Concept explainers

Videos

1. and 2.

Prepare the T-accounts.

1. and 2.

Explanation of Solution

T-account:

An account is referred to as a T-account, because the alignment of the components of the account resembles the capital letter ‘T’. An account consists of the three main components which are as follows:

- The title of the account

- The left or debit side

- The right or credit side

Post the unadjusted balances and the

Cash account:

| Cash | |||

| 10,300 | |||

| Balance | 10,300 | ||

| Accounts Receivable | |||

| 9,500 | |||

| Balance | 9,500 | ||

Supplies account:

| Supplies | |||

| 2,000 | |||

| 1,300 | |||

| Balance | 700 | ||

Interest receivable account:

| Interest receivable account | |||

| 0 | |||

| 800 | |||

| Balance | 800 | ||

Prepaid rent account:

| Prepaid rent | |||

| 7,200 | |||

| 5,400 | |||

| Balance | 1,800 | ||

Land account:

| Land | |||

| 78,000 | |||

| Balance | 78,000 | ||

Notes receivable account:

| Notes receivable | |||

| 20,000 | |||

| Balance | 20,000 | ||

Accounts Payable account:

| Accounts Payable | |||

| 7,700 | |||

| Balance | 7,700 | ||

Salaries Payable account:

| Salaries Payable | |||

| 0 | |||

| 2,100 | |||

| Balance | 2,100 | ||

Utilities Payable account:

| Utilities Payable | |||

| 0 | |||

| 200 | |||

| Balance | 200 | ||

Deferred revenue account:

| Deferred revenue | |||

| 5,300 | |||

| 3,300 | |||

| Balance | 2,000 | ||

Common Stock account:

| Common Stock | |||

| 79,000 | |||

| 0 | |||

| Balance | 79,000 | ||

| Retained Earnings | |||

| 19,700 | |||

| Balance | 19,700 | ||

Service Revenue account:

| Service Revenue | |||

| 0 | |||

| 42,200 | |||

| 3,300 | |||

| Balance | 45,500 | ||

Interest Revenue account:

| Interest Revenue | |||

| 0 | |||

| 800 | |||

| Balance | 800 | ||

Salaries Expense account:

| Salaries Expense | |||

| 24,500 | |||

| 2,100 | |||

| Balance | 26,600 | ||

Utilities Expense account:

| Utilities Expense | |||

| 2,400 | |||

| 200 | |||

| Balance | 2,600 | ||

Rent Expense account:

| Rent Expense | |||

| 0 | |||

| 5,400 | |||

| Balance | 5,400 | ||

Supplies Expense account:

| Supplies Expense | |||

| 0 | |||

| 1,300 | |||

| Balance | 1,300 | ||

3.

Prepare an adjusted

3.

Explanation of Solution

Trial balance:

Trial balance is a summary of all the ledger accounts balances presented in a tabular form with two column, debit and credit. It checks the mathematical accuracy of the

Prepare an adjusted trail balance for the year ending December 31, 2021:

|

CT Music Academy Adjusted Trial Balance For the Year Ending December 31, 2021 | ||

| Accounts | Debit ($) | Credit ($) |

| Cash | 10,300 | |

| Accounts Receivable | 9,500 | |

| Interest receivable | 800 | |

| Supplies | 700 | |

| Prepaid Rent | 1,800 | |

| Land | 78,000 | |

| Notes Receivable | 20,000 | |

| Accounts Payable | 7,700 | |

| Salaries Payable | 2,100 | |

| Deferred revenue | 2,000 | |

| Utilities Payable | 200 | |

| Common Stock | 79,000 | |

| Retained Earnings | 19,700 | |

| Interest Revenue | 800 | |

| Service Revenue | 45,500 | |

| Salaries Expense | 26,600 | |

| Rent Expense | 5,400 | |

| Supplies Expense | 1,300 | |

| Utilities Expense | 2,600 | |

| Total | 157,000 | 157,000 |

Table (1)

4.

Prepare an income statement, statement of shareholders’ equity, and a classified

4.

Explanation of Solution

Income statement:

The financial statement which reports revenues and expenses from business operations and the result of those operations as net income or net loss for a particular time period is referred to as income statement.

Prepare an income statement for the year ended December 31, 2021:

|

CT Music Academy Income statement For the Year Ending December 31, 2021 | ||

| Details | Amount ($) | Amount ($) |

| Revenues: | ||

| Service Revenue | 45,500 | |

| Interest Revenue | 800 | |

| Total Revenue | 46,300 | |

| Less: Expenses | ||

| Salaries Expense | 26,600 | |

| Rent Expense | 5,400 | |

| Supplies Expense | 1,300 | |

| Utilities Expense | 2,600 | |

| Total Expenses | (35,900) | |

| Net Income | $10,400 | |

Table (2)

Statement of

Stockholders’ equity statement shows the changes made in the stockholders’ equity account and in the total stockholders’ equity during the accounting period. It is otherwise known as statements of shareholder’s investment.

Prepare statement of stockholders’ equity the year ended December 31, 2021.

|

CT Music Academy Statement of Stockholders’ Equity For the Year Ended December 31, 2021 | |||

| Particulars | Common Stock | Retained Earnings | Total Stockholders’ Equity |

| Beginning balance | $79,000 | $19,700 | $64,000 |

| Issuance of common stock | $0 | $0 | $0 |

| Less: Net income for 2021 | $0 | $10,400 | $0 |

| Less: Dividends | $0 | $0 | $0 |

| Ending balance | $79,000 | $30,100 | $109,100 |

Table (3)

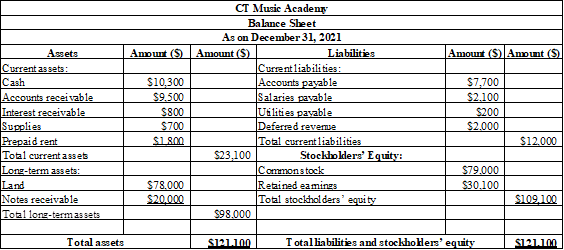

Balance sheet: This financial statement reports a company’s resources (assets) and claims of creditors (liabilities) and claims of stockholders (stockholders’ equity) over those resources. The resources of the company are assets which include money contributed by stockholders and creditors. Hence, the main elements of the balance sheet are assets, liabilities, and stockholders’ equity.

Prepare the balance sheet as of December 31, 2021.

Table (4)

5.

Prepare the closing entries.

5.

Explanation of Solution

Closing entries: The journal entries prepared to close the temporary accounts to Retained Earnings account are referred to as closing entries. The revenue, expense, and dividends accounts are referred to as temporary accounts because the information and figures in these accounts is held temporarily and consequently transferred to permanent account at the end of accounting year.

Prepare the closing entry for revenue account.

| Date | Accounts title and explanation |

Debit ($) |

Credit ($) |

| December 31, 2021 | Service Revenues | 45,500 | |

| Interest Revenue | 800 | ||

| Retained Earnings | 46,300 | ||

| (To close the revenues account) |

Table (5)

In this closing entry, service revenue account and interest revenue account is closed by transferring the amount of service revenue and interest account to the retained earnings account in order to bring the revenue account balance to zero. Hence, debit the service revenue account and interest revenue account and credit retained earnings account.

Prepare the closing entry for expense account:

| Date | Accounts title and explanation | Post Ref. |

Debit ($) |

Credit ($) |

| December 31, 2021 | Retained Earnings | 35,900 | ||

| Salaries expense | 26,600 | |||

| Rent expense | 5,400 | |||

| Supplies expense | 1,300 | |||

| Utilities expense | 2,600 | |||

| (To close the expenses account) |

Table (6)

In this closing entry, all the expenses account is closed by transferring the amount of expenses to the retained earnings in order to bring the expenses account balance to zero. Hence, debit the retained earnings account and credit all expenses account.

6.

Prepare the T-Accounts to post the closing entries.

6.

Explanation of Solution

Retained Earnings account:

| Retained Earnings | |||

| 19,700 | |||

| 35,900 | 46,300 | ||

| Balance | 30,100 | ||

Service Revenue account:

| Service Revenue | |||

| 42,200 | |||

| 42,200 | |||

| Balance | 0 | ||

Interest Revenue account:

| Interest Revenue | |||

| 800 | |||

| 800 | |||

| Balance | 0 | ||

Salaries Expense account:

| Salaries Expense | |||

| 24,500 | |||

| 2,100 | 26,600 | ||

| Balance | 0 | ||

Rent Expense account:

| Rent Expense | |||

| 0 | |||

| 5,400 | 5,400 | ||

| Balance | 0 | ||

Supplies Expense account:

| Salaries Expense | |||

| 0 | |||

| 1,300 | 1,300 | ||

| Balance | 0 | ||

Utilities Expense account:

| Utilities Expense | |||

| 2,400 | |||

| 200 | 2,600 | ||

| Balance | 0 | ||

7.

Prepare the post-closing trial balance.

7.

Explanation of Solution

Post-closing trial balance: It is a trial balance that is prepared after the closing entries are recorded. It includes only the balance sheet accounts as the income statement accounts are closed to the income summary.

Prepare a post-closing trial balance.

|

CT Music Academy Post-Closing Trial Balance For the Year Ended December 31, 2021 | ||

| Accounts |

Debit ($) |

Credit ($) |

| Cash | 10,300 | |

| Accounts receivable | 9,500 | |

| Interest receivable | 800 | |

| Supplies | 700 | |

| Prepaid rent | 1,800 | |

| Land | 78,000 | |

| Notes receivable | 20,000 | |

| Accounts payable | 7,700 | |

| Salaries payable | 2,100 | |

| Deferred revenue | 2,000 | |

| Utilities payable | 200 | |

| Common stock | 79,000 | |

| Retained earnings | 30,100 | |

| Total | $121,100 | $121,100 |

Table (7)

Want to see more full solutions like this?

Chapter 3 Solutions

Financial Accounting

- Please provide the solution to this general accounting question with accurate financial calculations.arrow_forwardI need help with this financial accounting question using standard accounting techniques.arrow_forwardI need help solving this general accounting question with the proper methodology.arrow_forward

- Please help me solve this general accounting question using the right accounting principles.arrow_forwardCan you solve this general accounting question with the appropriate accounting analysis techniques?arrow_forwardCan you provide a detailed solution to this financial accounting problem using proper principles?arrow_forward

- I am searching for the most suitable approach to this financial accounting problem with valid standards.arrow_forwardOmega Retail had accounts receivable of $450,000 at year-end. Based on historical data, the company estimates that 3% of accounts receivable will be uncollectible. The Allowance for Doubtful Accounts had a credit balance of $2,800 before adjustment. Calculate the required bad debt expense for the year.arrow_forwardCan you solve this general accounting problem with appropriate steps and explanations?arrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education