Intermediate Accounting: Reporting And Analysis

3rd Edition

ISBN: 9781337788281

Author: James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher: Cengage Learning

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 18, Problem 20E

Required:

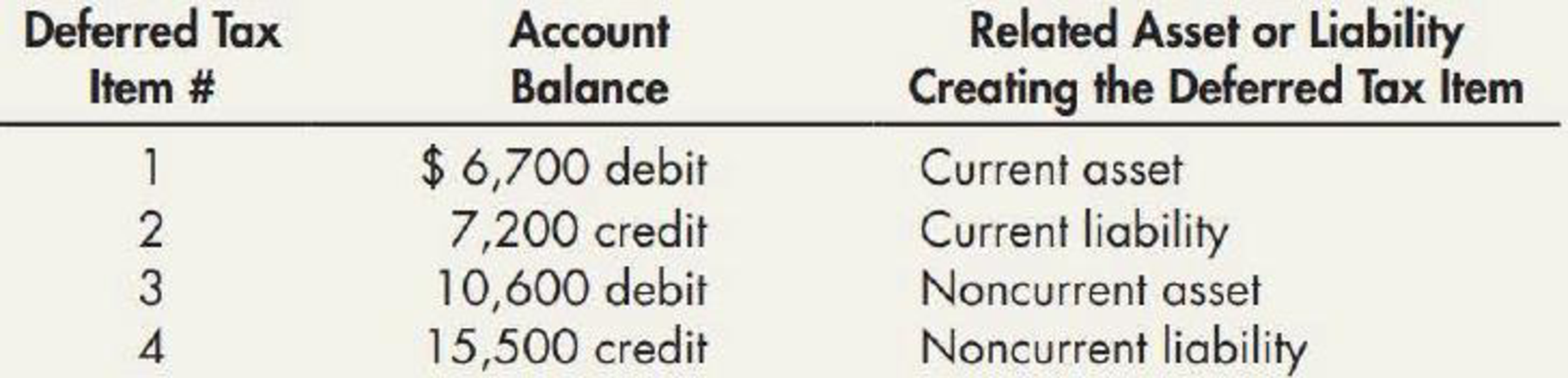

Show how the preceding deferred tax items are reported on Thiel’s December 31, 2019, balance sheet.

Expert Solution & Answer

Trending nowThis is a popular solution!

Students have asked these similar questions

Financial Accounting

Provide solution this following requirements on these financial accounting question

What is company bs net income?

Chapter 18 Solutions

Intermediate Accounting: Reporting And Analysis

Ch. 18 - What source is used to determine income tax...Ch. 18 - Prob. 2GICh. 18 - Prob. 3GICh. 18 - Prob. 4GICh. 18 - Prob. 5GICh. 18 - Prob. 6GICh. 18 - What are the three characteristics of a liability,...Ch. 18 - Prob. 8GICh. 18 - When does a corporation establish a valuation...Ch. 18 - List the steps necessary to measure and record a...

Ch. 18 - Prob. 11GICh. 18 - Prob. 12GICh. 18 - Prob. 13GICh. 18 - Prob. 14GICh. 18 - Prob. 15GICh. 18 - Describe an operating loss carryforward. List the...Ch. 18 - Prob. 17GICh. 18 - Prob. 18GICh. 18 - Prob. 19GICh. 18 - Prob. 20GICh. 18 - Prob. 21GICh. 18 - Prob. 22GICh. 18 - Prob. 23GICh. 18 - Which of the following is not a cause of a...Ch. 18 - Which of the following is an argument in favor of...Ch. 18 - Prob. 3MCCh. 18 - Prior to and during 2019, Shadrach Company...Ch. 18 - At the beginning of 2019, Conley Company purchased...Ch. 18 - Oliver Company earned taxable income of 7,500...Ch. 18 - Prob. 7MCCh. 18 - Prob. 8MCCh. 18 - Brooks Company reported a prior period adjustment...Ch. 18 - Which component of current income is not disclosed...Ch. 18 - Parker Company identifies depreciation as the only...Ch. 18 - Refer to RE18-1. Assume that Parkers taxable...Ch. 18 - In the current year, Madison Corporation had...Ch. 18 - Refer to RE18-3. Prepare the additional journal...Ch. 18 - Turnip Company purchased an asset at a cost of...Ch. 18 - Prob. 6RECh. 18 - Compute Radish Companys taxable income given the...Ch. 18 - Sky Company reports a pretax operating loss of...Ch. 18 - Prob. 9RECh. 18 - Kline Company has the following items of pretax...Ch. 18 - Barth James Inc. has the following deferred tax...Ch. 18 - Cole Company had a deferred tax liability of 1,000...Ch. 18 - Future Taxable Amount Arrow Company began...Ch. 18 - Change in Tax Rates At the end of 2019, Sentry...Ch. 18 - Temporary Difference At the end of 2019, its first...Ch. 18 - Single Temporary Difference: Multiple Rates At the...Ch. 18 - Prob. 5ECh. 18 - Valuation Account At the end of 2019, its first...Ch. 18 - Deferred Tax Asset and Valuation Account Zeta...Ch. 18 - Incomc Taxes Then Company has been in operation...Ch. 18 - Prob. 9ECh. 18 - Multiple Temporary Differences Vickers Company...Ch. 18 - Multiple Tax Rates For the year ended December 31,...Ch. 18 - Temporary and Permanent Differences Lin has just...Ch. 18 - Temporary and Permanent Differences Assume the...Ch. 18 - Operating Loss At the end of 2019, Keil Company...Ch. 18 - Operating Loss At the end of 2019, its first year...Ch. 18 - Operating Loss Baxter Company began operations in...Ch. 18 - Intraperiod Tax Allocation Wright Company reports...Ch. 18 - Prob. 18ECh. 18 - Prob. 19ECh. 18 - Balance Sheet Presentation Thiel Company reports...Ch. 18 - Uncertain Tax Position At the end of the current...Ch. 18 - Definitions The FASB has defined several terms in...Ch. 18 - Temporary and Permanent Differences In the current...Ch. 18 - Multiple Temporary Differences Wilcox Company has...Ch. 18 - Interperiod Tax Allocation Klerk Company had four...Ch. 18 - Prob. 5PCh. 18 - Interperiod Tax Allocation Quick Company reports...Ch. 18 - Deferred Tax Liability: Depreciation At the...Ch. 18 - Deferred Tax Liability: Depreciation Gire Company...Ch. 18 - Interperiod Tax Allocation Peterson Company has...Ch. 18 - Operating Loss Ross Company has been in business...Ch. 18 - Prob. 11PCh. 18 - Comprehensive Colt Company reports pretax...Ch. 18 - Prob. 13PCh. 18 - Comprehensive Jayryan Company sells products in a...Ch. 18 - Prob. 1CCh. 18 - Prob. 2CCh. 18 - Prob. 3CCh. 18 - Interperiod and Intraperiod Tax Allocation Income...Ch. 18 - Prob. 5CCh. 18 - Intel-period Tax Allocation Chris Green, CPA, is...Ch. 18 - Prob. 7CCh. 18 - Analyzing Coca-Colas Income Tax Disclosures Obtain...Ch. 18 - Prob. 9C

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:Cengage Learning

Chapter 19 Accounting for Income Taxes Part 1; Author: Vicki Stewart;https://www.youtube.com/watch?v=FMjwcdZhLoE;License: Standard Youtube License