined that the system of internal control was good. Accordingly, she observed the physical inventory at an interim date, May 31, 2019, instead of at year-end.

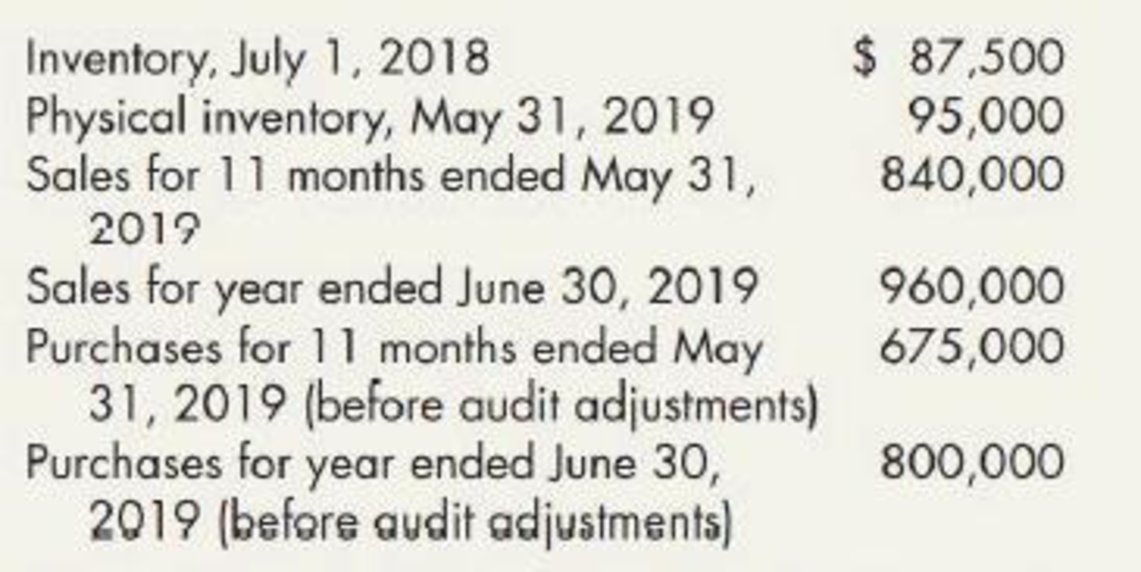

The CPA obtained the following information from the general ledger:

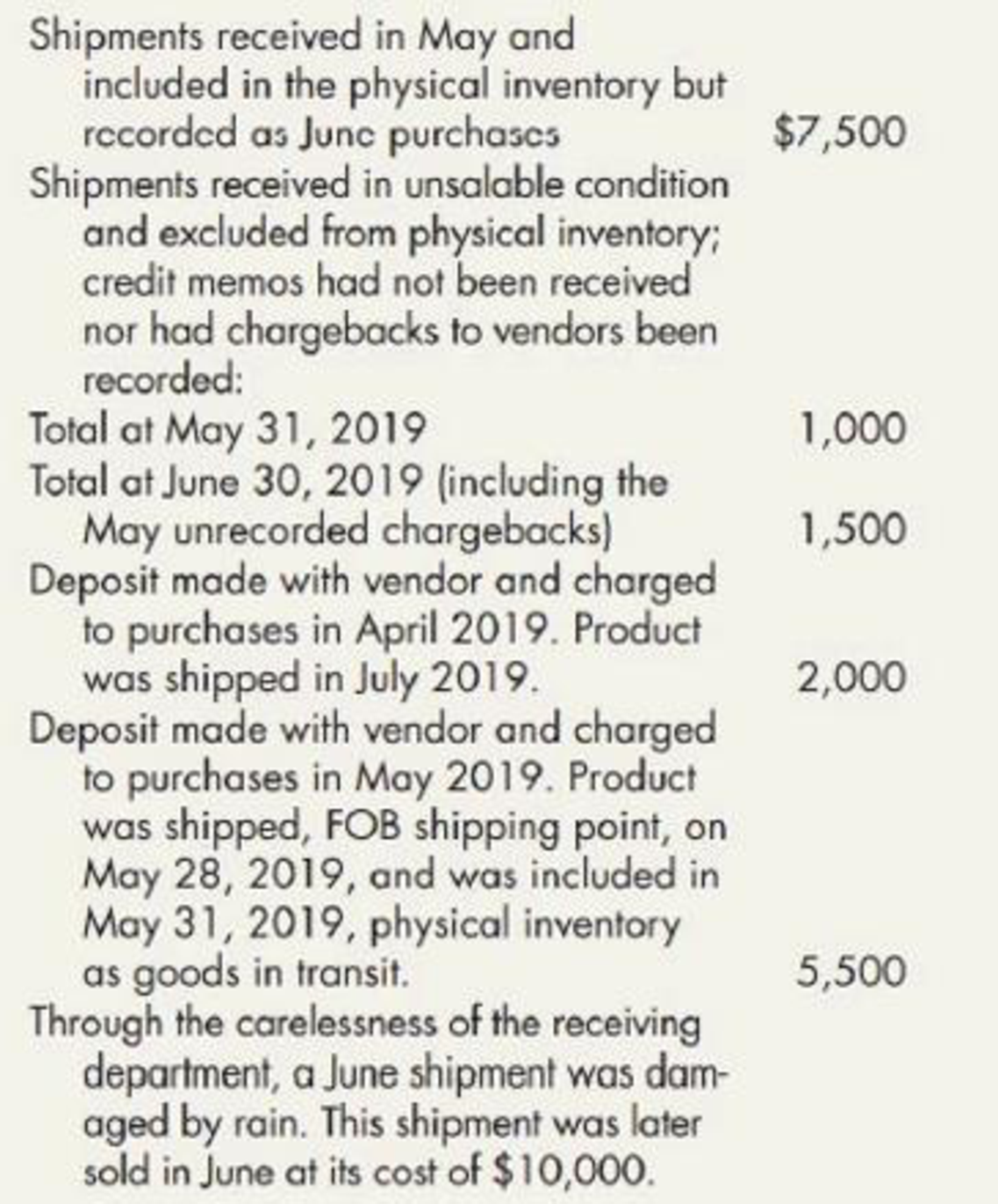

The CPA’s audit disclosed the following information:

Required:

In audit engagements in which interim physical inventories are observed, a frequently used auditing procedure is to test the reasonableness of the year-end inventory by the application of gross profit ratios. Prepare in good form the following schedules:

1. Computation of the gross profit ratio for 11 months ended May 31, 2019

2. Computation by the gross profit ratio method of cost of goods sold during June 2019

3. Computation by the gross profit ratio method of June 30, 2019 inventory

Definition Definition Methods and techniques used by the auditor to gather the appropriate evidence so that a true and fair judgment can be made on the quality of the financial statements of the client. Audit procedures are developed after determining audit objectives, scope, approach, and risk assessment.

Cullumber Company uses a job order cost system and applies overhead to production on the basis of direct labor costs. On January 1,

2025, Job 50 was the only job in process. The costs incurred prior to January 1 on this job were as follows: direct materials $16,800,

direct labor $10,080, and manufacturing overhead $13,440. As of January 1, Job 49 had been completed at a cost of $75,600 and was

part of finished goods inventory. There was a $12,600 balance in the Raw Materials Inventory account on January 1.

During the month of January, Cullumber Company began production on Jobs 51 and 52, and completed Jobs 50 and 51. Jobs 49 and

50 were sold on account during the month for $102,480 and $132,720, respectively. The following additional events occurred during

the month.

1.

Purchased additional raw materials of $75,600 on account.

2.

Incurred factory labor costs of $58,800.

3.

Incurred manufacturing overhead costs as follows: depreciation expense on equipment $10,080; and various other…

Cullumber Company uses a job order cost system and applies overhead to production on the basis of direct labor costs. On January 1,

2025, Job 50 was the only job in process. The costs incurred prior to January 1 on this job were as follows: direct materials $16,800,

direct labor $10,080, and manufacturing overhead $13,440. As of January 1, Job 49 had been completed at a cost of $75,600 and was

part of finished goods inventory. There was a $12,600 balance in the Raw Materials Inventory account on January 1.

During the month of January, Cullumber Company began production on Jobs 51 and 52, and completed Jobs 50 and 51. Jobs 49 and

50 were sold on account during the month for $102,480 and $132,720, respectively. The following additional events occurred during

the month.

1.

Purchased additional raw materials of $75,600 on account.

2.

Incurred factory labor costs of $58,800.

3.

Incurred manufacturing overhead costs as follows: depreciation expense on equipment $10,080; and various other…

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.

Auditing: A Risk Based-Approach (MindTap Course L...AccountingISBN:9781337619455Author:Karla M Johnstone, Audrey A. Gramling, Larry E. RittenbergPublisher:Cengage Learning

Auditing: A Risk Based-Approach (MindTap Course L...AccountingISBN:9781337619455Author:Karla M Johnstone, Audrey A. Gramling, Larry E. RittenbergPublisher:Cengage Learning Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning