Concept explainers

Videos

Recording Daily and

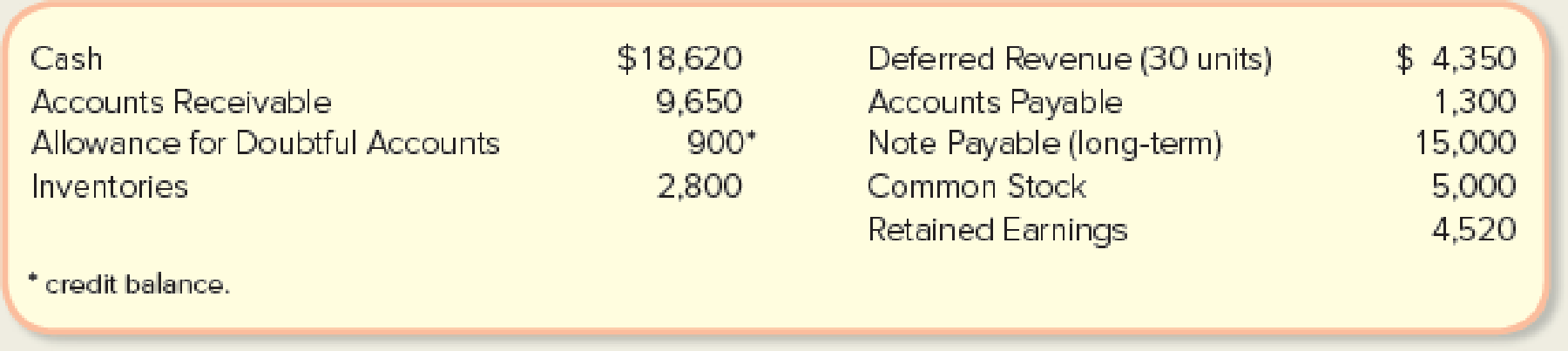

One Trick Pony (OTP) incorporated and began operations near the end of the year, resulting in the following post-closing balances at December 31:

The following information is relevant to the first month of operations in the following year:

- • OTP will sell inventory at $145 per unit. OTP’s January 1 inventory balance consists of 35 units at a total cost of $2,800. OTP’s policy is to use the FIFO method, recorded using a perpetual inventory system.

- • In December, OTP received a $4,350 payment for 30 units OTP is to deliver in January; this obligation was recorded in Deferred Revenue. Rent of $1,300 was unpaid and recorded in Accounts Payable at December 31.

- • OTP’s note payable matures in three years, and accrues interest at a 10% annual rate.

January Transactions

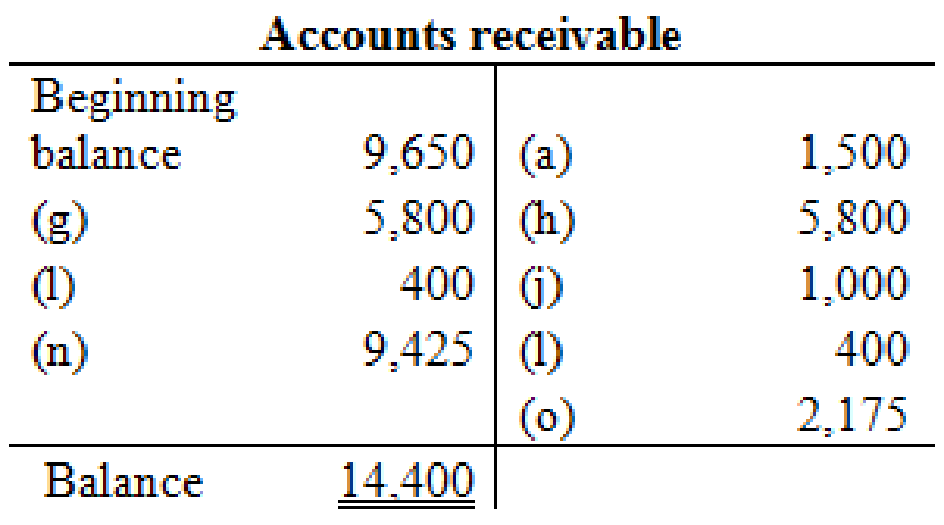

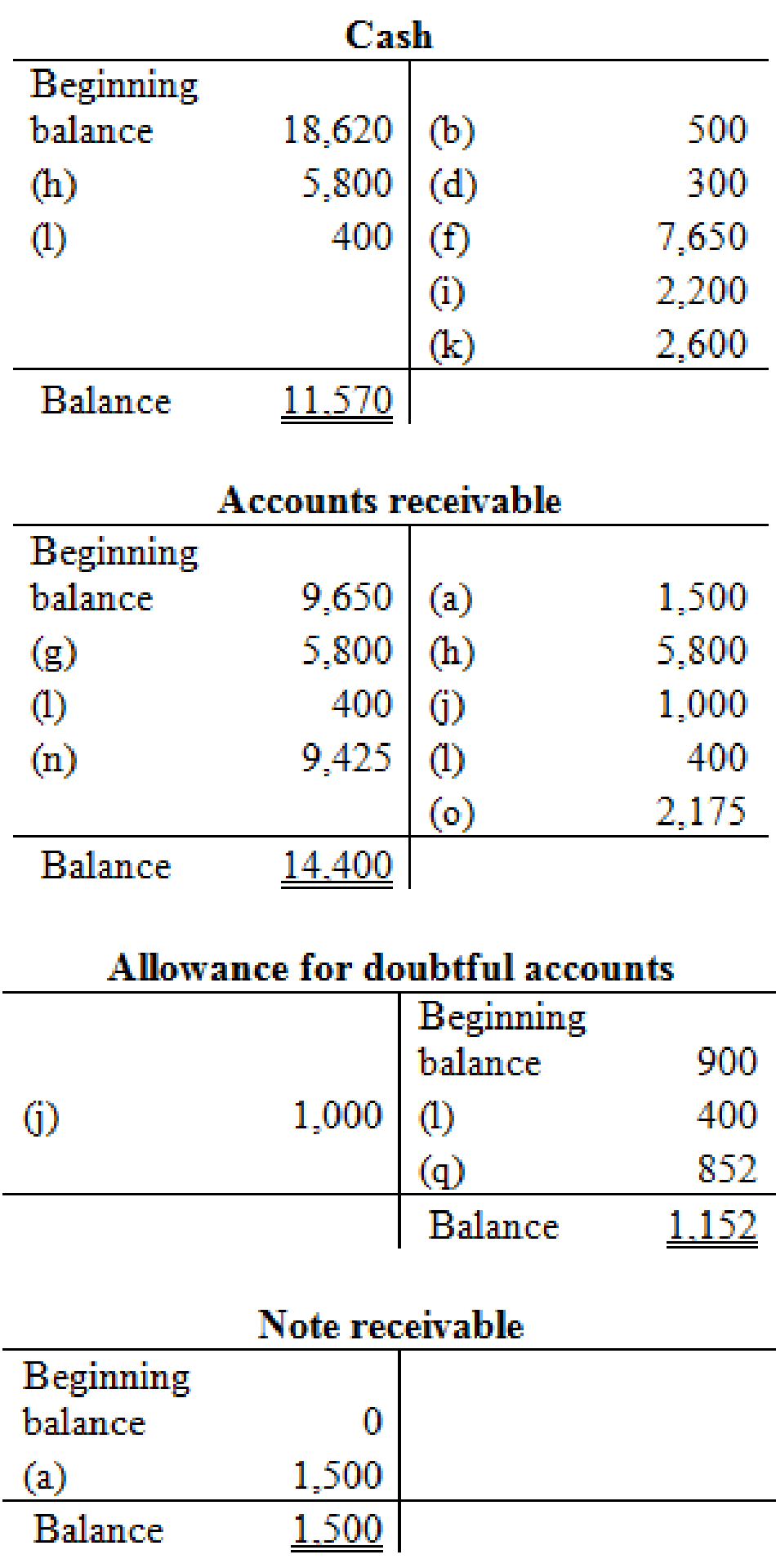

- a. Included in OTP’s January 1

Accounts Receivable balance is a $1,500 balance due from Jeff Letrotski. Jeff is havingcash flow problems and cannot pay the $1,500 balance at this time. On 01/01, OTP arranges with Jeff to convert the $1,500 balance to a six-month note, at 12% annual interest. Jeff signs the promissory note, which indicates the principal and all interest will be due and payable to OTP on July 1 of this year. - b. OTP paid a $500 insurance premium on 01/02, covering the month of January; the payment is recorded directly as an expense.

- c. OTP purchased an additional 150 units of inventory from a supplier on account on 01/05 at a total cost of $9,000, with terms n/30.

- d. OTP paid a courier $300 cash on 01/05 for same-day delivery of the 150 units of inventory.

- e. The 30 units that OTP’s customer paid for in advance in December are delivered to the customer on 01/06.

- f. On 01/07, OTP received a purchase allowance of $1,350 on account, and then paid the amount necessary to settle the balance owed to the supplier for the 1/05 purchase of inventory (in c).

- g. Sales of 40 units of inventory occurring during the period of 01/07–01/10 are recorded on 01/10. The sales terms are n/30.

- h. Collected payments on 01/14 from sales to customers recorded on 01/10.

- i. OTP paid the first 2 weeks’ wages to the employees on 01/16. The total paid is $2,200.

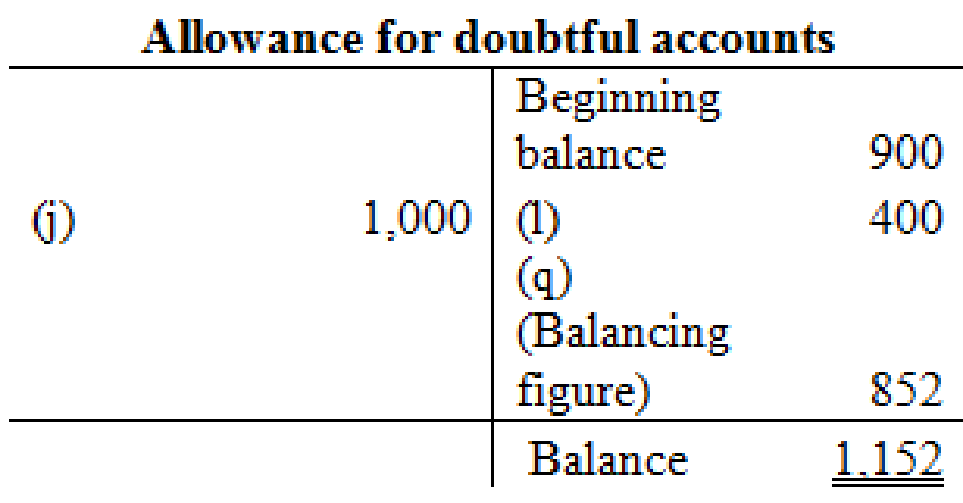

- j. Wrote off a $1,000 customer’s account balance on 01/18. OTP uses the allowance method, not the direct write-off method.

- k. Paid $2,600 on 01/19 for December and January rent. See the earlier bullets regarding the December portion. The January portion will expire soon, so it is charged directly to expense.

- l. OTP recovered $400 cash on 01/26 from the customer whose account had previously been written off on 01/18.

- m. An unrecorded $400 utility bill for January arrived on 01/27. It is due on 02/15 and will be paid then.

- n. Sales of 65 units of inventory during the period of 01/10–01/28, with terms n/30, are recorded on 01/28.

- o. Of the sales recorded on 01/28, 15 units are returned to OTP on 01/30. The inventory is not damaged and can be resold. OTP charges sales returns directly against Sales Revenue.

