Concept explainers

Videos

a.

Find the regression equation.

a.

Answer to Problem 53CE

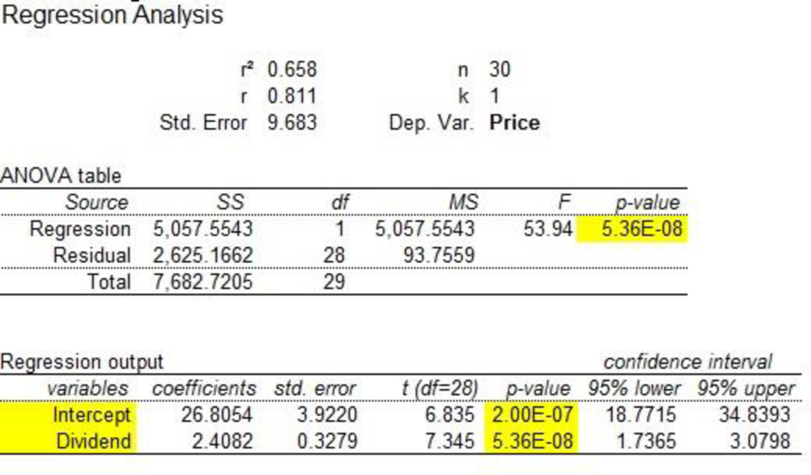

The regression equation is

Explanation of Solution

Calculation:

The values of x and y are given.

Regression equation:

Software procedure:

Step-by-step procedure to obtain the ‘Regression equation’ using the MegaStat software:

- In an EXCEL sheet enter the data values of x and y.

- Go to Add-Ins > MegaStat >

Correlation /Regression >Regression Analysis . - Select input

range as ‘Sheet1!$B$2:$B$16’ under Y/Dependent variable. - Select input range ‘Sheet1!$A$2:$A$16’ under X/Independent variables.

- Click on OK.

Output obtained using the MegaStat software is as given below:

From the output, the regression equation is

Where, y is the price per share and x is the dividend.

b.

Test whether the slope is significant or not.

b.

Answer to Problem 53CE

There is sufficient evidence to conclude that the slope of the regression line is different from zero.

Explanation of Solution

It is given that the regression equation is

The

From the regression equation, the estimated slope of the regression line is

Let

The given test hypotheses are as follows:

Null hypothesis:

That is, the slope of the regression line is equal to zero.

Alternate hypothesis:

That is, the slope of the regression line is not equal to zero.

Assume that the level of significance is 0.05.

Test statistic:

The t-test statistic is as follows:

Where,

Thus, the following is obtained:

Here, the sample size is

Critical value:

Software procedure:

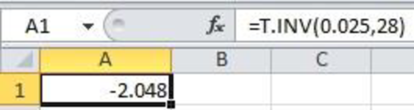

Step-by-step software procedure to obtain the critical value

- Open an EXCEL file.

- In cell A1, enter the formula “=T.INV(0.025,28)”.

Output obtained using the EXCEL is given as follows:

From the EXCEL output, the critical value is –2.048 (

Decision based on the critical value:

Reject the null hypothesis, if

Conclusion:

The t-calculated value is –7.34 and the critical value is –2.048.

That is,

Thus, the null hypothesis is rejected.

Hence, there is sufficient evidence to conclude that the slope of the regression line is different from zero.

c.

Find and interpret the value of coefficient of determination.

c.

Answer to Problem 53CE

The coefficient of determination is 0.658.

Explanation of Solution

From Part (a), the value of coefficient of determination is 0.658.

Therefore, 65.8% of variation in the ‘selling price’ is explained by ‘the annual dividend’.

d.

Find the value of

Test whether the correlation in the population is greater than zero or not.

d.

Answer to Problem 53CE

The correlation coefficient is 0.811.

There is enough evidence to infer that the correlation in the population is greater than zero.

Explanation of Solution

Calculation:

The correlation coefficient is as follows:

The given sample size is 30 and correlation is 0.811.

Denote the population correlation as

The hypotheses are given below:

Null hypothesis:

That is, the correlation in the population is less than or equal to zero.

Alternative hypothesis:

That is, the correlation in the population is greater than zero.

Test statistic:

The test statistic is as follows:

Here, the sample size is 30 and the correlation coefficient is 0.811.

The test statistic is as follows:

Degrees of freedom:

The level of significance is 0.05. Therefore,

Critical value:

Software procedure:

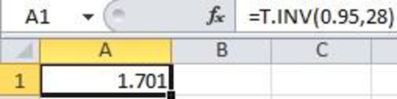

Step-by-step software procedure to obtain the critical value using the EXCEL software:

- Open an EXCEL file.

- In cell A1, enter the formula “=T.INV (0.95, 28)”.

Output obtained using the EXCEL is given as follows:

From the EXCEL output, the critical value is 1.701.

Conclusion:

The value of test statistic is 7.34 and the critical value is 1.701.

Here,

By the rejection rule, reject the null hypothesis.

Thus, there is enough evidence to infer that the correlation in the population is greater than zero.

Want to see more full solutions like this?

Chapter 13 Solutions

Loose Leaf for Statistical Techniques in Business and Economics

- Harvard University California Institute of Technology Massachusetts Institute of Technology Stanford University Princeton University University of Cambridge University of Oxford University of California, Berkeley Imperial College London Yale University University of California, Los Angeles University of Chicago Johns Hopkins University Cornell University ETH Zurich University of Michigan University of Toronto Columbia University University of Pennsylvania Carnegie Mellon University University of Hong Kong University College London University of Washington Duke University Northwestern University University of Tokyo Georgia Institute of Technology Pohang University of Science and Technology University of California, Santa Barbara University of British Columbia University of North Carolina at Chapel Hill University of California, San Diego University of Illinois at Urbana-Champaign National University of Singapore McGill…arrow_forwardName Harvard University California Institute of Technology Massachusetts Institute of Technology Stanford University Princeton University University of Cambridge University of Oxford University of California, Berkeley Imperial College London Yale University University of California, Los Angeles University of Chicago Johns Hopkins University Cornell University ETH Zurich University of Michigan University of Toronto Columbia University University of Pennsylvania Carnegie Mellon University University of Hong Kong University College London University of Washington Duke University Northwestern University University of Tokyo Georgia Institute of Technology Pohang University of Science and Technology University of California, Santa Barbara University of British Columbia University of North Carolina at Chapel Hill University of California, San Diego University of Illinois at Urbana-Champaign National University of Singapore…arrow_forwardA company found that the daily sales revenue of its flagship product follows a normal distribution with a mean of $4500 and a standard deviation of $450. The company defines a "high-sales day" that is, any day with sales exceeding $4800. please provide a step by step on how to get the answers in excel Q: What percentage of days can the company expect to have "high-sales days" or sales greater than $4800? Q: What is the sales revenue threshold for the bottom 10% of days? (please note that 10% refers to the probability/area under bell curve towards the lower tail of bell curve) Provide answers in the yellow cellsarrow_forward

- Find the critical value for a left-tailed test using the F distribution with a 0.025, degrees of freedom in the numerator=12, and degrees of freedom in the denominator = 50. A portion of the table of critical values of the F-distribution is provided. Click the icon to view the partial table of critical values of the F-distribution. What is the critical value? (Round to two decimal places as needed.)arrow_forwardA retail store manager claims that the average daily sales of the store are $1,500. You aim to test whether the actual average daily sales differ significantly from this claimed value. You can provide your answer by inserting a text box and the answer must include: Null hypothesis, Alternative hypothesis, Show answer (output table/summary table), and Conclusion based on the P value. Showing the calculation is a must. If calculation is missing,so please provide a step by step on the answers Numerical answers in the yellow cellsarrow_forwardShow all workarrow_forward

Glencoe Algebra 1, Student Edition, 9780079039897...AlgebraISBN:9780079039897Author:CarterPublisher:McGraw Hill

Glencoe Algebra 1, Student Edition, 9780079039897...AlgebraISBN:9780079039897Author:CarterPublisher:McGraw Hill Big Ideas Math A Bridge To Success Algebra 1: Stu...AlgebraISBN:9781680331141Author:HOUGHTON MIFFLIN HARCOURTPublisher:Houghton Mifflin Harcourt

Big Ideas Math A Bridge To Success Algebra 1: Stu...AlgebraISBN:9781680331141Author:HOUGHTON MIFFLIN HARCOURTPublisher:Houghton Mifflin Harcourt Functions and Change: A Modeling Approach to Coll...AlgebraISBN:9781337111348Author:Bruce Crauder, Benny Evans, Alan NoellPublisher:Cengage Learning

Functions and Change: A Modeling Approach to Coll...AlgebraISBN:9781337111348Author:Bruce Crauder, Benny Evans, Alan NoellPublisher:Cengage Learning Holt Mcdougal Larson Pre-algebra: Student Edition...AlgebraISBN:9780547587776Author:HOLT MCDOUGALPublisher:HOLT MCDOUGAL

Holt Mcdougal Larson Pre-algebra: Student Edition...AlgebraISBN:9780547587776Author:HOLT MCDOUGALPublisher:HOLT MCDOUGAL