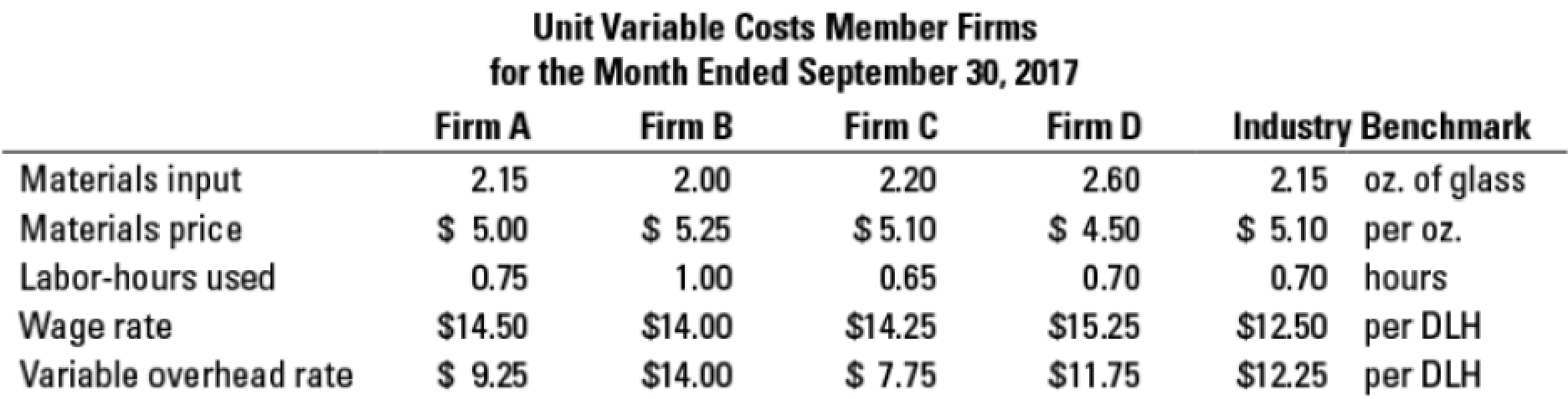

Use of materials and manufacturing labor variances for benchmarking. You are a new junior accountant at In Focus Corporation, maker of lenses for eyeglasses. Your company sells generic-quality lenses for a moderate price. Your boss, the controller, has given you the latest month’s report for the lens trade association. This report includes information related to operations for your firm and three of your competitors within the trade association. The report also includes information related to the industry benchmark for each line item in the report. You do not know which firm is which, except that you know you are Firm A. 1. Calculate the total variable cost per unit for each firm in the trade association. Compute the percent of total for the material, labor, and variable overhead components. 2. Using the trade association’s industry benchmark, calculate direct materials and direct manufacturing labor price and efficiency variances for the four firms. Calculate the percent over standard for each firm and each variance. 3. Write a brief memo to your boss outlining the advantages and disadvantages of belonging to this trade association for benchmarking purposes. Include a few ideas to improve productivity that you want your boss to take to the department heads’ meeting.

Use of materials and manufacturing labor variances for benchmarking. You are a new junior accountant at In Focus Corporation, maker of lenses for eyeglasses. Your company sells generic-quality lenses for a moderate price. Your boss, the controller, has given you the latest month’s report for the lens trade association. This report includes information related to operations for your firm and three of your competitors within the trade association. The report also includes information related to the industry benchmark for each line item in the report. You do not know which firm is which, except that you know you are Firm A. 1. Calculate the total variable cost per unit for each firm in the trade association. Compute the percent of total for the material, labor, and variable overhead components. 2. Using the trade association’s industry benchmark, calculate direct materials and direct manufacturing labor price and efficiency variances for the four firms. Calculate the percent over standard for each firm and each variance. 3. Write a brief memo to your boss outlining the advantages and disadvantages of belonging to this trade association for benchmarking purposes. Include a few ideas to improve productivity that you want your boss to take to the department heads’ meeting.

Solution Summary: The author explains the variable cost of production of a product that varies with the change in output.

Use of materials and manufacturing labor variances for benchmarking. You are a new junior accountant at In Focus Corporation, maker of lenses for eyeglasses. Your company sells generic-quality lenses for a moderate price. Your boss, the controller, has given you the latest month’s report for the lens trade association. This report includes information related to operations for your firm and three of your competitors within the trade association. The report also includes information related to the industry benchmark for each line item in the report. You do not know which firm is which, except that you know you are Firm A.

1. Calculate the total variable cost per unit for each firm in the trade association. Compute the percent of total for the material, labor, and variable overhead components.

2. Using the trade association’s industry benchmark, calculate direct materials and direct manufacturing labor price and efficiency variances for the four firms. Calculate the percent over standard for each firm and each variance.

3. Write a brief memo to your boss outlining the advantages and disadvantages of belonging to this trade association for benchmarking purposes. Include a few ideas to improve productivity that you want your boss to take to the department heads’ meeting.

Definition Definition System of assigning an estimated cost to the product (instead of the actual cost) so that the product cost can be determined well in advance and the pricing of the product can be done on time. Since the actual cost cannot be predicted at the initial stage of the production process, the estimated cost is recorded in the books. Any deviation of the estimated cost of the actual cost is adjusted in the books at the end of the period.

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning

Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning