Videos

MASTERY PROBLEM

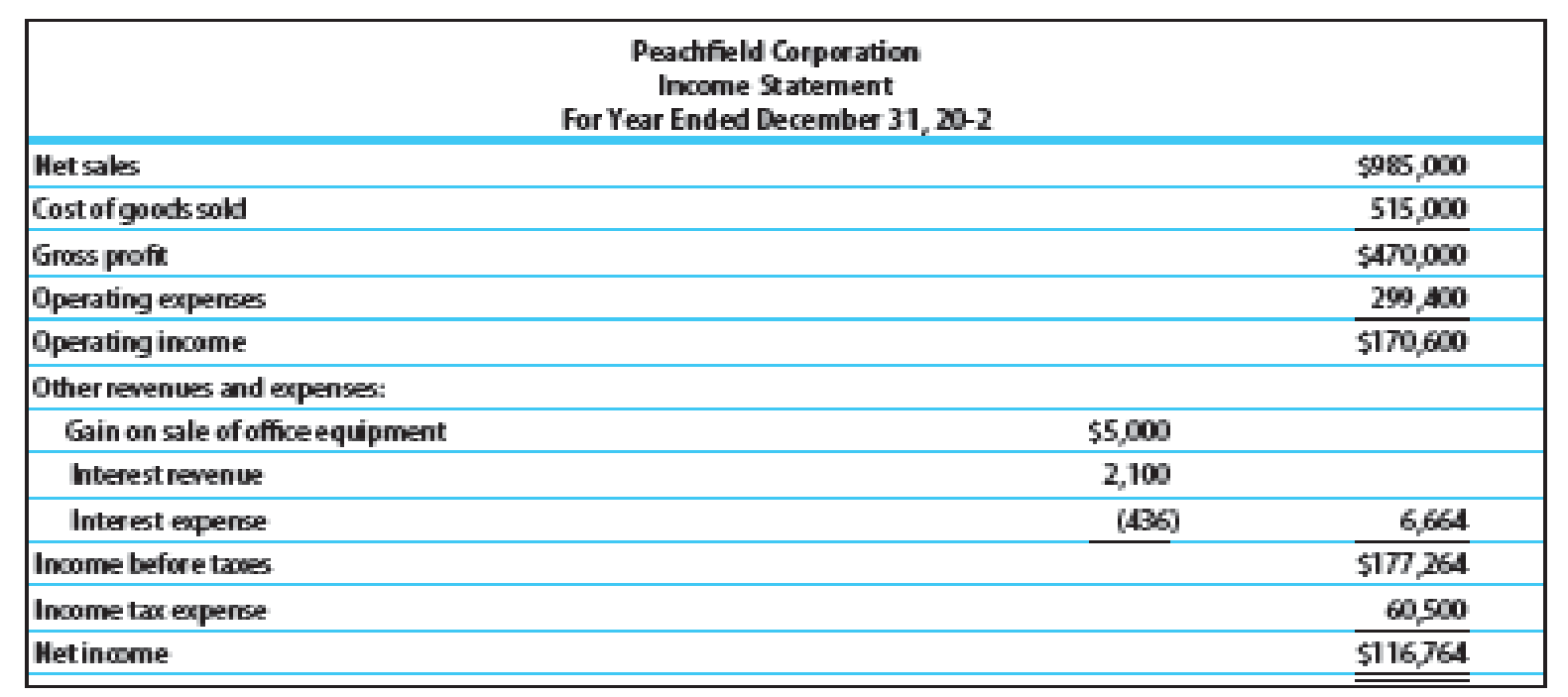

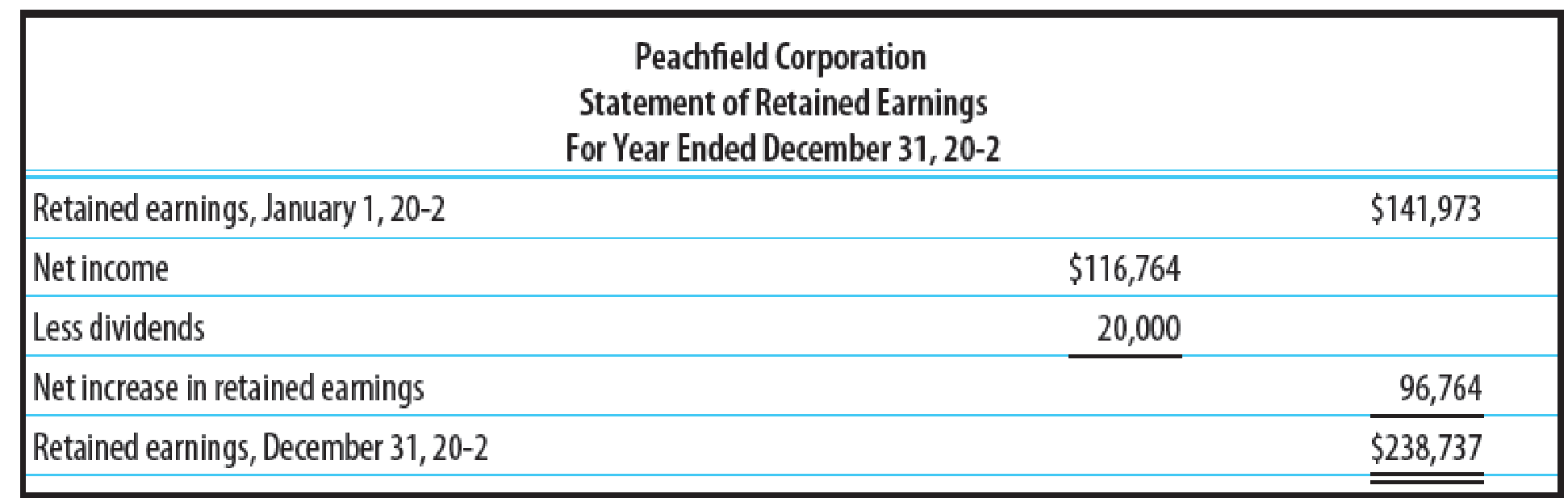

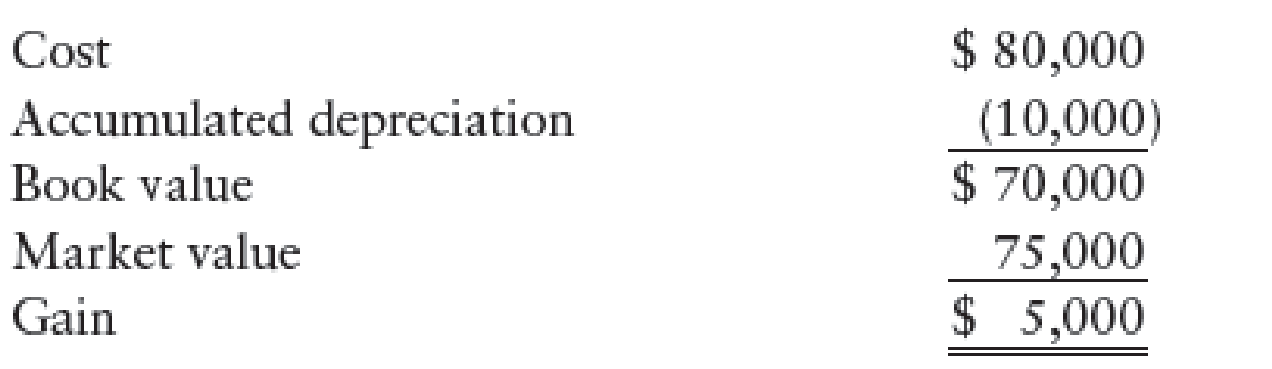

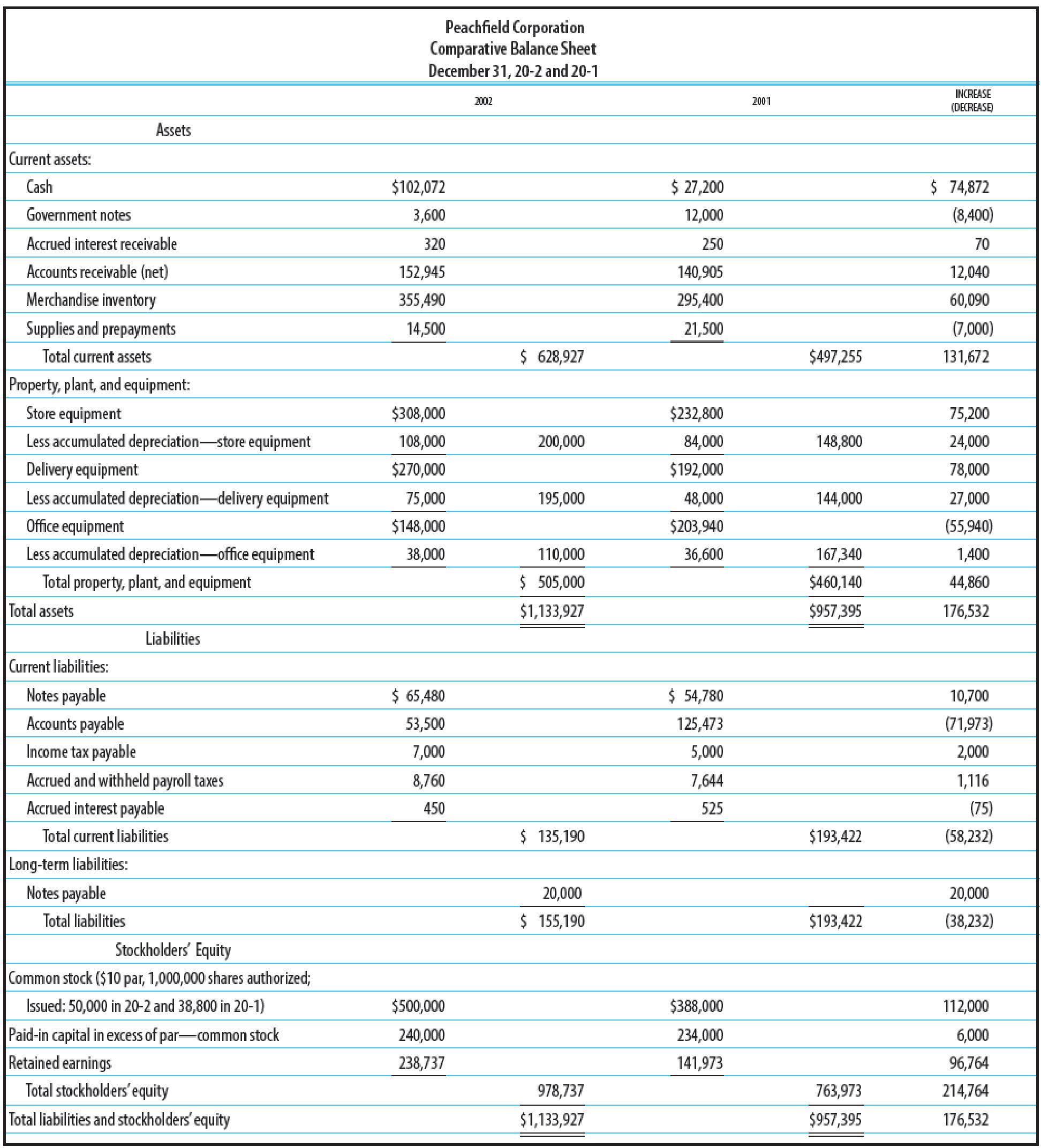

Financial statements for Peachfield Corporation as well as additional information relevant to

Additional information:

1. Office equipment was sold during the year for $75,000.

2.

3. No other equipment was sold during the year. The following purchases were made for cash.

4. Declared and paid cash dividends of $20,000.

5. Issued 11,200 shares of $10 par common stock for $118,000.

6. Issued a note payable for $10,700.

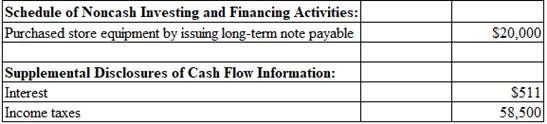

7. Additional store equipment was acquired by issuing a long-term note payable for $20,000.

REQUIRED

1. Prepare a statement of cash flows explaining the change in cash and cash equivalents.

2. Reconcile cash and cash equivalents at the bottom of the statement of cash flows.

1.

Prepare a statement of cash flows explaining the change in cash and cash equivalents.

Explanation of Solution

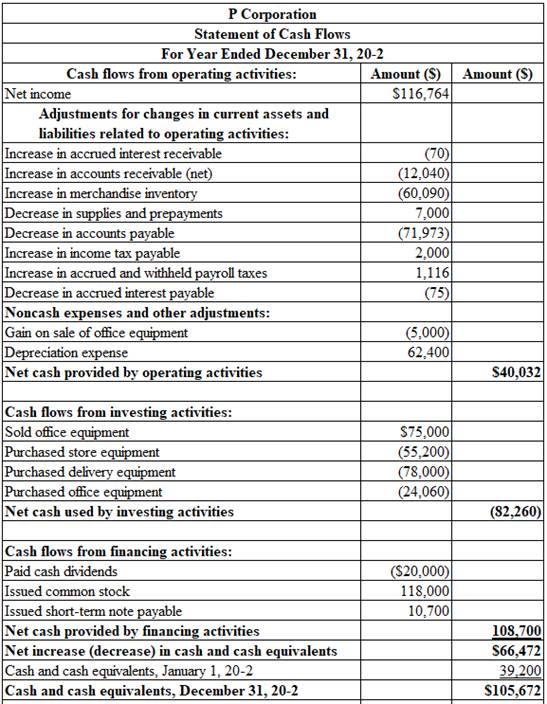

Statement of cash flows: This statement reports all the cash transactions which are responsible for inflow and outflow of cash, and result of these transactions is reported as ending balance of cash at the end of reported period. Statement of cash flows includes the changes in cash balance due to operating, investing, and financing activities.

Indirect method: Under indirect method, net income is reported first, and then non-cash expenses, losses from fixed assets, and changes in opening balances and ending balances of current assets and current liabilities are adjusted to reconcile the net income balance.

Cash flows from operating activities: Operating activities refer to the normal activities of a company to carry out the business.

The below table shows the way of calculation of cash flows from operating activities:

| Cash flows from operating activities (Indirect method) |

| Net income: |

| Add: Decrease in current assets |

| Increase in current liability |

| Depreciation expense and amortization expense |

| Loss on sale of plant assets |

| Deduct: Increase in current assets |

| Decrease in current liabilities |

| Gain on sale of plant assets |

| Net cash provided from or used by operating activities |

Table (1)

Cash flows from investing activities: Investing activities refer to the activities carried out by a company for acquisition of long term assets. It includes the purchase or sale of equipment or land, or marketable securities, which is used for business operations.

The below table shows the way of calculation of cash flows from investing activities:

| Cash flows from investing activities |

| Add: Proceeds from collection of loan made to borrowers |

| Sale of marketable securities / investments |

| Sale of property, plant and equipment |

| Proceeds from discounting notes receivables |

| Deduct: Purchase of fixed assets/long-lived assets |

| Loan made by the company to others |

| Purchase of marketable securities |

| Net cash provided from or used by investing activities |

Table (2)

Cash flows from financing activities: Financing activities refer to the activities carried out by a company to mobilize funds to carry out the business activities. It includes raising cash from long-term debt or payment of long-term debt, which is used for business operations.

The below table shows the way of calculation of cash flows from financing activities:

| Cash flows from financing activities |

| Add: Issuance of common stock |

| Proceeds from borrowings by signing of a mortgage |

| Proceeds from sale of treasury stock |

| Proceeds from issuance of debt |

| Deduct: Payment of dividend |

| Repayment of debt |

| Repayment of the principal on loan |

| Redemption of debt |

| Purchase of treasury stock |

| Net cash provided from or used by financing activities |

Table (3)

Prepare a statement of cash flows explaining the change in cash and cash equivalents.

Table (1)

Working notes:

Compute the amount of cash paid for interest in 20-2.

Compute the amount of cash paid for income taxes in 20-2.

2.

Reconcile cash and cash equivalents at the bottom of the statement of cash flows.

Explanation of Solution

Cash: Cash is the money readily available in the form of currency. Since cash can be easily converted into other types of assets, it is reported as first item in the assets section as the most liquid asset.

