Concept explainers

Videos

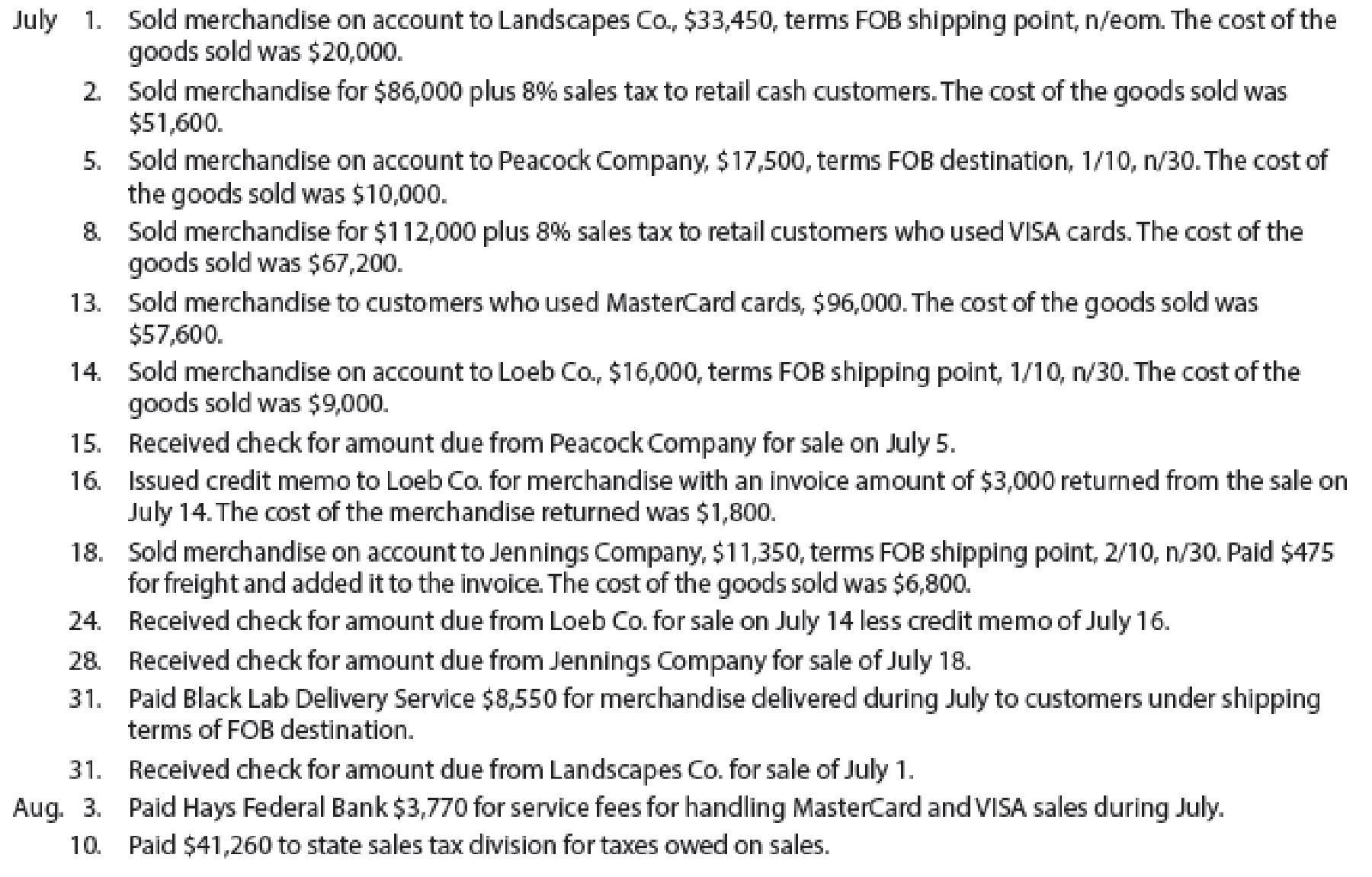

Sales-related transactions using perpetual inventory system

The following selected transactions were completed by Green Lawn Supplies Co., which sells irrigation supplies primarily to other businesses and occasionally to retail customers:

Instructions

Record the sale transactions of the company.

Explanation of Solution

Sales is an activity of selling the inventory of a business.

Record the journal entry for the sale of inventory on account.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 1 | Accounts receivable | 33,450 | |

| Sales Revenue | 33,450 | ||

| (To record the sale of inventory on account) |

Table (1)

- • Accounts Receivable is an asset and it is increased by $33,450. Therefore, debit accounts receivable with $33,450.

- • Sales revenue is revenue and it increases the value of equity by $33,450. Therefore, credit sales revenue with $33,450.

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 1 | Cost of Sold | 20,000 | |

| Inventory | 20,000 | ||

| (To record the cost of goods sold) |

Table (2)

- • Cost of sold is an expense account and it decreases the value of equity by $20,000. Therefore, debit cost of sold account with $20,000.

- • Inventory is an asset and it is decreased by $20,000. Therefore, credit inventory account with $20,000.

Record the journal entry for the sale of inventory for cash.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 2 | Cash | 92,880 (2) | |

| Sales Revenue | 86,000 | ||

| Sales Tax Payable | 6,880 (1) | ||

| (To record the sale of inventory for cash) |

Table (3)

Working Note (1):

Calculate the amount of sales tax payable.

Sales revenue = $86,000

Sales tax percentage = 8%

Working Note (2):

Calculate the amount of cash received.

Sales revenue = $86,000

Sales tax payable = $6,880 (1)

- • Cash is an asset and it is increased by $92,880. Therefore, debit cash account with $92,880.

- • Sales revenue is revenue and it increases the value of equity by $86,000. Therefore, credit sales revenue with $86,000.

- • Sales tax payable is a liability and it is increased by $6,880. Therefore, credit sales tax payable account with $6,880.

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 2 | Cost of Sold | 51,600 | |

| Inventory | 51,600 | ||

| (To record the cost of goods sold) |

Table (4)

- • Cost of sold is an expense account and it decreases the value of equity by $51,600. Therefore, debit cost of sold account with $51,600.

- • Inventory is an asset and it is decreased by $51,600. Therefore, credit inventory account with $51,600.

Record the journal entry for the sale of inventory on account.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 5 | Accounts receivable | 17,325 (3) | |

| Sales Revenue | 17,325 | ||

| (To record the sale of inventory on account) |

Table (5)

Working Note (3):

Calculate the amount of accounts receivable.

Sales = $17,500

Discount percentage = 1%

- • Accounts Receivable is an asset and it is increased by $17,325. Therefore, debit accounts receivable with $17,325.

- • Sales revenue is revenue and it increases the value of equity by $17,325. Therefore, credit sales revenue with $17,325.

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 5 | Cost of Sold | 10,000 | |

| Inventory | 10,000 | ||

| (To record the cost of goods sold) |

Table (6)

- • Cost of sold is an expense account and it decreases the value of equity by $10,000. Therefore, debit cost of sold account with $10,000.

- • Inventory is an asset and it is decreased by $10,000. Therefore, credit inventory account with $10,000.

Record the journal entry for the sale of inventory for cash.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 8 | Cash | 120,960 (5) | |

| Sales Revenue | 112,000 | ||

| Sales Tax Payable | 8,960 (4) | ||

| (To record the sale of inventory for cash) |

Table (7)

Working Note (4):

Calculate the amount of sales tax payable.

Sales revenue = $112,000

Sales tax percentage = 8%

Working note (5):

Calculate the amount of cash received.

Sales revenue = $112,000

Sales tax payable = $8,960 (4)

- • Cash is an asset and it is increased by $120,960. Therefore, debit cash account with $120,960.

- • Sales revenue is revenue and it increases the value of equity by $112,000. Therefore, credit sales revenue with $112,000.

- • Sales tax payable is a liability and it is increased by $8,960. Therefore, credit sales tax payable account with $8,960.

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 8 | Cost of Sold | 67,200 | |

| Inventory | 67,200 | ||

| (To record the cost of goods sold) |

Table (8)

- • Cost of sold is an expense account and it decreases the value of equity by $67,200. Therefore, debit cost of sold account with $67,200.

- • Inventory is an asset and it is decreased by $67,200. Therefore, credit inventory account with $67,200.

Record the journal entry for the sale of inventory for cash.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 13 | Cash | 96,000 | |

| Sales Revenue | 96,000 | ||

| (To record the sale of inventory for cash) |

Table (9)

- • Cash is an asset and it is increased by $96,000. Therefore, debit cash account with $96,000.

- • Sales revenue is revenue and it increases the value of equity by $96,000. Therefore, credit sales revenue with $96,000.

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 13 | Cost of Sold | 57,600 | |

| Inventory | 57,600 | ||

| (To record the cost of goods sold) |

Table (10)

- • Cost of sold is an expense account and it decreases the value of equity by $57,600. Therefore, debit cost of sold account with $57,600.

- • Inventory is an asset and it is decreased by $57,600. Therefore, credit inventory account with $57,600.

Record the journal entry for the sale of inventory on account.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 14 | Accounts receivable | 15,840 (6) | |

| Sales Revenue | 15,840 | ||

| (To record the sale of inventory on account) |

Table (11)

Working Note (6):

Calculate the amount of accounts receivable.

Sales = $16,000

Discount percentage = 1%

- • Accounts Receivable is an asset and it is increased by $15,840. Therefore, debit accounts receivable with $15,840.

- • Sales revenue is revenue and it increases the value of equity by $15,840. Therefore, credit sales revenue with $15,840.

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 14 | Cost of Sold | 9,000 | |

| Inventory | 9,000 | ||

| (To record the cost of goods sold) |

Table (12)

- • Cost of sold is an expense account and it decreases the value of equity by $9,000. Therefore, debit cost of sold account with $9,000.

- • Inventory is an asset and it is decreased by $9,000. Therefore, credit inventory account with $9,000.

Record the journal entry for the cash receipt against accounts receivable.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 15 | Cash | 17,325 | |

| Accounts Receivable | 17,325 | ||

| (To record the receipt of cash against accounts receivables) |

Table (13)

- • Cash is an asset and it is increased by $17,325. Therefore, debit cash account with $17,325.

- • Accounts Receivable is an asset and it is increased by $17,325. Therefore, debit accounts receivable with $17,325.

Record the journal entry for sales return.

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| July 16 | Customer Refunds Payable | 2,970 (7) | ||

| Accounts Receivable | 2,970 | |||

| (To record sales returns) |

Table (14)

Working note (7):

Calculate the amount of refund owed to the customer.

Sales return = $3,000

Discount percentage = 1%

- • Customer refunds payable is a liability account and it is decreased by $2,970. Therefore, debit customer refunds payable account with $2,970.

- • Accounts Receivable is an asset and it is decreased by $2,970. Therefore, credit account receivable with $2,970.

Record the journal entry for the return of the .

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 16 | Inventory | 1,800 | |

| Estimated Returns Inventory | 1,800 | ||

| (To record the return of the ) |

Table (15)

- • Inventory is an asset and it is increased by $1,800. Therefore, debit inventory account with $1,800.

- • Estimated retunrs inventory is an expense account and it increases the value of equity by $1,800. Therefore, credit estimated returns inventory account with $1,800.

Record the journal entry for the sale of inventory on account.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 18 | Accounts receivable | 11,123 (8) | |

| Sales Revenue | 11,123 | ||

| (To record the sale of inventory on account) |

Table (16)

Working Note (8):

Calculate the amount of accounts receivable.

Sales = $11,350

Discount percentage = 2%

- • Accounts Receivable is an asset and it is increased by $11,123. Therefore, debit accounts receivable with $11,123.

- • Sales revenue is revenue and it increases the value of equity by $11,123. Therefore, credit sales revenue with $11,123.

Record the journal entry.

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| July 18 | Accounts Receivable | 475 | ||

| Cash | 475 | |||

| (To record freight charges paid) |

Table (17)

- • Accounts Receivable is an asset and it is increased by $475. Therefore, debit accounts receivable with $475.

- • Cash is an asset and it is decreased by $475. Therefore, credit cash account with $475.

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 18 | Cost of Sold | 6,800 | |

| Inventory | 6,800 | ||

| (To record the cost of goods sold) |

Table (18)

- • Cost of sold is an expense account and it decreases the value of equity by $6,800. Therefore, debit cost of sold account with $6,800.

- • Inventory is an asset and it is decreased by $6,800. Therefore, credit inventory account with $6,800.

Record the journal entry for the cash receipt against accounts receivable.

| Date | Accounts and Explanation |

Debit ($) | Credit ($) |

| July 24 | Cash | 12,870 (9) | |

| Accounts Receivable | 12,870 | ||

| (To record the receipt of cash against accounts receivables) |

Table (19)

Working note (9):

Calculate the amount of cash received.

Net accounts receivable = $15,840

Customer refunds payable = $2,970

- • Cash is an asset and it is increased by $12,870. Therefore, debit cash account with $12,870.

- • Accounts Receivable is an asset and it is increased by $12,870. Therefore, debit accounts receivable with $12,870.

Record the journal entry for the cash receipt against accounts receivable.

| Date | Accounts and Explanation |

Debit ($) | Credit ($) |

| July 28 | Cash | 11,598 (10) | |

| Accounts Receivable | 11,598 | ||

| (To record the receipt of cash against accounts receivables) |

Table (20)

Working note (10):

Calculate the amount of cash received.

Net accounts receivable = $11,123

Freight charges = $475

- • Cash is an asset and it is increased by $11,598. Therefore, debit cash account with $11,598.

- • Accounts Receivable is an asset and it is increased by $11,598. Therefore, debit accounts receivable with $11,598.

Record the journal entry for delivery expense.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 31 | Delivery expense | 8,550 | |

| Cash | 8,550 | ||

| (To record the payment of delivery expenses) |

Table (21)

- • Delivery expense is an expense account and it decreases the value of equity by $8,550. Therefore, debit delivery expense account with $8,550.

- • Cash is an asset and it is decreased by $8,550. Therefore, credit cash account with $8,550.

Record the journal entry for the cash receipt against accounts receivable.

| Date | Accounts and Explanation |

Debit ($) | Credit ($) |

| July 31 | Cash | 33,450 | |

| Accounts Receivable | 33,450 | ||

| (To record the receipt of cash against accounts receivables) |

Table (22)

- • Cash is an asset and it is increased by $33,450. Therefore, debit cash account with $33,450.

- • Accounts Receivable is an asset and it is increased by $33,450. Therefore, debit accounts receivable with $33,450.

Record the journal entry for credit card expense.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| August 3 | Credit card expense | 3,770 | |

| Cash | 3,770 | ||

| (To record the payment of credit card expenses) |

Table (23)

- • Credit card expense is an expense account and it decreases the value of equity by $3,770. Therefore, debit credit card expense account with $3,770.

- • Cash is an asset and it is decreased by $3,770. Therefore, credit cash account with $3,770.

Record the journal entry for credit card expense.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| August 10 | Sales tax payable | 41,260 | |

| Cash | 41,260 | ||

| (To record the payment of credit card expenses) |

Table (24)

- • Sales tax payable is a liability account and it is decreased by $41,260. Therefore, debit customer refunds payable account with $41,260.

- • Cash is an asset and it is decreased by $41,260. Therefore, credit cash account with $41,260

Want to see more full solutions like this?

Chapter 5 Solutions

Financial and Managerial Accounting - Workingpapers

- Green Grow Incorporated (GGI) manufactures lawn fertilizer. Because of the product’s very high quality, GGI often receives special orders from agricultural research groups. For each type of fertilizer sold, each bag is carefully filled to have the precise mix of components advertised for that type of fertilizer. GGI’s operating capacity is 34,000 one-hundred-pound bags per month, and it currently is selling 32,000 bags manufactured in 32 batches of 1,000 bags each. The firm just received a request for a special order of 7,400 one-hundred-pound bags of fertilizer for $210,000 from APAC, a research organization. The production costs would be the same, but there would be no variable selling costs. Delivery and other packaging and distribution services would cause a one-time $3,900 cost for GGI. The special order would be processed in two batches of 3,700 bags each. (No incremental batch-level costs are anticipated. Most of the batch-level costs in this case are short-term fixed costs,…arrow_forwardGeneral accountingarrow_forwardGeneral Accounting questionarrow_forward

- What is the budgeted cost of goods sold for March?arrow_forwardThe standard materials cost of a product is $40 per unit, based on 10 pounds of raw materials at a standard cost of $4 per pound. During January 20X9, 1,000 units of product were produced, using 10,200 pounds of raw material at a cost of $4.20 per pound. a) The standard cost for materials for January is b) The total materials variance for the month is c) The materials quantity variance is d) The materials price variance isarrow_forwardFinancial accounting questionarrow_forward

- What is the nominal cost of trade credit if the terms are 4/10, net 45 assuming that customers forego the discount and pay on the 45th day? (365 in year)arrow_forwardWhen would a variance be labeled as favorable? (a) When standard costs are less than actual costs (b) When estimated costs are greater than actual costs (c) When actual costs are less than standard costs (d) When standard costs are equal to actual costs.arrow_forwardGeneral accountingarrow_forward

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning