Concept explainers

Videos

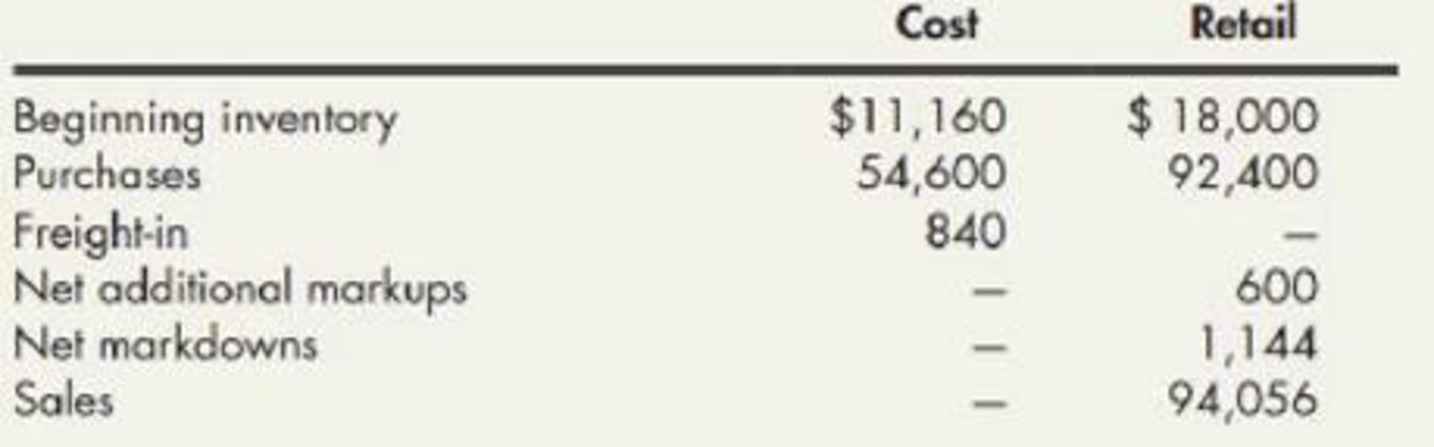

Retail Inventory Method The following information relates to the retail inventory method used by Jeffress Company:

Required:

- 1. Compute the ending inventory by the retail inventory method using the following cost flow' assumptions (round the cost-to-retail ratio to 3 decimal places):

- a. FIFO

- b. average cost

- c. LIFO

- d. lower of cost or market (based on average cost)

- 2. Next Level What assumptions are necessary for the retail inventory method to produce accurate estimates of ending inventory?

1.

Calculate the cost of ending inventory by the retail method using FIFO, average cost, LIFO, and LCM cost flow assumptions.

Explanation of Solution

Retail inventory method: It takes into account all the retail amounts that is, the current selling prices. Under this method, the goods available for sale, at retail is deducted from the sales, at retail to determine the ending inventory, at retail.

Conventional Retail Method: Conventional retail method refers to the estimation of the lower of average cost or market by eliminating the markdowns from the calculation of the cost-to-retail percentage.

In this case, the cost-to-retail percentage will be determined by dividing the goods available for sale at cost by the goods available for at retail (excluding markdowns). Thus, the conventional retail method will always result in lower estimation of ending inventory when the markdowns exist.

a.

FIFO: Under this inventory method, the units that are purchased first are sold first. Thus, it starts from the selling of the beginning inventory, followed by the units purchased in a chronological order of their purchases took place during a particular period.

Calculate the cost of ending inventory by the retail method using FIFO cost flow.

| Ending Inventory - FIFO | ||

| Details | Cost ($) | Retail ($) |

| Purchases | 54,600 | 92,400 |

| Freight-in | 840 | |

| Markups (net) | 600 | |

| Markdowns | 0 | (1,144) |

| 55,440 | 91,856 | |

| Add: Beginning inventory | 11,160 | 18,000 |

| Goods available for sale | 66,600 | 109,856 |

| Less: Sales | (94,056) | |

| Ending inventory at retail | $15,800 | |

| Ending inventory at cost | $9,543 | |

Table (1)

Working note 1:

Calculate ending inventory at cost:

Step 1: Calculate cost-to-retail ratio.

Step 2: Calculate ending inventory at cost.

b.

Average cost method: Under this method, the cost of the goods available for sale is divided by the number of units available for sale during a particular period.

Calculate the cost of ending inventory by the retail method using average cost flow.

| Ending Inventory - Average Cost | ||

| Details | Cost ($) | Retail ($) |

| Beginning inventory | 11,160 | 18,000 |

| Add: Net purchase | 54,600 | 92,400 |

| Freight in | 840 | |

| Net markups (net) | 600 | |

| Less: Net markdowns | 0 | (1,144) |

| Goods available for sale | 66,600 | 109,856 |

| Less: Sales | (94,056) | |

| Estimated ending inventory at retail | $15,800 | |

| Estimated ending inventory at cost | $9,575 | |

Table (2)

Working note 1:

Calculate ending inventory at cost.

Step 1: Calculate cost-to-retail ratio.

Step 2: Calculate ending inventory at cost.

c.

LIFO: Under this inventory method, the units that are purchased last are sold first. Thus, it starts from the selling of the units recently purchased and ending with the beginning inventory.

Calculate the cost of ending inventory by the retail method using LIFO cost flow.

| Ending Inventory - LIFO | ||

| Details | Cost ($) | Retail ($) |

| Beginning inventory | 11,160 | 18,000 |

| Net purchase | 54,600 | 92,400 |

| Freight-in | 840 | |

| Net markups | 600 | |

| Less: Net markdowns | 0 | (1,144) |

| 55,440 | 91,856 | |

| 11,160 | 18,000 | |

| Goods available for sale | 66,600 | 109,856 |

| Less: Sales | (94,056) | |

| Estimated ending inventory at retail | $15,800 | |

| Estimated ending inventory at LIFO cost | 9,796 | |

Table (3)

Working note 1:

Calculate ending inventory at cost for beginning layer.

Step 1: Calculate cost-to-retail ratio (Beginning layer).

Step 2: Calculate ending inventory at cost (Beginning layer).

d.

Lower-of-cost-or-market: The lower-of-cost-or-market (LCM) is a method which requires the reporting of the ending merchandise inventory in the financial statement of a company, either at current market value or at historical cost price of the inventory, whichever is less.

Calculate the cost of ending inventory by the retail method using lower of cost or market rule:

| Ending Inventory - LCM | ||

| Details | Cost ($) | Retail ($) |

| Beginning inventory | 11,160 | 18,00 |

| Add: Net purchase | 54,600 | 92,400 |

| Freight-in | 840 | |

| Net markups | 0 | 600 |

| Goods available for sale before markdowns | 66,600 | 111,000 |

| Less: Net markdowns | 0 | (1,144) |

| Sales | (94,056) | |

| Estimated ending inventory at retail | $15,800 | |

| Estimated ending inventory at cost (LCM) | $9,480 | |

Table (4)

Working note 1:

Calculate ending inventory at cost:

Step 1: Calculate cost-to-retail ratio.

Step 2: Calculate ending inventory at cost.

2.

Indicate the needed assumptions for the retail inventory method to produce correct estimated of ending inventory.

Explanation of Solution

There are two general assumptions are required for the retail inventory method to produce a correct estimates of inventory.

- Firstly, the company’s inventory items should be adequately homogeneous so that all of the items have the same markup, or if different markups exist and the items in ending inventory should be in the same proportion to those items in goods available for sale.

- Secondly, over the accounting period the cost-to-retail ratio must remain constant.

Want to see more full solutions like this?

Chapter 8 Solutions

Intermediate Accounting: Reporting And Analysis

- Need this general account subject solutionarrow_forwardLinden Corporation uses a predetermined overhead rate of $18.75 per direct labor hour. This predetermined rate was based on a cost formula that estimated $225,000 of total manufacturing overhead for an estimated activity level of 12,000 direct labor hours. During the period, the company incurred actual total manufacturing overhead costs of $210,000 and 11,200 total direct labor hours worked. Required: Determine the amount of manufacturing overhead that would have been applied to all jobs during the period.arrow_forwardchoose best answerarrow_forward

- Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning  College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning Financial Reporting, Financial Statement Analysis...FinanceISBN:9781285190907Author:James M. Wahlen, Stephen P. Baginski, Mark BradshawPublisher:Cengage Learning

Financial Reporting, Financial Statement Analysis...FinanceISBN:9781285190907Author:James M. Wahlen, Stephen P. Baginski, Mark BradshawPublisher:Cengage Learning