Concept explainers

Videos

Finlon Upholstery, Inc. uses a

Finlon applies manufacturing

Job no. 2077 was completed in January 20x2; there was no work in process at year-end. All jobs produced during 20x2 were sold with the exception of job no. 2143, which contained direct-material costs of $156,000 and direct-labor charges of $85,000. The company charges any under- or overapplied overhead to Cost of Goods Sold.

Required:

- 1. Determine the company’s predetermined overhead application rate.

- 2. Determine the additions to the Work-in-Process Inventory account for direct material used, direct labor, and manufacturing overhead.

- 3. Compute the amount that the company would disclose as finished-goods inventory on the December 31, 20x2, balance sheet.

- 4. Prepare the

journal entry needed to record the year’s completed production. - 5. Compute the amount of under- or overapplied overhead at year-end, and prepare the necessary journal entry to record its disposition.

- 6. Determine the company’s 20x2 cost of goods sold.

- 7. Would it be appropriate to include selling and administrative expenses in either manufacturing overhead or cost of goods sold? Briefly explain.

1.

Calculate the amount of Company F’s predetermined overhead application rate.

Explanation of Solution

Predetermined Overhead Rate: Predetermined overhead rate is a measure used to allocate the estimated manufacturing overhead cost to the products or job orders during a particular period. This is generally evaluated at the beginning of each reporting period. The evaluation takes into account the estimated manufacturing overhead cost and the estimated allocation base that includes direct labor hours, direct labor in dollars, machine hours and direct materials.

Calculate the amount of Company F’s predetermined overhead application rate.

Thus, the amount of Company F’s predetermined overhead application rate is 130% of direct labor cost.

2.

Calculate the additions that are made to the work-in-process inventory account for direct materials used, direct labor, and manufacturing overhead.

Explanation of Solution

Work-in-process is the middle part of raw materials and finished goods. This inventory is the portion of the manufactured inventory for which the process has been started but not yet completed.

Calculate the additions that are made to the work-in-process inventory account for direct materials used, direct labor, and manufacturing overhead.

| Particulars | Amount ($) |

| Direct materials used | $5,600,000 |

| Direct labor | $4,350,000 |

| Manufacturing overhead | $5,655,000 |

| Total | $15,605,000 |

Table (1)

Thus, the total addition (debits) made to work-in process inventory account is $15,605,000.

3.

Identify the amount that would be disclosed by the company as finished goods inventory on the balance sheet as of December 31, 20x2.

Explanation of Solution

Finished goods inventory are completely ready for sale after completing the production process.

The amount that would be disclosed by the company as finished goods inventory on the balance sheet as of December 31, 20x2 is $351,500

4.

Prepare the journal entry in the books of Company F to record the year’s completed production.

Explanation of Solution

Prepare the journal entry in the books of Company F to record the year’s completed production.

| Date | Account title and explanation | Debit ($) | Credit ($) |

| Finished-goods inventory | 15,761,800 | ||

| Work-in-process inventory | 15,761,800 | ||

| (To record the company’s completed production) |

Table (2)

5.

Calculate the amount of under-applied or over-applied at year end and record its disposition.

Explanation of Solution

Under-applied overhead:

When there is a debit balance in the manufacturing overhead account during the month end, it indicates that overheads applied to jobs are less than the actual overhead cost incurred by the business. Therefore, the debit balance in the manufacturing overhead account is referred to as under-applied overhead.

Over-applied overhead:

When there is a credit balance in the manufacturing overhead account during the month end, indicates that overheads applied to jobs is more than the actual overhead cost incurred by the business. Therefore, the credit balance in the manufacturing overhead account is referred to as over- applied overhead.

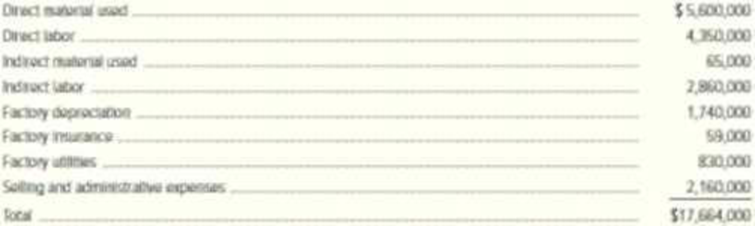

Step 1: calculate the amount of actual overhead.

| Particulars | Amount ($) |

| Indirect materials used | $65,000 |

| Indirect labor | $2,860,000 |

| Factory depreciation | $1,740,000 |

| Factory insurance | $59,000 |

| Factory utilities | $830,000 |

| Total | $5,554,000 |

Table (3)

Step 2: Calculate the amount of under-applied or over-applied overhead.

Working note (1):

Calculate the amount of applied overhead.

Thus, the overhead is over-applied by $101,000.

Prepare the journal entry.

| Date | Account title and explanation | Debit ($) | Credit ($) |

| Manufacturing overhead | 101,000 | ||

| Cost of goods sold | 101,000 | ||

| (To record the company’s completed production) |

Table (4)

6.

Calculate the cost of goods sold of Company F for the year 20x2.

Explanation of Solution

Cost of goods sold: Cost of goods sold is the total of all the expenses incurred by a company to sell the goods during the given period.

Calculate the cost of goods sold of Company F for the year 20x2.

| Particulars | Amount ($) |

| Finished-goods inventory, January 1 | $0 |

| Add: Cost of goods manufactured | $15,761,800 |

| Cost of goods available for sale | $15,761,800 |

| Less: Finished-goods inventory, December 31 | $351,500 |

| Unadjusted cost of goods sold | $15,410,300 |

| Less: Over applied overhead | $101,000 |

| Cost of goods sold | $15,309,300 |

Table (5)

Thus, the amount of cost of goods sold is $15,309,300.

7.

Explain whether it would be appropriate to include selling and administrative expenses in either manufacturing overhead or cost of goods sold.

Explanation of Solution

Selling and administrative expenses are the operating expenses of the company. These costs are considered as the period cost rather than the product costs. Hence, these costs are unrelated to manufacturing overhead and cost of goods sold. Thus, it cannot be included.

Want to see more full solutions like this?

Chapter 3 Solutions

Managerial Accounting: Creating Value in a Dynamic Business Environment

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning