Subpart (a):

The equilibrium price and the quantity of haircuts and total surplus.

Subpart (a):

Explanation of Solution

Supply curve: The supply equation is

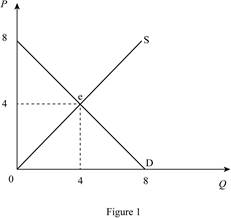

In Figure 1, horizontal axis measures quantity and vertical axis measures price. The curve D indicates demand and the curve S indicates supply. Market reaches the equilibrium at point ‘e’ where the demand curve intersects with supply curve.

Equilibrium price can be calculated as follows.

Equilibrium price is $4.

Thus, equilibrium quantity is 4 units.

Consumer surplus is $8.

Producer surplus is $8.

Total surplus can be calculated as follows.

Total surplus is $16.

Concept introduction:

Consumer surplus: It is the difference between the highest willing price of the consumer and the actual price that the consumer pays.

Producer surplus: It is the difference between the minimum accepted price for the producer and the actual price received by the producer.

Equilibrium price: It is the market price determined by equating the supply to the demand. At this equilibrium point, the supply will be equal to the demand and there will be no excess demand or

Subpart (b):

The equilibrium price and the quantity of haircuts and total surplus.

Subpart (b):

Explanation of Solution

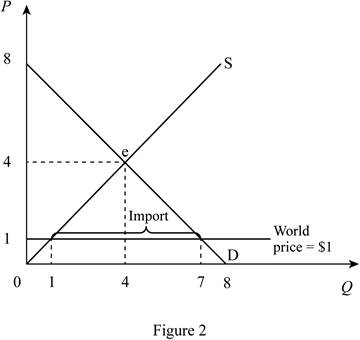

The world price for the good is $1. Thus, when the country opens the market for trade, the price becomes $1 in domestic country too. Figure 2 describe this situation.

In Figure 2, horizontal axis measures quantity and vertical axis measures price. The curve D indicates demand and the curve S indicates supply. Market reaches the equilibrium at point ‘e’ where the demand curve intersects with supply curve.

When the competitor (Rest of the world) sells a good at price $1, in domestic country equilibrium price become equal to world price. Thus, equilibrium price in the domestic country is $1.

Equilibrium domestic supply can be calculated by substituting the domestic equilibrium price in to supply equation.

Thus, equilibrium quantity is 1 unit.

Equilibrium domestic demand can be calculated by substituting the domestic equilibrium price in to demand equation.

Thus, equilibrium domestic demand is 7 units.

Total imports can be calculated as follows.

Domestic imports are 6 units.

Consumer surplus can be calculated as follows.

Consumer surplus is $24.5.

Producer surplus can be calculated as follows.

Producer surplus is $0.5.

Total surplus can be calculated as follows.

Total surplus is $25.

Concept introduction:

Consumer surplus: It is the difference between the highest willing price of the consumer and the actual price that the consumer pays.

Producer surplus: It is the difference between the minimum accepted price for the producer and the actual price received by the producer.

Equilibrium price: It is the market price determined by equating the supply to the demand. At this equilibrium point, the supply will be equal to the demand and there will be no excess demand or excess supply in an economy. Thus, the economy will be at equilibrium.

Subpar (c):

The equilibrium price and the quantity of haircuts and total surplus.

Subpar (c):

Explanation of Solution

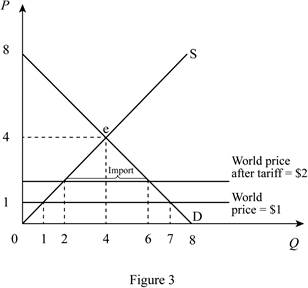

When domestic country impose tariff of $1, the price in domestic country increases from $1 to $2. This increase in price is shown in the Figure 3.

In Figure 3, horizontal axis measures quantity and vertical axis measures price. The curve D indicates demand and the curve S indicates supply. Market reaches the equilibrium at point ‘e’ where the demand curve intersects with supply curve. Price is increases from $1 to $2 due to the tariff of $1.

Domestic equilibrium price can be calculated as follows.

New domestic price is $2.

Equilibrium domestic supply can be calculated by substituting the domestic equilibrium price in to supply equation.

Thus, equilibrium quantity is 2 units.

Equilibrium domestic demand can be calculated by substituting the domestic equilibrium price in to demand equation.

Thus, equilibrium domestic demand is 6 units.

Total imports can be calculated as follows.

Domestic imports are 4 units.

Consumer surplus can be calculated as follows.

Consumer surplus is $18.

Producer surplus can be calculated as follows.

Producer surplus is $2.

Government revenue can be calculated as follows.

Government revenue is 4.

Total surplus can be calculated as follows.

Total surplus is $24.

Concept introduction:

Consumer surplus: It is the difference between the highest willing price of the consumer and the actual price that the consumer pays.

Producer surplus: It is the difference between the minimum accepted price for the producer and the actual price received by the producer.

Equilibrium price: It is the market price determined by equating the supply to the demand. At this equilibrium point, the supply will be equal to the demand and there will be no excess demand or excess supply in an economy. Thus, the economy will be at equilibrium.

Subpart (d):

Calculate total gains and deadweight loss.

Subpart (d):

Explanation of Solution

Total gains from opening up trade can be calculated as follows.

Total gains are$8.

Deadweight loss can be calculated as follows.

Deadweight loss is $1.

Want to see more full solutions like this?

Chapter 9 Solutions

Bundle: Principles of Microeconomics, Loose-Leaf Version, 7th + Principles of Macroeconomics, Loose-Leaf Version, 7th + MindTap Economics, 2 terms (12 ... for Mankiw’s Principles of Economics, 7th

- Not use aiarrow_forwardProblem 3 Stata Output Analysis Suppose a study investigates the causal effect of education on wages. Table 1 reports the results of an OLS regression of wages (wage per hour in dollars) on education (years in education). Table 1 Source SS df MS Number of obs = 3,017 F(1, 3015) = 298.39 Model Residual 18904467 191011981 1 18904467 3,015 63353.8909 Prob > F 0.0000 R-squared 0.0901 Adj R-squared 0.0898 Total 209916448 3,016 69600.9444 Root MSE 251.7 wage Coef. Std. Err. t P>|t| [95% Conf. Interval] education cons 29.56644 183.9342 1.711605 23.15976 17.27 0.000 7.94 0.000 26.21041 138.5237 32.92247 229.3447 a. How would you write this relationship using the Core Model? (5 points) b. What is the value for B₁, the coefficient on Education? (2 points) C. What is the standard error of ẞ₁? (2 points) d. What is the R squared for the model? (2 points) e. What is the t statistic for ₁at the 5% level of significance? (2 points) Λ f. What is the 95% confidence interval for B₁? (2 points) Λ g.…arrow_forwardProblem 2 Hypothesis Testing Suppose you are interested in the effect of neighborhood crime incidents on high school graduation rates. You run the following regression model: Graduation; ßo+ß₁Crime; +ɛ¿ = You would like to test whether the neighborhood crime incidents have a statistically significant effect on high school graduation rate at the 5% level of significance (α = 0.05). You estimate the model and find that B₁ = -0.04 and se (B₁) = 0.008. a. Write down the null hypothesis and alternative hypothesis. (4 points) b. Calculate thet statistic of B₁. (5 points) C. What is the critical value of thet statistic for the 5% level of significance? (2 points) d. Calculate the 95% confidence interval for the coefficient on Crime? (6 points) e. Based on your answers to the questions b, c, and d, do you reject or fail to reject the null hypothesis you defined in question a? Justify your answer. (5 points) Λ f. Isẞ₁ statistically significant at the 5% level? (3 points)arrow_forward

- Problem 1 Endogeneity & Bias The ACT (an abbreviation of American College Testing) is a standardized test used for college admissions in the United States. Suppose you are interested in whether ACT preparation improves ACT scores. Consider the following model: ACT=B+B Preparation,+e; where Preparation measures the number of hours spent on ACT preparation and ACT is ACT scores. Each student is denoted by the subscript i. Suppose you estimate = - 21 andß₁ = 0.9. a. What is the dependent variable? What is the independent variable? (3 points) b. How do you interpret ẞ = 21 in this context? (4 points) 0 C. How do you interpretß₁ = 0.9 in this context? (4 points) 1 d. Describe a scenario which can cause the independent variable to be endogenous. (4 points)arrow_forwardHow does mining raw materials fir tech companies like apple affect the humar right violation all over the worldarrow_forwardConsider the market for electricity. Suppose that a power plant dumps byproducts into a nearby river, creating a negative externality for those living downstream from the plant. Producing additional electricity imposes a constant per-unit external cost of $490. The following graph shows the demand (private value) curve and the supply (private cost) curve for electricity. Use the purple points (diamond symbol) to plot the social cost curve when the external cost is $490 per unit. PRICE (Dollars per unit of electricity) 1400 1260 1120 980 840 700 560 420 280 140 ° D 1 2 3 D Supply (Private Cost) Demand (Private Value) 5 6 7 QUANTITY (Units of electricity) Social Cost The market equilibrium quantity is units of electricity, but the socially optimal quantity of electricity production is units. To create an incentive for the firm to produce the socially optimal quantity of electricity, the government could impose a unit of electricity. perarrow_forward

- How do mining of raw materials for a tech industry affects the human rights in the worldarrow_forwardAssume the Federal Interstate Commission began the fiscal year with the following account balances: FEDERAL INTERSTATE COMMISSION Trial BalanceOctober 1, 2020 Debits Credits Fund Balance with Treasury$810,000 Supplies 107,000 Equipment 1, 370,000 Accumulated Depreciation $484,000 Accounts Payable 130,000 Wages Payable 85,000Cumulative Results of Operations 1,588,000 $2,287,000 $2,287,000 Congress passed a spending bill providing $17,200, 000 to fund the agency's operations for the year. During the first quarter the commission processed the following items for payment (all items were paid by Treasury in the first quarter). Accounts payable$130,000 Wages payable 85,000 Salaries and benefits 507,000 Supplies 524,000 Contracted services 2,200,000 Grants 1,020,000 Equipment 620,000 Total$5,086,000 Unpaid wages at the end of the quarter totaled $37,000. In addition to the items paid in item 2, the commission received supplies of $24,000 and contracted services of $82,000 that are to be…arrow_forwardnot use aiarrow_forward

Principles of MicroeconomicsEconomicsISBN:9781305156050Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of MicroeconomicsEconomicsISBN:9781305156050Author:N. Gregory MankiwPublisher:Cengage Learning Principles of Economics, 7th Edition (MindTap Cou...EconomicsISBN:9781285165875Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics, 7th Edition (MindTap Cou...EconomicsISBN:9781285165875Author:N. Gregory MankiwPublisher:Cengage Learning Principles of Macroeconomics (MindTap Course List)EconomicsISBN:9781285165912Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Macroeconomics (MindTap Course List)EconomicsISBN:9781285165912Author:N. Gregory MankiwPublisher:Cengage Learning Microeconomics: Private and Public Choice (MindTa...EconomicsISBN:9781305506893Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning

Microeconomics: Private and Public Choice (MindTa...EconomicsISBN:9781305506893Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning Macroeconomics: Private and Public Choice (MindTa...EconomicsISBN:9781305506756Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning

Macroeconomics: Private and Public Choice (MindTa...EconomicsISBN:9781305506756Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning Economics: Private and Public Choice (MindTap Cou...EconomicsISBN:9781305506725Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning

Economics: Private and Public Choice (MindTap Cou...EconomicsISBN:9781305506725Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning