Concept explainers

Videos

Journal entries and

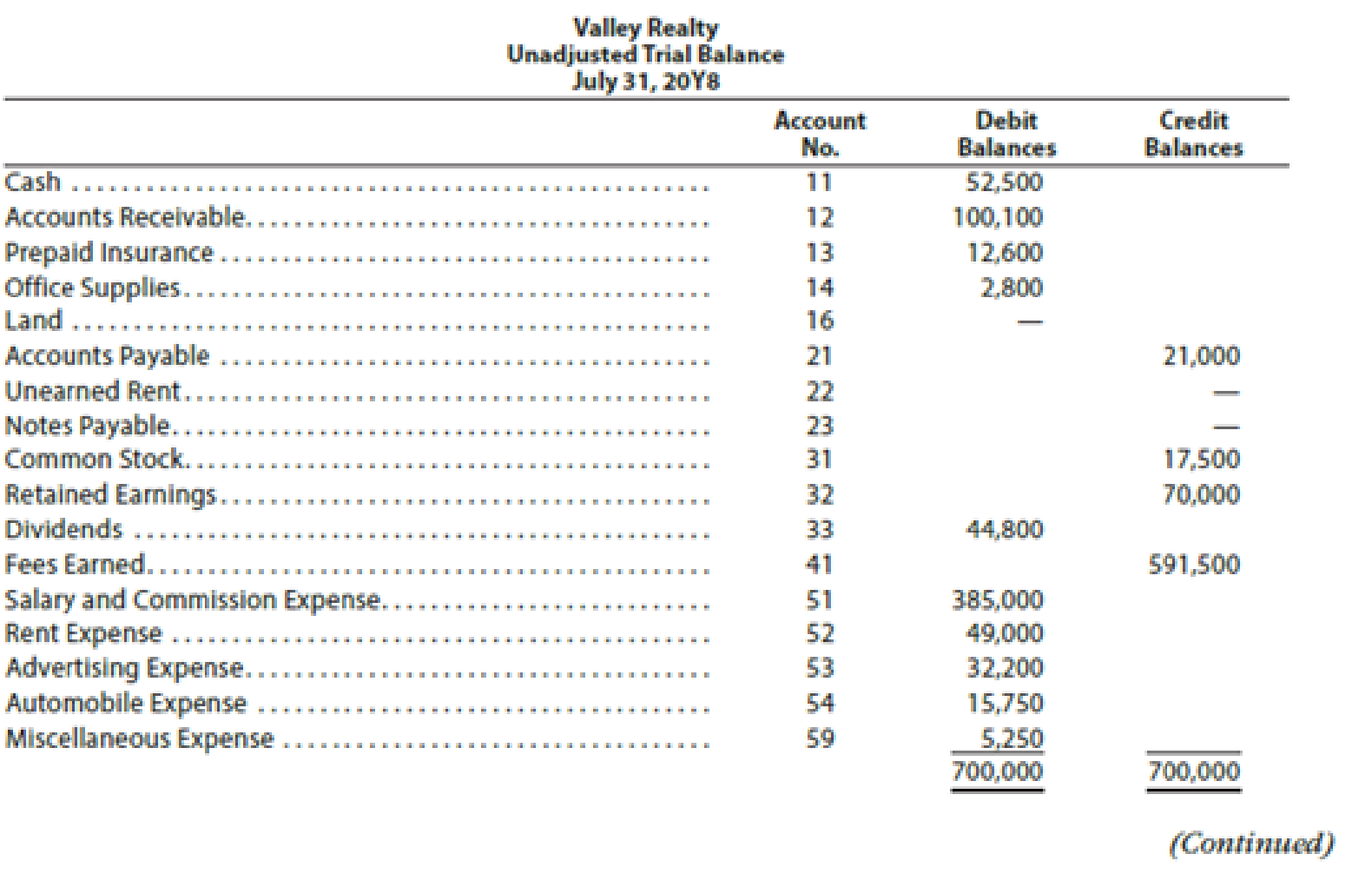

Valley Realty acts as an agent in buying, selling, renting, and managing real estate. The unadjusted trial balance on July 31, 20Y8, follows:

The following business transactions were completed by Valley Realty during August 20Y8:

Aug. 1. Purchased office supplies on account, $3,150.

2. Paid rent on office for month, $7,200.

3. Received cash from clients on account, $83,900.

5. Paid insurance premiums, $12,000.

9. Returned a portion of the office supplies purchased on August 1, receiving full credit for their cost, $400.

17. Paid advertising expense, $8,000.

23. Paid creditors on account, $13,750.

Enter the following transactions on Page 19 of the two-column journal:

29. Paid miscellaneous expenses, $1,700.

30. Paid automobile expense (including rental charges for an automobile), $2,500.

31. Discovered an error in computing a commission during July; received cash from the salesperson for the overpayment, $2,000.

31. Paid salaries and commissions for the month, $53,000.

31. Recorded revenue earned and billed to clients during the month, $183,500.

31. Purchased land for a future building site for $75,000, paying $7,500 in cash and giving a note payable for the remainder.

31. Paid dividends, $1,000.

31. Rented land purchased on August 31 to a local university for use as a parking lot during football season (September, October, and November); received advance payment of $5,000.

Instructions

1. Record the August 1 balance of each account in the appropriate balance column of a four-column account, write Balance in the item section, and place a check mark (✓) in the Posting Reference column.

2. Journalize the transactions for August in a two-column journal beginning on Page 18.

3. Post to the ledger, extending the account balance to the appropriate balance column after each posting.

4. Prepare an unadjusted trial balance of the ledger as of August 31, 20Y8.

5. Assume that the August 31 transaction for dividends should have been $10,000. (a) Why did the unadjusted trial balance in (4) balance? (b) Journalize the correcting entry. (c) Is this error a transposition or slide?

(2) and (3)

Journalize the transactions of August in a two column journal beginning on page 18.

Explanation of Solution

Journal:

Journal is the book of original entry. Journal consists of the day today financial transactions in a chronological order. The journal has two aspects; they are debit aspect and the credit aspect.

Rules of debit and credit:

“An increase in an asset account, an increase in an expense account, a decrease in liability account, and a decrease in a revenue account should be debited.

Similarly, an increase in liability account, an increase in a revenue account and a decrease in an asset account, a decrease in an expenses account should be credited”.

Journalize the transactions of August in a two column journal beginning on page 18.

| Journal Page 18 | |||||

| Date | Description | Post. Ref | Debit ($) | Credit ($) | |

| 20Y8 | Office supplies | 14 | 3,150 | ||

| August | 1 | Accounts payable | 21 | 3,150 | |

| (To record the purchase of supplies of account) | |||||

| 2. | Rent expense | 52 | 7,200 | ||

| Cash | 11 | 7,200 | |||

| (To record the payment of rent) | |||||

| 3 | Cash | 11 | 83,900 | ||

| Accounts receivable | 12 | 83,900 | |||

| (To record the receipt of cash from clients) | |||||

| 5 | Prepaid insurance | 13 | 12,000 | ||

| Cash | 11 | 12,000 | |||

| (To record the payment of insurance premium) | |||||

| 9 | Accounts payable | 21 | 400 | ||

| Office supplies | 14 | 400 | |||

| (To record the payment made to creditors on account) | |||||

| 17 | Advertising expense | 53 | 8,000 | ||

| Cash | 11 | 8,000 | |||

| (To record the payment of advertising expense) | |||||

| 23 | Accounts payable | 21 | 13,750 | ||

| Cash | 11 | 13,750 | |||

| (To record the payment made to creditors on account) | |||||

Table (1)

| Journal Page 19 | |||||

| Date | Description | Post. Ref | Debit ($) | Credit ($) | |

| 20Y8 | 29 | Miscellaneous expense | 59 | 1,700 | |

| August | Cash | 11 | 1,700 | ||

| (To record the payment made for Miscellaneous expense) | |||||

| 30 | Automobile expense | 54 | 2,500 | ||

| Cash | 11 | 2,500 | |||

| (To record the payment made for automobile expense) | |||||

| 31 | Cash | 11 | 2,000 | ||

| Salary and commission expense | 51 | 2,000 | |||

| (To record the receipt of cash) | |||||

| 31 | Salary and commission expense | 51 | 53,000 | ||

| Cash | 11 | 53,000 | |||

| (To record the payment made for salary and commission expense) | |||||

| 31 | Accounts receivable | 12 | 183,500 | ||

| Fees earned | 41 | 183,500 | |||

| (To record the revenue earned and billed) | |||||

| 31 | Land | 16 | 75,000 | ||

| Cash | 11 | 7,500 | |||

| Notes payable | 23 | 67,500 | |||

| (To record the purchase of land party for cash and party on signing a note) | |||||

| 31 | Dividends | 33 | 1,000 | ||

| Cash | 11 | 1,000 | |||

| (To record the drawing made for personal use) | |||||

| 31 | Cash | 11 | 5,000 | ||

| Unearned rent | 22 | 5,000 | |||

| (To record the cash received for the service yet to be provide) | |||||

Table (2)

(1) and (3)

Record the beginning balances of each accounts in the appropriate balance column of a four-column account, and post them to the ledger extending the account balance to the appropriate balance column after each posting.

Explanation of Solution

Record the beginning balance in the general ledger:

| Account: Cash Account no. 11 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| August | 1 | Balance | ✓ | 52,500 | |||

| 2 | 18 | 7,200 | 45,300 | ||||

| 3 | 18 | 83,900 | 129,200 | ||||

| 5 | 18 | 12,000 | 117,200 | ||||

| 17 | 18 | 8,000 | 109,200 | ||||

| 23 | 18 | 13,750 | 95,450 | ||||

| 29 | 19 | 1,700 | 93,750 | ||||

| 30 | 19 | 2,500 | 91,250 | ||||

| 31 | 19 | 2,000 | 93,250 | ||||

| 31 | 19 | 53,000 | 40,250 | ||||

| 31 | 19 | 7,500 | 32,750 | ||||

| 31 | 19 | 1,000 | 31,750 | ||||

| 31 | 19 | 5,000 | 36,750 | ||||

Table (3)

| Account: Accounts Receivable Account no. 12 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| August | 1 | Balance | ✓ | 100,100 | |||

| 3 | 18 | 83,900 | 16,200 | ||||

| 31 | 19 | 183,500 | 199,700 | ||||

Table (4)

| Account: Prepaid Insurance Account no. 13 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| August | 1 | Balance | ✓ | 12,600 | |||

| 5 | 18 | 12,000 | 24,600 | ||||

Table (5)

| Account: Office Supplies Account no. 14 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| August | 1 | Balance | ✓ | 2,800 | |||

| 1 | 18 | 3,150 | 5,950 | ||||

| 9 | 18 | 400 | 5,550 | ||||

Table (6)

| Account: Land Account no. 16 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| August | 31 | 19 | 75,000 | 75,000 | |||

Table (7)

| Account: Accounts Payable Account no. 21 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| August | 1 | Balance | ✓ | 21,000 | |||

| 1 | 18 | 3,150 | 24,150 | ||||

| 9 | 18 | 400 | 23,750 | ||||

| 23 | 18 | 13,750 | 10,000 | ||||

Table (8)

| Account: Unearned Rent Account no. 22 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| August | 31 | 19 | 5,000 | 5,000 | |||

Table (9)

| Account: Notes Payable Account no. 23 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| August | 31 | 19 | 67,500 | 67,500 | |||

Table (11)

| Account: Common stock Account no. 31 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| August | 1 | Balance | ✓ | 17,500 | |||

Table (12)

| Account: Retained earnings Account no. 32 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| August | 1 | Balance | ✓ | 70,000 | |||

Table (13)

| Account: Dividends Account no. 33 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| August | 1 | Balance | ✓ | 44,800 | |||

| 31 | 19 | 1,000 | 45,800 | ||||

Table (13)

| Account: Fees earned Account no. 41 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| August | 1 | Balance | ✓ | 591,500 | |||

| 31 | 19 | 183,500 | 775,000 | ||||

Table (14)

| Account: Salary and commission expense Account no. 51 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| August | 1 | Balance | ✓ | 385,000 | |||

| 31 | 19 | 2,000 | 383,000 | ||||

| 31 | 19 | 53,000 | 436,000 | ||||

Table (15)

| Account: Rent expense Account no. 52 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| August | 1 | Balance | ✓ | 49,000 | |||

| 2 | 18 | 7,200 | 56,200 | ||||

Table (16)

| Account: Advertising expense Account no. 53 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| August | 1 | Balance | ✓ | 32,200 | |||

| 17 | 18 | 8,000 | 40,200 | ||||

Table (17)

| Account: Automobile expense Account no. 54 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| August | 1 | Balance | ✓ | 15,750 | |||

| 30 | 19 | 2,500 | 18,250 | ||||

Table (19)

| Account: Miscellaneous expense Account no. 59 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| August | 1 | Balance | ✓ | 5,250 | |||

| 29 | 19 | 1,700 | 6,950 | ||||

Table (20)

(4)

Prepare an unadjusted trial balance of Company V at August 31, 20Y8.

Explanation of Solution

Unadjusted trial balance:

The unadjusted trial balance is the summary of all the ledger accounts that appears on the ledger accounts before making adjusting journal entries.

Prepare an unadjusted trial balance of Company V at August 31, 20Y8 as follows:

|

Company V Unadjusted Trial Balance August 31, 20Y8 | |||

| Particulars |

Account No. |

Debit $ | Credit $ |

| Cash | 11 | 36,750 | |

| Accounts receivable | 12 | 199,700 | |

| Prepaid insurance | 13 | 24,600 | |

| Office supplies | 14 | 5,550 | |

| Land | 16 | 75,000 | |

| Accounts payable | 21 | 10,000 | |

| Unearned rent | 22 | 5,000 | |

| Notes payable | 23 | 67,500 | |

| Common stock | 31 | 17,500 | |

| Retained earnings | 32 | 70,000 | |

| Dividends | 33 | 45,800 | |

| Fees earned | 41 | 775,000 | |

| Salaries and commission expense | 51 | 436,000 | |

| Rent expense | 52 | 56,200 | |

| Advertising expense | 53 | 40,200 | |

| Automobile expense | 54 | 18,250 | |

| Miscellaneous expense | 59 | 6,950 | |

| Total | 945,000 | 945,000 | |

Table (20)

The debit column and credit column of the unadjusted trial balance are agreed, both having balance of $945,000.

(5) (a)

Explain the reason for unadjusted trial balance in (4) is balanced.

Explanation of Solution

Unadjusted trial balance:

The unadjusted trial balance is the summary of all the ledger accounts that appears on the ledger accounts before making adjusting journal entries.

The unadjusted trial balance in (4) would still balance, since the debit equalized the credit in the original journal entry.

(5) (b)

Journalize the correcting entry

Explanation of Solution

The correcting entry is as follows:

| Journal Page 19 | |||||

| Date | Description | Post. Ref | Debit ($) | Credit ($) | |

| 20Y8 | Dividends | 33 | 9,000 | ||

| August | 31 | Cash | 11 | 9,000 | |

| (To record the correcting entry) | |||||

Table (21)

Working notes:

(5) (c)

Identify whether the error made is a slide or transposition.

Explanation of Solution

Slide error:

A slide error occurs, when the decimal point of an amount has been misplaced.

The drawings account balance recorded as $10,000 instead of $1,000 is a slide error. Since, the decimal point of the amount has been misplaced.

Want to see more full solutions like this?

Chapter 2 Solutions

Financial and Managerial Accounting - CengageNow

- Kindly help me with accounting questionsarrow_forwardAn ARO is to be calcualted for the Leashold improvement made in 2024. The book life given is 10 years (based on the lease) and it is Straight line depreciation.What are the amounts to capitalize and ARO when the given info is 1. total Capitalized cost is 1,100,000 2. estimated cost to tear down $200,000 the ridsk free Rate of interest is 3%, the firm assumes annual inflation of 2% - What is the future value of single payment (use inflation rate) - What is the present value of single payment (use risk free rate of return) What would be the entries for the years to be madearrow_forwardMETLOCK COMPANY Comparative Balance Sheet Assets Dec. 31, 2025 Dec. 31, 2024 Cash $33,900 $12,500 Accounts receivable 17,500 14,500 Inventory Prepaid insurance Stock investments 26,400 19,200 8,500 10,000 -0- 15,700 Equipment Accumulated depreciation-equipment Total assets 88,000 44,000 (15,500) (14,800) $158,800 $101,100 Liabilities and Stockholders' Equity Accounts payable $34,700 $7,900 Bonds payable 37,000 49,400 Common stock 40,400 24,300 Retained earnings 46,700 19,500 Total liabilities and stockholder's equity $158,800 $101,100 Additional information: 1 Net income for the year ending December 31, 2025 was $36,000. 2 Cash dividends of $8,800 were declared and paid during the year. 3. Stock investments that had a book value of $15,700 were sold for $12,000. 4. Sales for 2025 are $150,000. Prepare a statement of cash flows for the year ended December 31, 2025 using the indirect method. (Show amounts that decrease cash flow with either a-sign eg-15,000 or in parenthesise.g.…arrow_forward

- Kindly give a step by step details explaination of each answers especially question 5 and 6. Please, don't just give answers without explaining how we arrived at the answer. Thanks! The following are the questions: 1. What is the general journal entries the transactions described for Hogan Company. All sales are on account. Use the date of December 31 to make the entry to summarize sales for the year in the old territory and new territory. 2. Make the journal entries to record the write-off of accounts in the new territory. 3. Make the journal entry to record the write-off of accounts in the old territory. 4. Make the entry on December 31 to record uncollectible accounts expense for 20X1 for both territories. Make the calculation using the percentages developed by Hogan. 5. Let’s say the Allowance for Doubtful Accounts had a credit balance of $24,800 on September 30 before any of the above entries were made. Calculate the balance in the allowance account after…arrow_forwardFinancial accountingarrow_forwardGeneral Accountingarrow_forward

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:CengagePrinciples of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:CengagePrinciples of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning