Worksheet Devlin Company has prepared the following partially completed worksheet for the year ended December 31, 2019: The following additional information is available : (a) salaries accrued but unpaid total $250; (b) the $80 heat and light bill for December has not been recorded or paid; (c) depreciation expense totals $810 on the buildings and equipment; (d) interest accrued on the note payable totals $380 (this will be paid when the note is repaid); (e) the company leases a portion of its floor space to KT & Daniel Specialty Company for $50 per month, and KT & Daniel has not yet paid its December rent; (f) interest accrued on the note receivable totals $80; (g) bad debts expense is $70; and (h) the income tax rate is 30% on current income and is payable in the first quarter of 2017. Required: 1. Complete the worksheet. (Round to the nearest dollar.) 2. Prepare the company’s financial statements. 3. Prepare (a) adjusting and (b) closing entries in the general journal.

Worksheet Devlin Company has prepared the following partially completed worksheet for the year ended December 31, 2019: The following additional information is available : (a) salaries accrued but unpaid total $250; (b) the $80 heat and light bill for December has not been recorded or paid; (c) depreciation expense totals $810 on the buildings and equipment; (d) interest accrued on the note payable totals $380 (this will be paid when the note is repaid); (e) the company leases a portion of its floor space to KT & Daniel Specialty Company for $50 per month, and KT & Daniel has not yet paid its December rent; (f) interest accrued on the note receivable totals $80; (g) bad debts expense is $70; and (h) the income tax rate is 30% on current income and is payable in the first quarter of 2017. Required: 1. Complete the worksheet. (Round to the nearest dollar.) 2. Prepare the company’s financial statements. 3. Prepare (a) adjusting and (b) closing entries in the general journal.

Solution Summary: The author explains how to prepare the financial statements of Company D.

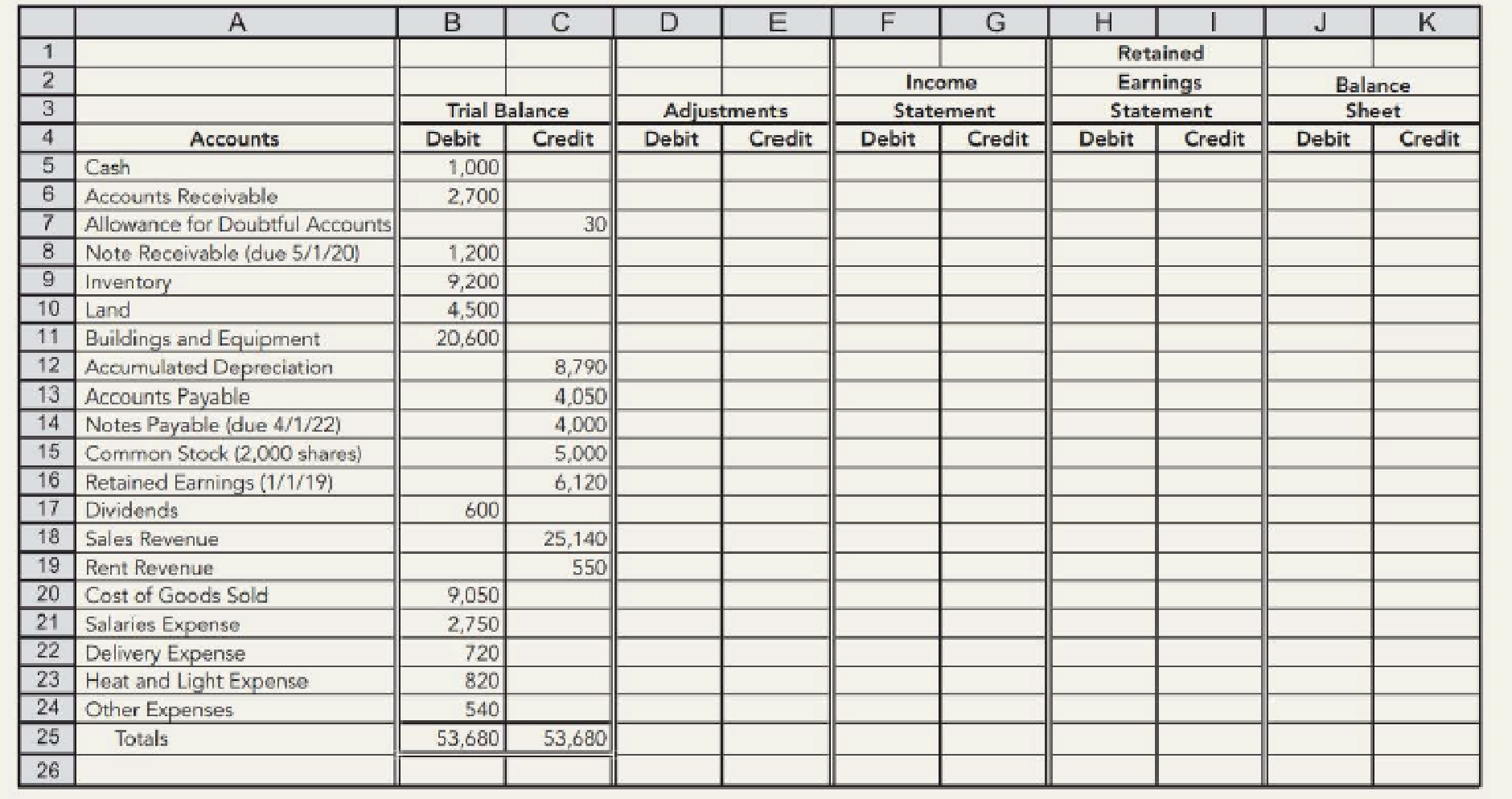

Worksheet Devlin Company has prepared the following partially completed worksheet for the year ended December 31, 2019:

The following additional information is available: (a) salaries accrued but unpaid total $250; (b) the $80 heat and light bill for December has not been recorded or paid; (c) depreciation expense totals $810 on the buildings and equipment; (d) interest accrued on the note payable totals $380 (this will be paid when the note is repaid); (e) the company leases a portion of its floor space to KT & Daniel Specialty Company for $50 per month, and KT & Daniel has not yet paid its December rent; (f) interest accrued on the note receivable totals $80; (g) bad debts expense is $70; and (h) the income tax rate is 30% on current income and is payable in the first quarter of 2017.

Required:

1. Complete the worksheet. (Round to the nearest dollar.)

2. Prepare the company’s financial statements.

3. Prepare (a) adjusting and (b) closing entries in the general journal.

Definition Definition Financial statement that provides a snapshot of an organization's financial position at a specific point in time. It summarizes a company's assets, liabilities, and shareholder's equity, detailing what the company owns, what it owes, and what is left over for its owners. The balance sheet serves as a crucial tool to assess the financial health and stability of a company, as well as to help management make informed decisions about its future investments and financial obligations.

For Eckstein Company, the predetermined overhead rate is 118% of direct labor cost. During the month, Eckstein incurred $119,000 in factory labor costs, of which $98,200 is direct labor and $26,400 is indirect labor. The actual overhead incurred was $132,600. Compute the amount of manufacturing overhead applied during the month. Determine the amount of under- or overapplied manufacturing overhead.??

Provide answer with calculation

Hello tutor please provide correct answer general accounting

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.

7.2 Ch 7: Notes Payable and Interest, Revenue recognition explained; Author: Accounting Prof - making it easy, The finance storyteller;https://www.youtube.com/watch?v=wMC3wCdPnRg;License: Standard YouTube License, CC-BY

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning