Concept explainers

Videos

Lower-of-cost-or market inventory

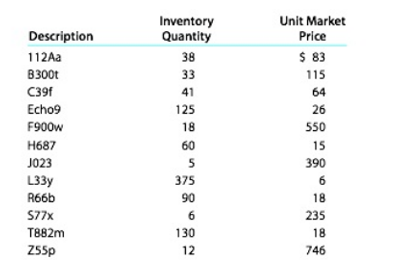

Data on the physical inventory of Moyer Company as of December 31, 20Y9, are presented below.

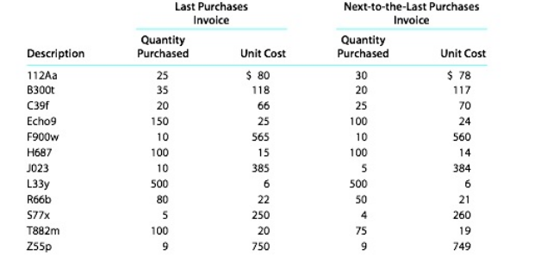

Quantity and cost data from the last purchases invoice of the year and the next-to-the-last purchases invoice are summarized as follows:

Instructions

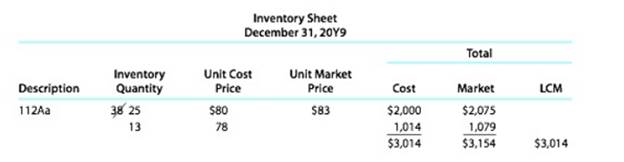

Determine the inventory at cost and at the lower of cost or market, using the first-in, first-out method. Record the appropriate unit costs on an inventory sheet and complete the pricing of the inventory. When there are two different unit costs applicable to an item, proceed as follows:

1. Draw a line through the quantity, and insert the quantity and unit cost of the last purchase.

2. On the following line, insert the quantity and unit cost of the next-to-the-last purchase.

3. Total the cost and market columns and insert the lower of the two totals in the LCM column. The first item on the inventory sheet has been completed below as an  example.

example.

Want to see the full answer?

Check out a sample textbook solution

Chapter 6 Solutions

Survey of Accounting (Accounting I)

- Hii expert please given answer general accountingarrow_forwardGranville Corporation has two divisions: The Beta Division and the Delta Division. The Beta Division has sales of $375,000, variable expenses of $182,500, and traceable fixed expenses of $84,200. The Delta Division has sales of $580,000, variable expenses of $312,700, and traceable fixed expenses of $128,600. The total amount of common fixed expenses not traceable to the individual divisions is $145,500. What is the company's net operating income (NOI)? answerarrow_forwardNeed step by step answerarrow_forward

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning

Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning