INTERM.ACCT.:REPORTING...-CENGAGENOWV2

3rd Edition

ISBN: 9781337909358

Author: WAHLEN

Publisher: CENGAGE L

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 8, Problem 7RE

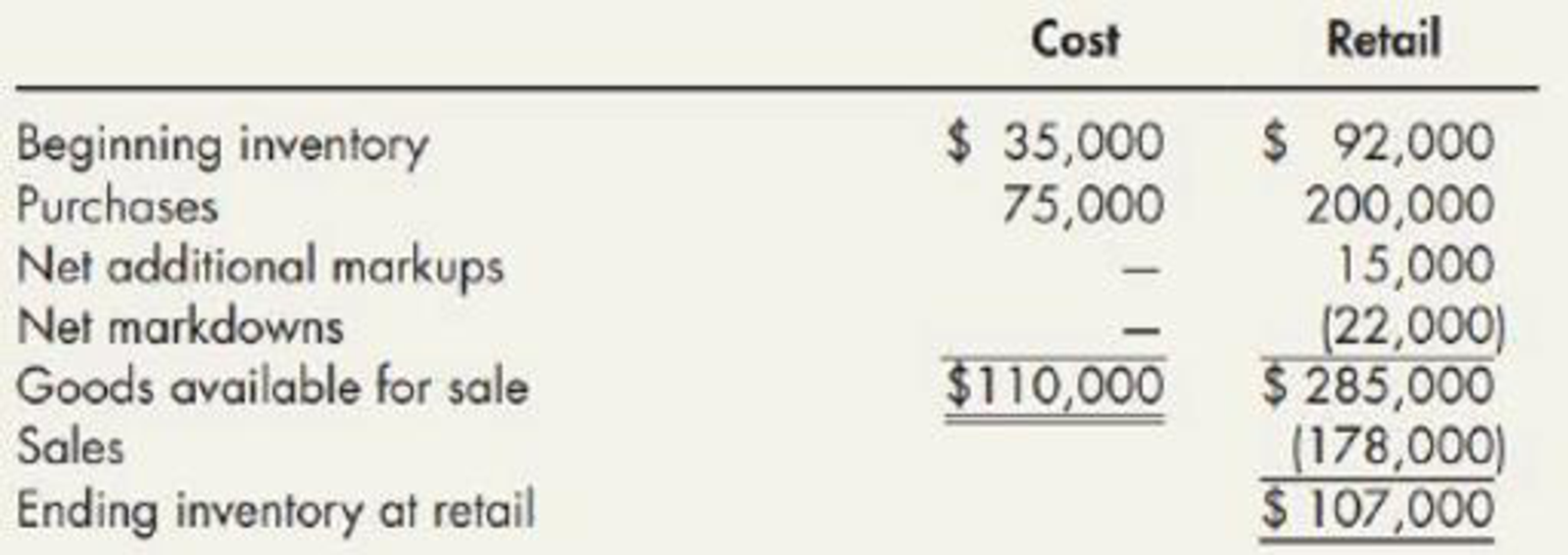

Uncle Butch’s Hunting Supply Shop reports the following information related to inventory:

Calculate Uncle Butch’s’ ending inventory using the retail inventory method under the FIFO cost flow assumption. Round the cost-to-retail ratio to 3 decimal places.

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

Recently, Abercrombie & Fitch has been implementing a turnaround strategy since its sales had been falling for the past few years (11% decrease in 2014, 8% in 2015, and just 3% in 2016.) One part of Abercrombie's new strategy has been to abandon its logo-adorned merchandise, replacing it with a subtler look. Abercrombie wrote down $20.6 million of inventory, including logo-adorned merchandise, during the year ending January 30, 2016. Some of this inventory dated back to late 2013. The write-down was net of the amount it would be able to recover selling the inventory at a discount. The write-down is significant; Abercrombie's reported net income after this write-down was $35.6 million. Interestingly, Abercrombie excluded the inventory write-down from its non-GAAP income measures presented to investors; GAAP earnings were also included in the same report. Question: What impact would the write-down of inventory have had on Abercrombie's assets, Liabilities, and Equity?

Need answer general Accounting

Provide correct answer of this question answer general Accounting

Chapter 8 Solutions

INTERM.ACCT.:REPORTING...-CENGAGENOWV2

Ch. 8 - Under what circumstances will a company value...Ch. 8 - What is the conceptual justification for reducing...Ch. 8 - Define the terms cost, net realizable value, and...Ch. 8 - For companies that use either LIFO or the retail...Ch. 8 - What three implementation approaches may a company...Ch. 8 - Describe the two approaches to recording the...Ch. 8 - Prob. 7GICh. 8 - In applying the inventory valuation rules to...Ch. 8 - Prob. 9GICh. 8 - What are the exceptions to historical cost...

Ch. 8 - Prob. 11GICh. 8 - Prob. 12GICh. 8 - What is the basic assumption underlying the gross...Ch. 8 - Prob. 14GICh. 8 - Prob. 15GICh. 8 - Explain the meaning of the following terms:...Ch. 8 - Prob. 17GICh. 8 - Prob. 18GICh. 8 - The retail inventory method indicated an inventory...Ch. 8 - Prob. 20GICh. 8 - Indicate the effect of each of the following...Ch. 8 - Sienna Company uses the FIFO cost flow assumption....Ch. 8 - Moore Company uses the LIFO cost flow assumption...Ch. 8 - A company uses the LIFO cost flow assumption. The...Ch. 8 - Prob. 4MCCh. 8 - Hestor Companys records indicate the following...Ch. 8 - Under the retail inventory method, freight-in...Ch. 8 - The retail inventory method would include which of...Ch. 8 - At December 31, 2019, the following information...Ch. 8 - Estimates of price-level changes for specific...Ch. 8 - A company forgets to record a purchase on credit...Ch. 8 - Brown Company has the following information...Ch. 8 - Black Corporation uses the LIFO cost flow...Ch. 8 - Blue Corporation uses the FIFO cost flow...Ch. 8 - Paul Corporation uses FIFO and reports the...Ch. 8 - Using the information provided in RE8-4, prepare...Ch. 8 - Kays Beauty Supply uses the gross profit method to...Ch. 8 - Uncle Butchs Hunting Supply Shop reports the...Ch. 8 - Use the information in RE8-7. Calculate Uncle...Ch. 8 - Use the information in RE8-7. Calculate Uncle...Ch. 8 - Use the information in RE8-7. Calculate Uncle...Ch. 8 - Johnson Corporation had beginning inventory of...Ch. 8 - Borys Companys periodic inventory at December 31,...Ch. 8 - Refer to the information provided in RE8-4. If...Ch. 8 - Refer to the information provided in RE8-4. If...Ch. 8 - Inventory Write-Down Stiles Corporation uses the...Ch. 8 - Inventory Write-Down Stiles Corporation uses the...Ch. 8 - Inventory Write-Down Byron Company has five...Ch. 8 - Inventory Write-Down The following information for...Ch. 8 - Inventory Write-Down The following information is...Ch. 8 - Inventory Write-Down The inventories of Berry...Ch. 8 - Prob. 7ECh. 8 - Gross Profit Method: Estimation of Flood Loss On...Ch. 8 - Prob. 9ECh. 8 - Gross Profit Method: Estimation of Theft Loss You...Ch. 8 - Retail Inventory Method Harmes Company is a...Ch. 8 - Retail Inventory Method The following data were...Ch. 8 - Retail Inventory Method The following information...Ch. 8 - Dollar-Value LIFO Retail Johns Company adopts the...Ch. 8 - Dollar-Value LIFO Retail Wyatt Company adopts the...Ch. 8 - Dollar-Value LIFO Retail On December 31, 2018,...Ch. 8 - Errors A company that uses the periodic inventory...Ch. 8 - Errors During the course of your examination of...Ch. 8 - (Appendix 8.1) Inventory Write-Down The...Ch. 8 - Inventory Write-Down Palmquist Company has five...Ch. 8 - Inventory Write-Down The following are the...Ch. 8 - Inventory Write-Down The inventory records of...Ch. 8 - Gross Profit Method: Estimation of Fire Loss On...Ch. 8 - Gross Profit Method: Estimation of Flood Loss On...Ch. 8 - Retail Inventory Method Turner Corporation uses...Ch. 8 - Retail Inventory Method EKC Company uses the...Ch. 8 - Retail Inventory Method Red Department Store uses...Ch. 8 - Retail Inventory Method Weber Corporation uses the...Ch. 8 - Dollar-Value LIFO Retail The following information...Ch. 8 - Dollar-Value LIFO Retail Intella Inc. adopted the...Ch. 8 - Prob. 12PCh. 8 - Errors As controller of Lerner Company, which uses...Ch. 8 - Comprehensive: Inventory Adjustments Layne...Ch. 8 - (Appendix 8.1) Inventory Write-Down The following...Ch. 8 - (Appendix 8.1) Inventory Write-Down Frost Companys...Ch. 8 - Prob. 1CCh. 8 - Sandberg Paint Company, your client, manufactures...Ch. 8 - Prob. 3CCh. 8 - Inventory Valuation Issues Hanlon Company...Ch. 8 - Gross Profit Shelly Corporation is an importer and...Ch. 8 - Prob. 6CCh. 8 - Prob. 7CCh. 8 - Various Inventory Issues Hudson Company, which is...Ch. 8 - Analyzing Starbucks Inventory Disclosures Obtain...Ch. 8 - Analyzing Moet Hennessy Louis Vuittons (LVMH)...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:Cengage Learning

Cornerstones of Financial Accounting

Accounting

ISBN:9781337690881

Author:Jay Rich, Jeff Jones

Publisher:Cengage Learning

Principles of Accounting Volume 1

Accounting

ISBN:9781947172685

Author:OpenStax

Publisher:OpenStax College

Financial Accounting

Accounting

ISBN:9781337272124

Author:Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:Cengage Learning

College Accounting, Chapters 1-27

Accounting

ISBN:9781337794756

Author:HEINTZ, James A.

Publisher:Cengage Learning,

Financial Accounting

Accounting

ISBN:9781305088436

Author:Carl Warren, Jim Reeve, Jonathan Duchac

Publisher:Cengage Learning

Chapter 6 Merchandise Inventory; Author: Vicki Stewart;https://www.youtube.com/watch?v=DnrcQLD2yKU;License: Standard YouTube License, CC-BY

Accounting for Merchandising Operations Recording Purchases of Merchandise; Author: Socrat Ghadban;https://www.youtube.com/watch?v=iQp5UoYpG20;License: Standard Youtube License