Concept explainers

Videos

Dollar-value LIFO retail

• LO9–5

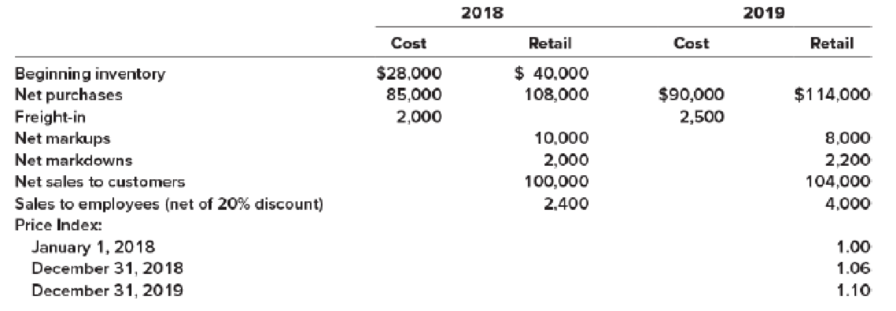

On January 1, 2018, HGC Camera Store adopted the dollar-value LIFO retail inventory method. Inventory transactions at both cost and retail, and cost indexes for 2018 and 2019 are as follows:

Required:

Estimate the 2018 and 2019 ending inventory and cost of goods sold using the dollar-value LIFO retail inventory method.

Dollar-Value-LIFO

This method shows all the inventory figures at dollar price rather than units. Under this inventory method, the units that are purchased last, are sold first. Thus, it starts from the selling of the units recently purchased and ending with the beginning inventory.

To Estimate: the ending inventory and cost of goods sold in 2018 using dollar-value LIFO retail method.

Explanation of Solution

Solution:

Calculate the amount of estimated ending inventory and cost of goods sold at retail.

| Details | Cost ($) | Retail ($) |

| Beginning inventory | 28,000 | 40,000 |

| Add: Net purchase | 85,000 | 108,000 |

| Freight-in | 2,000 | |

| Net markups | 10,000 | |

| Less: Net markdowns | (2,000) | |

| Goods available for sale – Excluding beginning inventory | 87,000 | 116,000 |

| Goods available for sale – Including beginning inventory | 115,000 | 156,000 |

| Less: Net sales | 0 | (102,400) |

| Employees discounts | (600) | |

| Estimated ending inventory at current year retail prices | 53,000 | |

| Estimated ending inventory at cost (Refer Table 2) | (35,950) | |

| Estimated Cost of Goods Sold | 79,050 |

Table (1)

Working Notes:

Calculate base layer cost-to retail percentage.

Calculate current year cost-to retail percentage.

Calculate the amount of estimated ending inventory at cost.

| Ending inventory at dollar-value LIFO retail cost | ||||

| Ending inventory at year-end retail prices ($) | Ending inventory at base year retail prices ($) | Inventory layers at base year retail prices ($) | Inventory layers converted to cost ($) | |

| 53,000 | 50,000 | 40,000 (Base) | 28,000 | |

| 10,000 (2018) | 7,950 | |||

| Total ending inventory at dollar-value LIFO retail cost | 35,950 | |||

Table (2)

Calculate the amount of ending inventory at base year retail prices.

Calculate the amount of inventory layers at base year retail prices.

Calculate the amount of inventory layers at current year retail prices.

Calculate the amount of inventory layers converted to cost (Base).

Calculate the amount of inventory layers converted to cost (2018).

Calculate the amount of estimated ending inventory and cost of goods sold at retail.

| Details | Cost ($) | Retail ($) |

| Beginning inventory | 35,950 | 53,000 |

| Add: Net purchase | 90,000 | 114,000 |

| Freight-in | 2,500 | |

| Net markups | 8,000 | |

| Less: Net markdowns | (2,200) | |

| Goods available for sale – Excluding beginning inventory | 92,500 | 119,800 |

| Goods available for sale – Including beginning inventory | 128,450 | 172,800 |

| Less: Net sales | 0 | (108,000) |

| Employees discounts | (1,000) | |

| Estimated ending inventory at current year retail prices | 63,800 | |

| Estimated ending inventory at cost (Refer Table 2) | (42,744) | |

| Estimated Cost of Goods Sold | 85,706 |

Table (3)

Working Notes:

Calculate base layer cost-to retail percentage.

Calculate 2018 year cost-to retail percentage.

Calculate current year cost-to retail percentage.

Calculate the amount of estimated ending inventory at cost.

| Ending inventory at dollar-value LIFO retail cost | ||||

| Ending inventory at year-end retail prices ($) | Ending inventory at base year retail prices ($) | Inventory layers at base year retail prices ($) | Inventory layers converted to cost ($) | |

| 63,800 | 58,000 | 40,000 (Base) | 28,000 | |

| 10,000 (2018) | 7,950 | |||

| 8,000 (2019) | 6,794 | |||

| Total ending inventory at dollar-value LIFO retail cost | 42,744 | |||

Table (4)

Calculate the amount of ending inventory at base year retail prices.

Calculate the amount of inventory layers at base year retail prices.

Calculate the amount of inventory layers at current year retail prices.

Calculate the amount of inventory layers converted to cost (Base).

Calculate the amount of inventory layers converted to cost (2018).

Calculate the amount of inventory layers converted to cost (2019).

Want to see more full solutions like this?

Chapter 9 Solutions

INTERMEDIATE ACCOUNTING (LL) W/CONNECT

- Which of the following errors will cause the trial balance to not balance?A. Omission of a transactionB. Entry posted twiceC. Transposing digits in one sideD. Debiting one account and crediting anotherarrow_forwardMime Delivery Service is owned and operated by Pamela Kolp. The following selected transactionswere completed by Mime Delivery Service during October:1. Received cash from the owner as an additional investment, $7,500.2. Paid creditors on account, $815.3. Billed customers for delivery services on account, $3,250.4. Received cash from customers on account, $1,150.5. Paid cash to the owner for personal use, $500.Required:Indicate the effect of each transaction on the accounting equation elements (Assets, Liabilities,Owner’s Equity, Drawing, Revenue, and Expense) by listing the numbers identifying the transactions,(1) to (5). Also, indicate the specific item within the accounting equation element that is affected, i.e.(1) Asset (Cash) increases by $; Owner’s Equity (Pamela Kolp, Capital) increases by $.arrow_forwardWhen a company incurs an expense but does not yet pay it, what is the entry?A. Debit Expense, Credit CashB. Debit Liability, Credit ExpenseC. Debit Expense, Credit LiabilityD. No entry needed helparrow_forward

- When a company incurs an expense but does not yet pay it, what is the entry?A. Debit Expense, Credit CashB. Debit Liability, Credit ExpenseC. Debit Expense, Credit LiabilityD. No entry neededarrow_forwardDont use ai What is the effect of writing off an uncollectible account under the allowance method?A. Increases net incomeB. No effect on total assetsC. Decreases revenueD. Increases expensesarrow_forwardWhat is the effect of writing off an uncollectible account under the allowance method?A. Increases net incomeB. No effect on total assetsC. Decreases revenueD. Increases expensesi need help ..arrow_forward

- Get the Correct Answer with calculation of this General Accounting Questionarrow_forwardI am trying to find the accurate solution to this general accounting problem with appropriate explanations.arrow_forwardI need help with this general accounting problem using proper accounting guidelines.arrow_forward

- I am looking for the correct answer to this general accounting problem using valid accounting standards.arrow_forwardHello Dear Tutor Please Need Answer of this Question as possible fast and Correctarrow_forward15. The balance in the dividends account is closed to:A. CashB. RevenueC. Retained EarningsD. Common Stock dont use AIarrow_forward

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College Accounting Information SystemsFinanceISBN:9781337552127Author:Ulric J. Gelinas, Richard B. Dull, Patrick Wheeler, Mary Callahan HillPublisher:Cengage Learning

Accounting Information SystemsFinanceISBN:9781337552127Author:Ulric J. Gelinas, Richard B. Dull, Patrick Wheeler, Mary Callahan HillPublisher:Cengage Learning