Cash equivalents: Cash equivalents are the near-cash items, which are readily convertible into cash. Cash equivalents have a maturity period of three months, or less than 3 months. Cash equivalents are reported along with cash in the assets section of the balance sheet, as ‘Cash and cash equivalents’.

Calculate the amount of cash and cash equivalents at January 1, 20-2.

Calculate the amount of cash and cash equivalents at December 31, 20-2.

Want to see more full solutions like this?

Chapter 23 Solutions

College Accounting, Chapters 1-27

- What is the amount of the net fixed assets?arrow_forward9 A B C D E 4 Ramsey Miller Style, Inc. manufactures a product which requires 15 pounds of direct materials at a cost of $8 5 per pound and 5.0 direct labor hours at a rate of $17 per hour. Variable overhead is budgeted at a rate of $3 per direct labor hour. Budgeted fixed overhead is $433,000 per month. The company's policy is to end each month with direct materials inventory equal to 45% of the next month's direct materials requirement, and finished 7 goods inventory equal to 60% of next month's sales. August sales were 13,400 units, and marketing expects 8 sales to increase by 500 units in each of the upcoming three months. At the end of August, the company had 9 95,850 pounds of direct materials in inventory, and 8,340 units in finished goods inventory. 10 11 August sales 12 Expected increase in monthly sales 13 Desired ending finished goods (units) 14 Selling price per unit 15 Direct materials per unit 16 Direct materials cost 17 Direct labor hours (DLHS) per unit 18 Direct labor…arrow_forwardSherrod, Incorporated, reported pretax accounting income of $84 million for 2024. The following information relates to differences between pretax accounting income and taxable income: a. Income from installment sales of properties included in pretax accounting income in 2024 exceeded that reported for tax purposes by $3 million. The installment receivable account at year-end 2024 had a balance of $4 million (representing portions of 2023 and 2024 installment sales), expected to be collected equally in 2025 and 2026. b. Sherrod was assessed a penalty of $4 million by the Environmental Protection Agency for violation of a federal law in 2024. The fine is to be paid in equal amounts in 2024 and 2025. c. Sherrod rents its operating facilities but owns one asset acquired in 2023 at a cost of $88 million. Depreciation is reported by the straight-line method, assuming a four-year useful life. On the tax return, deductions for depreciation will be more than straight- line depreciation the…arrow_forward

- Direct materials price variancearrow_forward$ 36,000 204,000 The Drysdale, Koufax, and Marichal partnership has the following balance sheet immediately prior to liquidation: Cash Noncash assets Liabilities Drysdale, loan $ 50,000 10,000 Total assets $ 240,000 Drysdale, capital (50%) Koufax, capital (30%) Marichal, capital (20%) Total liabilities and capital 70,000 60,000 50,000 $ 240,000 Required: a-1. Determine the maximum loss that can be absorbed in Step 1. Then, assuming that this loss has been incurred, determine the next maximum loss that can be absorbed in Step 2. a-2. Liquidation expenses are estimated to be $15,000. Prepare a predistribution schedule to guide the distribution of cash. b. Assume that assets costing $74,000 are sold for $60,000. How is the available cash to be divided? Complete this question by entering your answers in the tabs below.arrow_forwardCalculate GP ratio round answers to decimal placearrow_forward

- What is the gross profit percentage for this periodarrow_forwardThe company's gross margin percentage is ?arrow_forwardProblem 19-13 (Algo) Shoney Video Concepts produces a line of video streaming servers that are linked to personal computers for storing movies. These devices have very fast access and large storage capacity. Shoney is trying to determine a production plan for the next 12 months. The main criterion for this plan is that the employment level is to be held constant over the period. Shoney is continuing in its R&D efforts to develop new applications and prefers not to cause any adverse feelings with the local workforce. For the same reason, all employees should put in full workweeks, even if that is not the lowest-cost alternative. The forecast for the next 12 months is MONTH FORECAST DEMAND January February March April 530 730 830 530 May June 330 230 July 130 August 130 September 230 October 630 730 800 November December Manufacturing cost is $210 per server, equally divided between materials and labor. Inventory storage cost is $4 per unit per month and is assigned based on the ending…arrow_forward

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning