INTERMEDIATE ACCOUNTING(LL)-W/CONNECT

9th Edition

ISBN: 9781260216141

Author: SPICELAND

Publisher: MCG CUSTOM

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 12, Problem 12.18E

Equity investments; fair value through net income

• LO12-4

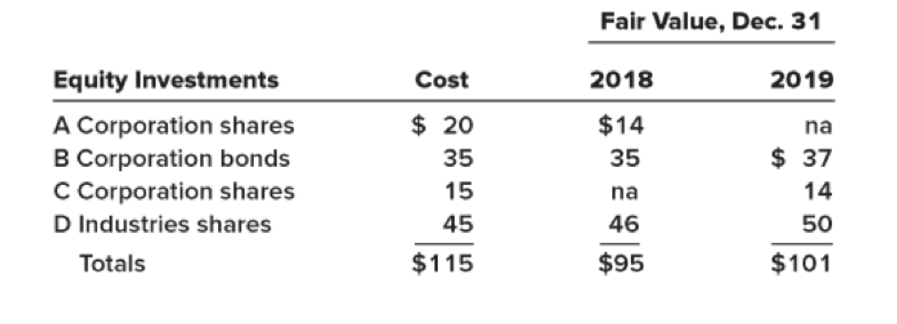

The investments of Harlon Enterprises included the following cost and fair value amounts ($ in millions):

Harlon accounts for its equity investment portfolio at fair value through net income. Harlon sold its holdings of A Corporation shares on June 1, 2019, for $15 million. On September 12, it purchased the C Corporation shares.

Required:

1. What is the effect of the sale of the A Corporation shares and the purchase of the C Corporation shares on Harlon’s 2019 pretax earnings?

2. At what amount should Harlon’s securities equity investment portfolio be reported in its 2019

Expert Solution & Answer

Trending nowThis is a popular solution!

Students have asked these similar questions

Please give me correct answer this financial accounting question

Need answer the financial accounting question not use ai and chatgpt

Compute the spending variance for materials

Chapter 12 Solutions

INTERMEDIATE ACCOUNTING(LL)-W/CONNECT

Ch. 12 - All investments in debt securities are classified...Ch. 12 - When market rates of interest rise after a...Ch. 12 - Does GAAP distinguish between fair values that are...Ch. 12 - When a debt investment is acquired to be held for...Ch. 12 - Prob. 12.5QCh. 12 - What is comprehensive income? Its composition...Ch. 12 - Why are holding gains and losses treated...Ch. 12 - Prob. 12.8QCh. 12 - Prob. 12.9QCh. 12 - Prob. 12.10Q

Ch. 12 - Under IFRS No. 9, which reporting categories are...Ch. 12 - Prob. 12.12QCh. 12 - Do U.S. GAAP and IFRS differ in the amount of...Ch. 12 - Under what circumstances is the equity method used...Ch. 12 - The equity method has been referred to as a...Ch. 12 - In the application of the equity method, how...Ch. 12 - Prob. 12.17QCh. 12 - Prob. 12.18QCh. 12 - Prob. 12.19QCh. 12 - How does IFRS differ from U.S. GAAP with respect...Ch. 12 - What is the effect of a company electing the fair...Ch. 12 - Define a financial instrument. Provide three...Ch. 12 - Some financial instruments are called derivatives....Ch. 12 - (Based on Appendix 12A) Northwest Carburetor...Ch. 12 - Prob. 12.25QCh. 12 - Prob. 12.26QCh. 12 - (Based on Appendix 12B) Reporting an investment at...Ch. 12 - Prob. 12.28QCh. 12 - Explain how the CECL model (introduced in ASU No....Ch. 12 - Prob. 12.30QCh. 12 - Prob. 12.1BECh. 12 - Prob. 12.2BECh. 12 - Trading securities LO12-3 For the Coca-Cola bonds...Ch. 12 - Available -for-sale securities LO12-4 SL...Ch. 12 - Available -for-sale securities LO12-4 For the...Ch. 12 - Prob. 12.6BECh. 12 - Prob. 12.7BECh. 12 - Prob. 12.8BECh. 12 - Prob. 12.9BECh. 12 - Prob. 12.10BECh. 12 - Equity investments and dividends LO12-5 Turner...Ch. 12 - Prob. 12.12BECh. 12 - Prob. 12.13BECh. 12 - Equity method investments LO12-6, LO12-9 Kim...Ch. 12 - Change in principle; change to the equity method ...Ch. 12 - Fair value option; equity method investments ...Ch. 12 - Prob. 12.17BECh. 12 - Impairments (AFS Credit Loss Model) (Appendix 12B)...Ch. 12 - Prob. 12.19BECh. 12 - Prob. 12.20BECh. 12 - Prob. 12.1ECh. 12 - Prob. 12.2ECh. 12 - Securities held-to-maturity LO12-1 FFT...Ch. 12 - Prob. 12.4ECh. 12 - Prob. 12.5ECh. 12 - Trading securities LO12-1 [This is a variation of...Ch. 12 - Various transactions relating to trading...Ch. 12 - Prob. 12.8ECh. 12 - Securities available-for-sale; adjusting entries ...Ch. 12 - Available -for-sale securities LO12-1, LO12-4...Ch. 12 - Available -for-sale securities LO12-1, LO12-4...Ch. 12 - Available -for-sale securities LO12-1, LO12-4...Ch. 12 - Classification of securities; adjusting entries ...Ch. 12 - Prob. 12.14ECh. 12 - Equity investments; fair value through net income ...Ch. 12 - Equity investments; fair value through net income ...Ch. 12 - Prob. 12.17ECh. 12 - Equity investments; fair value through net income ...Ch. 12 - Investment securities and equity method...Ch. 12 - Equity method; purchase; investee income;...Ch. 12 - Error corrections; equity method investment ...Ch. 12 - Prob. 12.22ECh. 12 - Prob. 12.23ECh. 12 - Prob. 12.24ECh. 12 - Prob. 12.25ECh. 12 - Prob. 12.26ECh. 12 - Prob. 12.27ECh. 12 - Prob. 12.28ECh. 12 - Prob. 12.29ECh. 12 - Prob. 12.30ECh. 12 - Prob. 12.31ECh. 12 - Prob. 12.32ECh. 12 - Accounting for impairments under IFRS (Appendix...Ch. 12 - Prob. 12.1PCh. 12 - Prob. 12.2PCh. 12 - Securities available-for-sale; bond investment;...Ch. 12 - Prob. 12.4PCh. 12 - Various transactions related to trading securities...Ch. 12 - Various transactions related to securities...Ch. 12 - Prob. 12.7PCh. 12 - Various transactions relating to trading...Ch. 12 - Securities held-to-maturity; securities available...Ch. 12 - Investment securities and equity method...Ch. 12 - Prob. 12.11PCh. 12 - Prob. 12.12PCh. 12 - Prob. 12.13PCh. 12 - Equity method LO12-6, LO12-7 On January 2, 2018,...Ch. 12 - Prob. 12.15PCh. 12 - Prob. 12.16PCh. 12 - Accounting for debt and equity investments ...Ch. 12 - Prob. 12.18PCh. 12 - Real World Case 121 Intels investments LO12-4 The...Ch. 12 - Prob. 12.2BYPCh. 12 - Prob. 12.4BYPCh. 12 - Prob. 12.6BYPCh. 12 - Real World Case 127 Comprehensive income Microsoft...Ch. 12 - Continuing Cases Target Case LO12-4, LO12-6...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial Accounting

Accounting

ISBN:9781337690881

Author:Jay Rich, Jeff Jones

Publisher:Cengage Learning

Operating Loss Carryback and Carryforward; Author: SuperfastCPA;https://www.youtube.com/watch?v=XiYhgzSGDAk;License: Standard Youtube License