- p. On 01/31, OTP records the $2,200 employee salary that is owed but will be paid February 1.

- q. OTP uses the aging method to estimate and adjust for uncollectible accounts on 01/31. All of OTP’s accounts receivable fall into a single aging category, for which 8% is estimated to be uncollectible. (Update the balances of both relevant accounts prior to determining the appropriate adjustment, and round your calculation to the nearest dollar.)

- r. Accrue interest for January on the note payable on 01/31.

- s. Accrue interest for January on Jeff Letrotski’s note on 0 1/3 1 (see a).

Required:

- 1. Prepare all January

journal entries and adjusting entries for items (a)–(s). - 2. If you are completing this problem manually, set up T-accounts using the December 31 balances as the beginning balances,

post the journal entries from requirement 1, and prepare an adjustedtrial balance at January 31. If you are completing this problem in Connect using the general ledger tool, this requirement will be completed automatically using your previous answers. - 3. Prepare an income statement, statement of

retained earnings , and classifiedbalance sheet at the end of January. - 4. For the month ended January 31, indicate the (i) gross profit percentage (rounded to one decimal place), (ii) number of units in ending inventory, and (iii) cost per unit of ending inventory (include dollars and cents).

- 5. If OTP had used the percentage of sales method (using 2% of Net Sales) rather than the aging method, what amounts would OTC’s January financial statements have reported for (i) Bad Debt Expense and (ii) Accounts Receivable, net?

- 6. If OTP had used LIFO rather than FIFO, what amount would OTC have reported for Cost of Goods Sold on 01/10?

1.

Prepare the journal entries and adjusting entries for items (a) to (s).

Explanation of Solution

Accounts receivable: Accounts receivable refers to the amounts to be received within a short period from customers upon the sale of goods and services on account. In other words, accounts receivable are amounts customers owe to the business. Accounts receivable is an asset of a business.

Prepare the journal entries and adjusting entries for items (a) to (s).

| Date | Account Title and Explanation | Debit | Credit | |

| a. | January 1 | Note receivable | $1,500 | |

| Account receivable | $1,500 | |||

| (To record the acceptance of note) | ||||

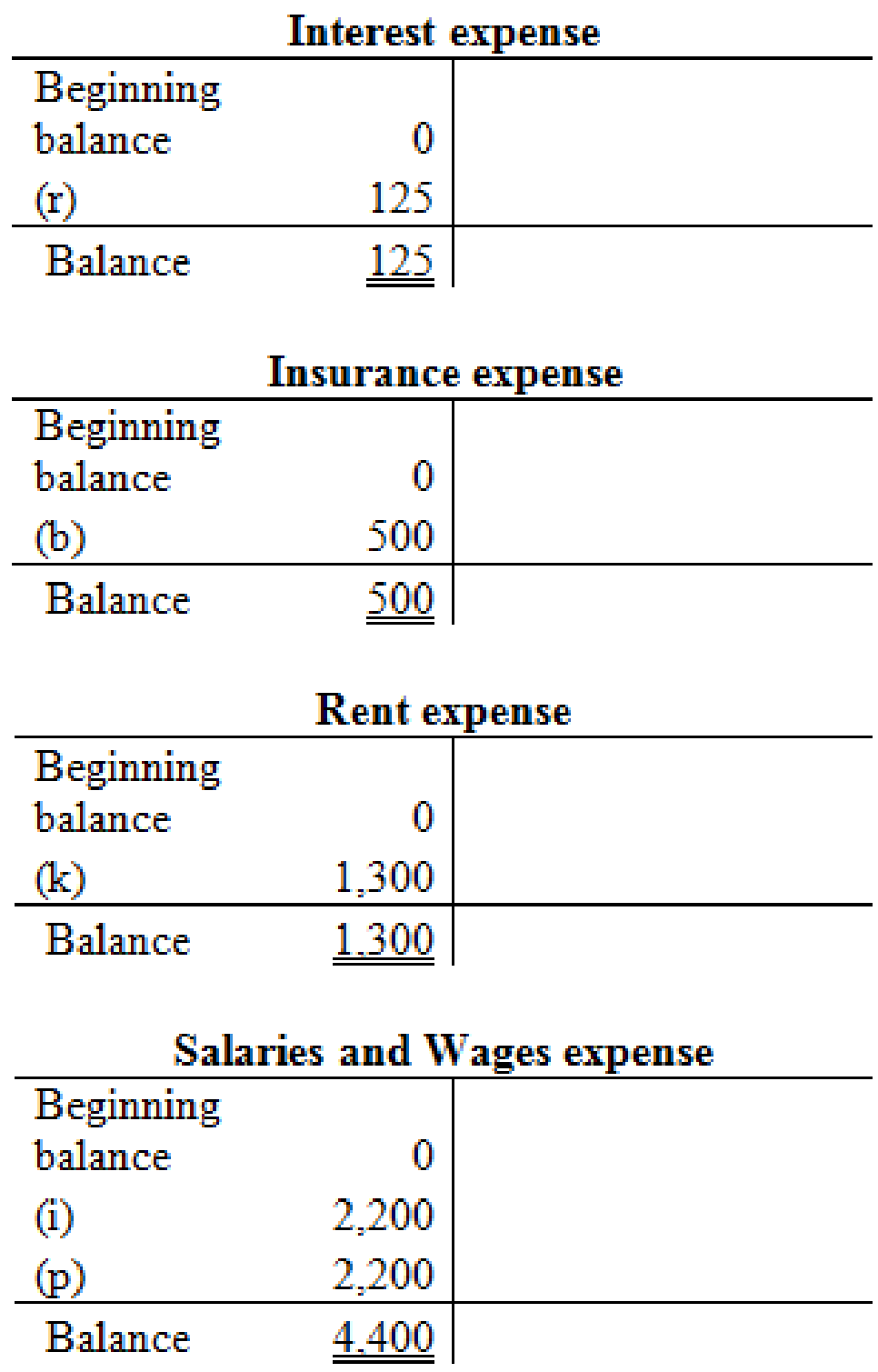

| b. | January 2 | Insurance expense | $500 | |

| Cash | $500 | |||

| (To record the insurance expense ) | ||||

| c. | January 5 | Inventory | $9,000 | |

| Accounts payable | $9,000 | |||

| (To record the purchase of inventory on account) | ||||

| d. | January 5 | Inventory | $300 | |

| Cash | $300 | |||

| (To record the purchase of inventory for cash) | ||||

| e. | January 6 | Deferred revenue | $4,350 | |

| Sales revenue | $4,350 | |||

| (To record the earned deferred revenue) | ||||

| January 6 |

Cost of goods sold | $2,400 | ||

| Sales revenue | $2,400 | |||

| (To record the cost of goods sold) | ||||

| f. | January 7 | Accounts payable | $9,000 | |

| Cash | $7,650 | |||

| Inventory | $1350 | |||

| (To record the settlement of payables) | ||||

| g. |

January 10 | Accounts receivable | $5,800 | |

|

Sales revenue | $5,800 | |||

| (To record the sales provided on account) | ||||

| January 10 |

Cost of goods sold | $2,255 | ||

| Sales revenue | $2,255 | |||

| (To record the cost of goods sold) | ||||

| h. | January 14 | Cash | $5,800 | |

| Accounts receivable | $5,800 | |||

| (To record the collection of cash on account) | ||||

| i. | January 16 | Salaries and Wages expense | $2,200 | |

| Cash | $2,200 | |||

| (To record the salaries and wages expense) | ||||

| j. | January 18 | Allowance for doubtful accounts | $1,000 | |

| Accounts receivable | $1,000 | |||

| (To record the write off) | ||||

| k. | January 19 | Accounts payable | $1,300 | |

| Rent expense | $1,300 | |||

| Cash | $2,600 | |||

| (To record the payment of rent expense and accounts payable) | ||||

| l. | January 26 | Accounts receivable | $400 | |

| Allowance for doubtful accounts | $400 | |||

| (To reverse the written off bad debt) | ||||

| January 26 | Cash | $400 | ||

| Accounts receivable | $400 | |||

| (To record the collection of cash on account) | ||||

| m. | January 27 | Utilities expense | $400 | |

| Accounts payable | $400 | |||

| (To record the accrued utilities expense) | ||||

| n. |

January 28 | Accounts receivable | $9,425 | |

|

Sales revenue | $9,425 | |||

| (To record the sales provided on account) | ||||

| January 28 |

Cost of goods sold | $3,445 | ||

| Sales revenue | $3,445 | |||

| (To record the cost of goods sold) | ||||

| o. | January 30 | Sales returns and allowances | $2,175 | |

| Accounts receivable | $2,175 | |||

| (To record the sales returns) | ||||

| January 30 | Inventory | $795 | ||

| Cost of goods sold | $795 | |||

| (To record the cost of goods sold) | ||||

| p. | January 31 | Salaries and Wages expense | $2,200 | |

| Salaries and Wages payable | $2,200 | |||

| (To record the salaries and wages expense) | ||||

| q. | January 31 | Bad debt expense (1) | $852 | |

| Allowance for doubtful accounts | $852 | |||

| (To record the bad debt expense) | ||||

| r. | January 31 | Interest expense | $125 | |

| Interest payable | $125 | |||

| (To record the interest expense) | ||||

| s. | January 31 | Interest receivable | $15 | |

| Interest revenue | $15 | |||

| (To record the interest revenue) | ||||

Table (1)

Working note (1):

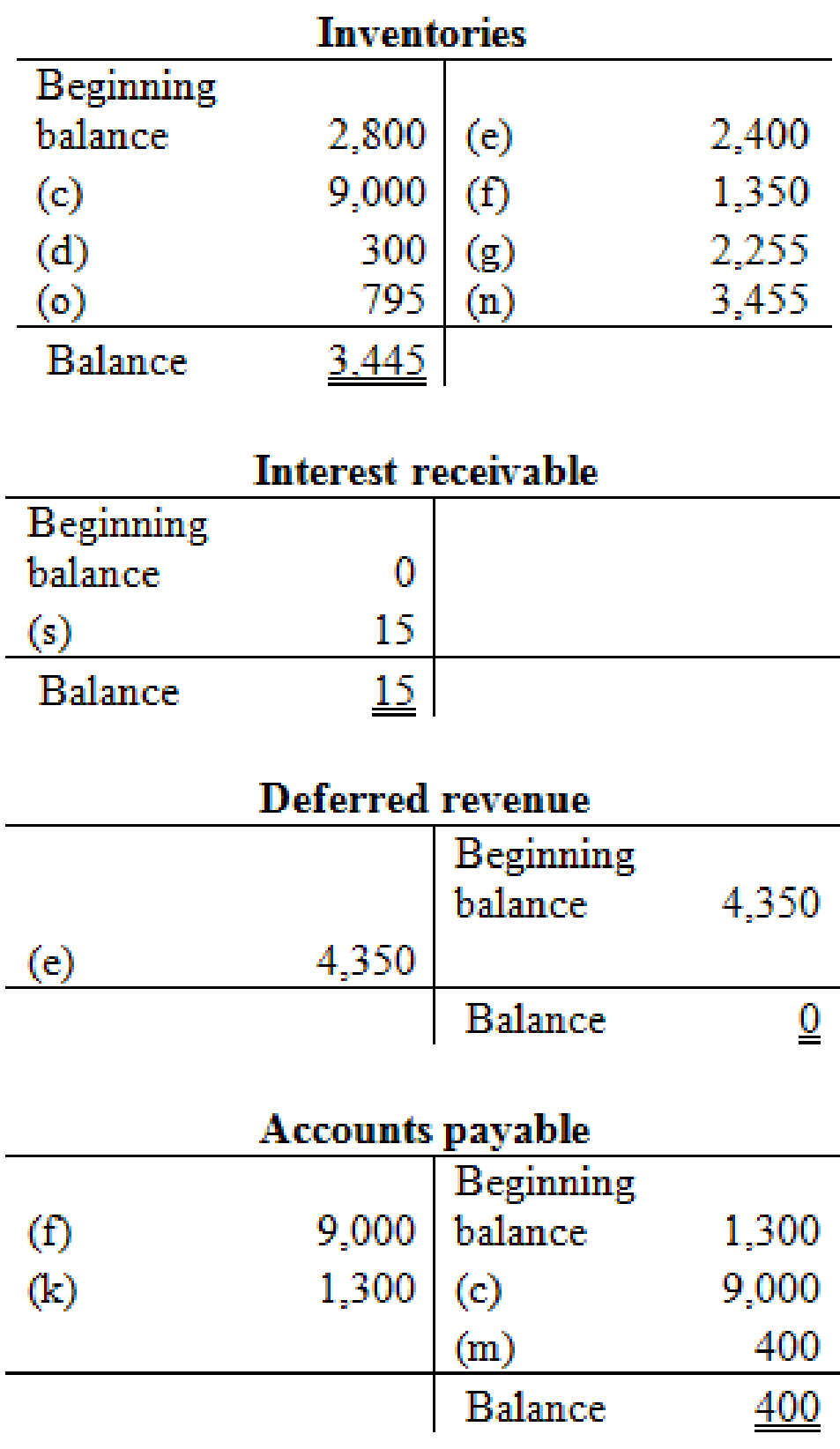

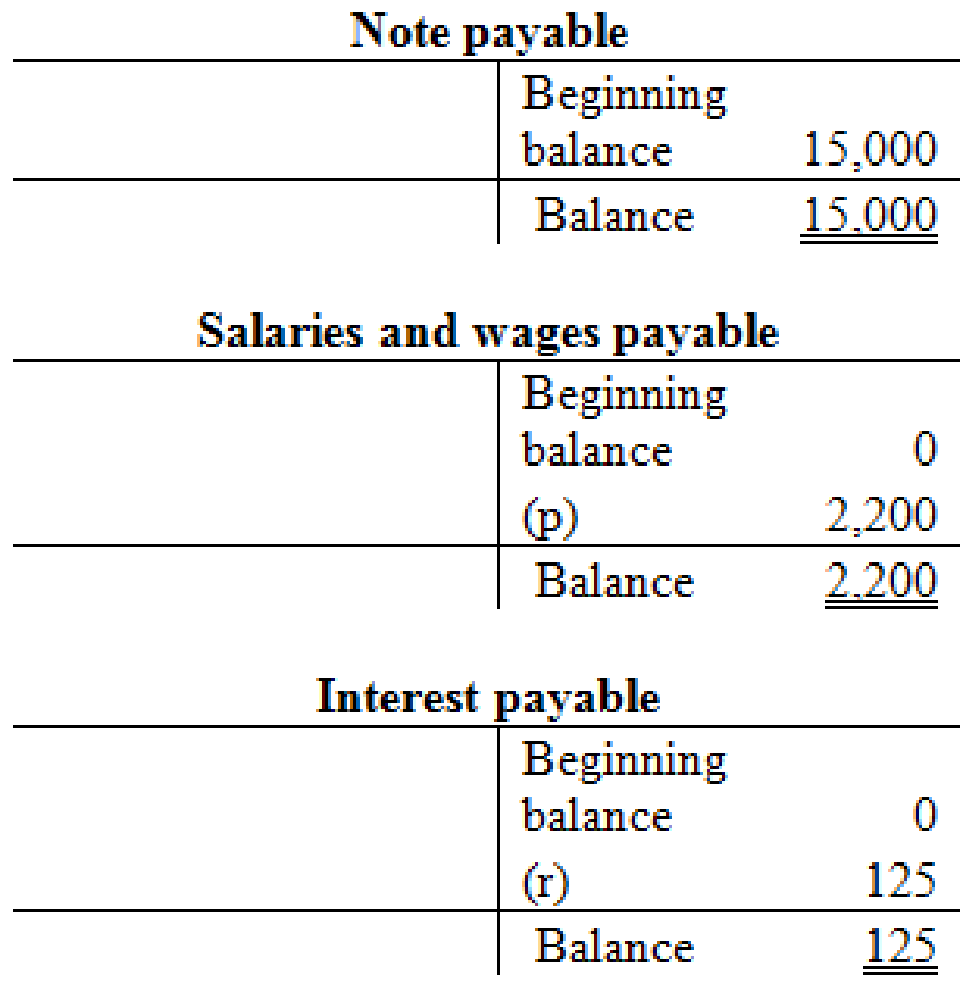

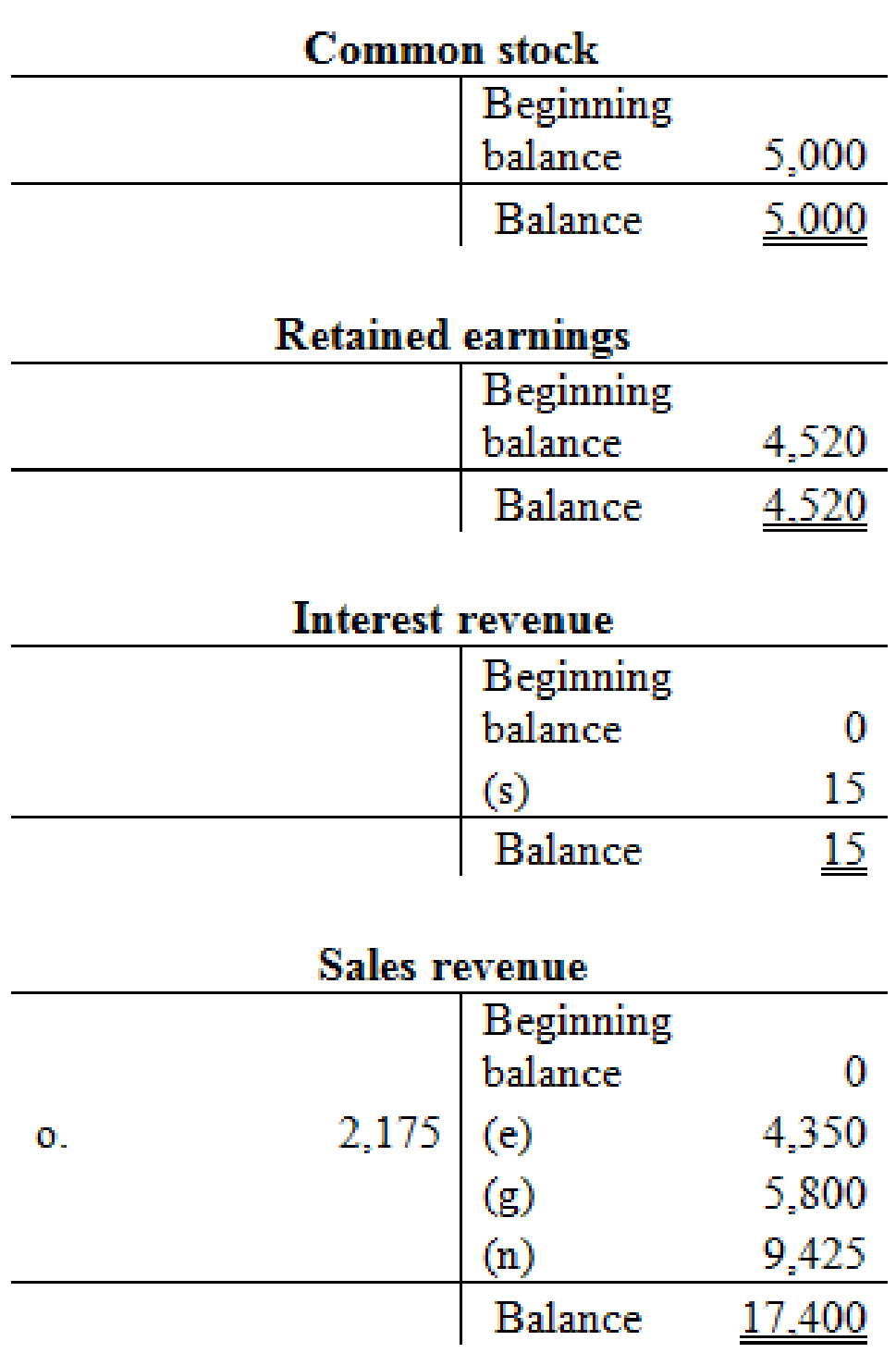

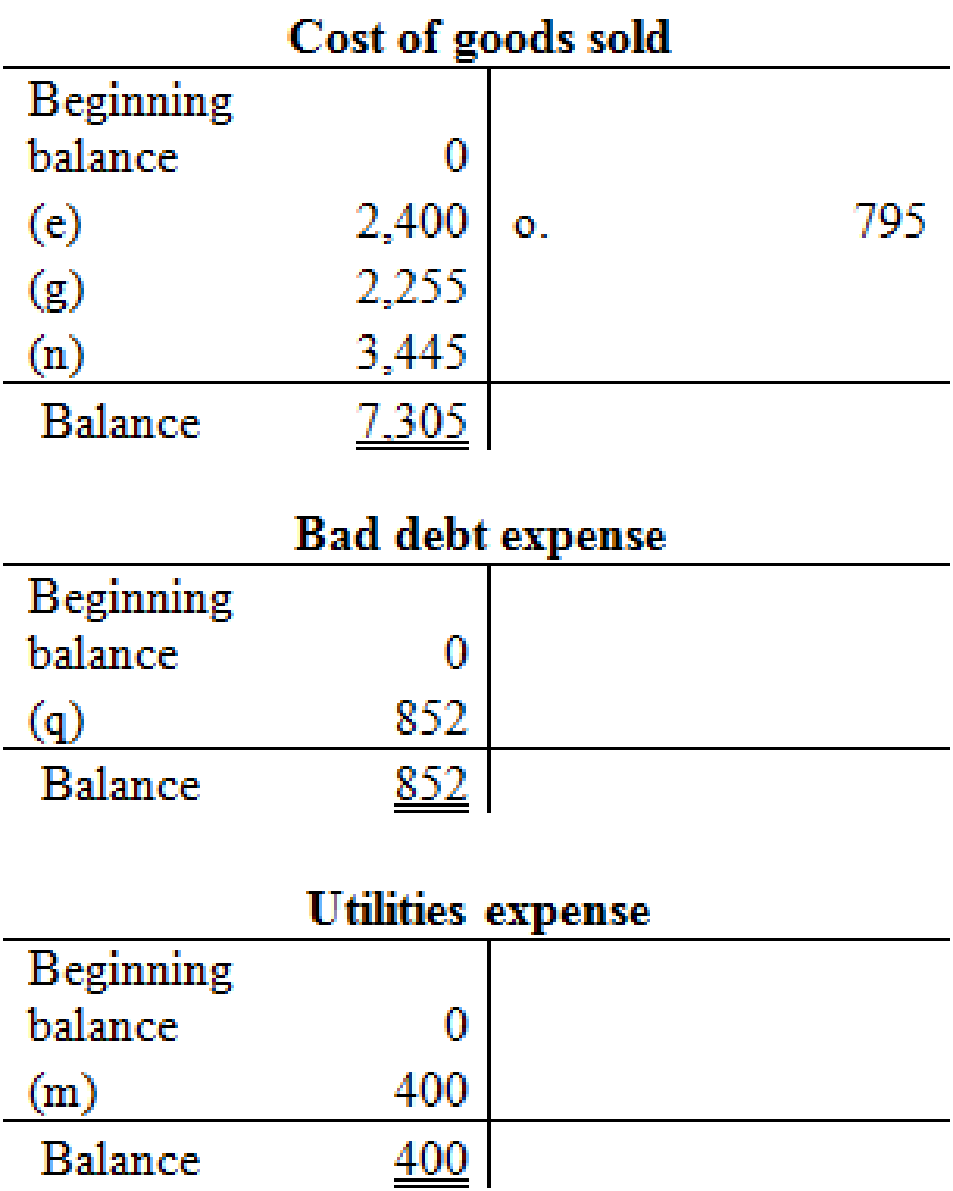

Step 1: Prepare T-account for accounts receivable.

Step 2: Determine the desired ending balance for allowance for doubtful accounts.

Step 3: Now, determine the bad debt expense to be reported on January 31 using T-account for allowance for doubtful accounts.

2.

Set up T-account and post the journal entries, and prepare adjusted trial balance.

Explanation of Solution

Adjusted trial balance: Adjusted trial balance is that statement which contains complete list of accounts with their adjusted balances, after all relevant adjustments have been made. This statement is prepared at the end of every financial period.

Set up T-account and post the journal entries as follows:

Prepare adjusted trial balance for Company OTP as follows:

| Company OTP | ||

| Adjusted trial balance | ||

| January 31 | ||

| Account Titles | Debit | Credit |

| Cash | $11,570 | |

| Accounts Receivable | 14,400 | |

| Allowance for Doubtful Accounts | $1,152 | |

| Inventory | 3,445 | |

| Note Receivable | 1,500 | |

| Interest Receivable | 15 | |

| Deferred Revenue | 0 | |

| Accounts Payable | 400 | |

| Salaries and Wages Payable | 2,200 | |

| Interest Payable | 125 | |

| Note Payable | 15,000 | |

| Common Stock | 5,000 | |

| Retained Earnings | 4,520 | |

| Sales Revenue | 17,400 | |

| Cost of Goods Sold | 7,305 | |

| Salaries and Wages Expense | 4,400 | |

| Rent Expense | 1,300 | |

| Bad Debt Expense | 852 | |

| Insurance Expense | 500 | |

| Utilities Expense | 400 | |

| Interest Expense | 125 | |

| Interest Revenue | 15 | |

| Totals | $45,812 | $45,812 |

Table (2)

3.

Prepare an income statement, retained earnings statement and classified balance sheet for the month ended January 31.

Explanation of Solution

Income statement: The financial statement which reports revenues and expenses from business operations and the result of those operations as net income or net loss for a particular time period is referred to as income statement.

Prepare an income statement for Company OTP as follows:

| Company OTP | |

| Income Statement | |

| For the Month Ended January 31 | |

| Particulars | Amount |

| Sales Revenue | $17,400 |

| Less: Cost of Goods Sold | 7,305 |

| Gross Profit | 10,095 |

| Less: Salaries and Wages Expense | 4,400 |

| Rent Expense | 1,300 |

| Bad Debt Expense | 852 |

| Insurance Expense | 500 |

| Utilities Expense | 400 |

| Income from Operations | 2,643 |

| Less: Interest Revenue (Expense), net | 110 |

| Net Income | $2,533 |

Table (3)

Statement of Retained Earnings: Statement of retained earnings shows, the changes in the retained earnings, and the income left in the company after payment of the dividends, for the accounting period.

Prepare the statement of retained earnings for Company OTP as follows:

| Company OTP | |

| Statement of Retained Earnings | |

| For the Month Ended January 31 | |

| Particulars | Amount |

| Balance, January 1 | $ 4,520 |

| Add: Net Income | 2,533 |

| Less: Dividends | 0 |

| Balance, December 31 | $ 7,053 |

Table (4)

Classified balance sheet: The main elements of balance sheet assets, liabilities, and stockholders’ equity are categorized or classified further into sections, and sub-sections in a classified balance sheet. Assets are further classified as current assets, long-term investments, property, plant, and equipment (PPE), and intangible assets. Liabilities are classified into two sections current and long-term. Stockholders’ equity comprises of common stock and retained earnings. Thus, the classified balance sheet includes all the elements under different sections.

Prepare classified balance sheet for Company OTP as follows:

| Company OTP | |

| Balance Sheet | |

| At December 31 | |

| Assets | Amount |

| Current Assets: | |

| Cash | $11,570 |

| Accounts Receivable | 14,400 |

| Less: Allowance for Doubtful Accounts | -1,152 |

| Inventory | 3,445 |

| Note Receivable | 1,500 |

| Interest Receivable | 15 |

| Total Assets | $29,778 |

| Liabilities and Stockholders’ Equity | Amount |

| Liabilities | |

| Current Liabilities: | |

| Accounts Payable | $400 |

| Salaries and Wages Payable | 2,200 |

| Interest Payable | 125 |

| Total Current Liabilities | 2,725 |

| Note Payable | 15,000 |

| Total Liabilities (a) | 17,725 |

| Stockholders’ Equity | |

| Common Stock | 5,000 |

| Retained Earnings | 7,053 |

| Total Stockholders’ Equity (b) | 12,053 |

| Total Liabilities and Stockholders’ Equity | $29,778 |

Table (5)

4.

Calculate the following:

- i. The gross profit percentage.

- ii. The number of units in ending inventory.

- iii. Cost per unit of ending inventory.

Explanation of Solution

Gross margin percentage: The percentage of gross profit generated by every dollar of net sales is referred to as gross profit percentage. This ratio measures the profitability of a company by quantifying the amount of income earned from sales revenue generated after cost of goods sold are paid. The higher the ratio, the more ability to cover operating expenses.

- i. Calculate the gross profit percentage as follows:

Thus, the gross profit percentage is 58.01%.

- ii. Calculate the number of units in ending inventory as follows:

| Particulars | Number of units |

| Inventory as of January 1 | 35 |

| Add: Inventory purchased on January 5 | 150 |

| Less: Inventory sold on January 6 | -30 |

| Less: Inventory sold on January 10 | -40 |

| Less: Inventory sold on January 28 | -65 |

| Add: Inventory returned on January 30 | 15 |

| Number of units on hand as of January 31 | 65 |

Table (6)

Thus, the number of units in ending inventory as of January 31 is 65 units.

- iii. Calculate the cost per unit of ending inventory as follows:

Hence, the cost per unit of ending inventory is $53 per unit.

5.

Calculate the net amount that would be reported by Company OTC for (i) bad debt expense, and (ii) accounts receivable, if it uses percentage of sale method.

Explanation of Solution

Bad debt expense: Bad debt expense is an expense account. The amounts of loss incurred from extending credit to the customers are recorded as bad debt expense. In other words, the estimated uncollectible accounts receivable are known as bad debt expense.

- i. Calculate the amount of bad debt expense.

Therefore, Company OTP would have reported $348 as bad debt expense if it uses percentage of sales method.

- ii. Calculate the amount of accounts receivable, net.

Step 1: Prepare T-account for allowance for doubtful accounts according calculated bad debts based on percentage of credit sales method.

| Allowance for doubtful accounts | ||||

| Beginning balance | 900 | |||

| (j) | 1,000 | (l) | 400 | |

| Bad debt expense | 348 | |||

| Balance | 648 | |||

Step 2: Calculate the accounts receivable, net.

Therefore, Company OTP would have reported $13,752 as accounts receivable, net, if it uses percentage of sales method.

6.

Calculate the amount of cost of goods sold that would be reported by Company OTC on January 10, if it uses LIFO instead of FIFO.

Explanation of Solution

First-in-First-Out (FIFO): In this method, items purchased initially are sold first. So, the value of the ending inventory consists the recent cost for the remaining unsold items.

Last-in-First-Out (LIFO): In this method, items purchased recently are sold first. So, the value of the ending inventory consists the initial cost for the remaining unsold items.

If Company OTP uses LIFO (Last-In First Out) instead of FIFO (First-In First Out), then it would have used the cost of goods that was acquired in recent times to calculate the cost of goods sold.

For January 10, the most recently purchased goods is $9,000 of 150 units on January 5, however the cost of goods sold is changed later due to the cost of freight and purchase discount, which is calculated as follows:

| Cost of goods sold | |

| Particulars | $ |

| Purchase value of goods | $9,000 |

| Add: Freight-in | $300 |

| Less: Purchase discount | –$1,350 |

| Cost of goods sold | $7,950 |

Table (7)

These 150 units cost is $7,950, and whose cost per unit is

Thus, at a LIFO unit cost of $53, the 40 units sold on January 10 would have produced a cost of goods sold of

Thus, at a LIFO unit cost of $53, the 40 units sold on January 10 would have produced a cost of goods sold of $2,120.

Want to see more full solutions like this?

Chapter 8 Solutions

FUNDAMENTALS OF FINANCIAL ACCOUNTING

Additional Business Textbook Solutions

Financial Accounting, Student Value Edition (5th Edition)

Marketing: An Introduction (13th Edition)

Principles of Microeconomics (MindTap Course List)

Principles of Operations Management: Sustainability and Supply Chain Management (10th Edition)

Gitman: Principl Manageri Finance_15 (15th Edition) (What's New in Finance)

Intermediate Accounting (2nd Edition)

- Please provide the solution to this financial accounting question using proper accounting principles.arrow_forwardOn May 31, 2026, Oriole Company paid $3,290,000 to acquire all of the common stock of Pharoah Corporation, which became a division of Oriole. Pharoah reported the following balance sheet at the time of the acquisition: Current assets $846,000 Current liabilities $564,000 Noncurrent assets 2,538,000 Long-term liabilities 470,000 Stockholder's equity 2,350,000 Total assets $3,384,000 Total liabilities and stockholder's equity $3,384,000 It was determined at the date of the purchase that the fair value of the identifiable net assets of Pharoah was $2,914,000. At December 31, 2026, Pharoah reports the following balance sheet information: Current assets $752,000 Noncurrent assets (including goodwill recognized in purchase) 2,256,000 Current liabilities (658,000) Long-term liabilities (470,000) Net assets $1,880,000 It is determined that the fair value of the Pharoah division is $2,068,000.arrow_forwardOn May 31, 2026, Oriole Company paid $3,290,000 to acquire all of the common stock of Pharoah Corporation, which became a division of Oriole. Pharoah reported the following balance sheet at the time of the acquisition: Current assets $846,000 Current liabilities $564,000 Noncurrent assets 2,538,000 Long-term liabilities 470,000 Stockholder's equity 2,350,000 Total assets $3,384,000 Total liabilities and stockholder's equity $3,384,000 It was determined at the date of the purchase that the fair value of the identifiable net assets of Pharoah was $2,914,000. At December 31, 2026, Pharoah reports the following balance sheet information: Current assets $752,000 Noncurrent assets (including goodwill recognized in purchase) 2,256,000 Current liabilities (658,000) Long-term liabilities (470,000) Net assets $1,880,000 It is determined that the fair value of the Pharoah division is $2,068,000.arrow_forward

- The following transactions involving intangible assets of Oriole Corporation occurred on or near December 31, 2025. 1.) Oriole paid Grand Company $520,000 for the exclusive right to market a particular product, using the Grand name and logo in promotional material. The franchise runs for as long as Oriole is in business. 2.) Oriole spent $654,000 developing a new manufacturing process. It has applied for a patent, and it believes that its application will be successful. 3.) In January 2026, Oriole's application for a patent (#2 above) was granted. Legal and registration costs incurred were $247,800. The patent runs for 20 years. The manufacturing process will be useful to Oriole for 10 years. 4.) Oriole incurred $168,000 in successfully defending one of its patents in an infringement suit. The patent expires during December 2029. 5.) Oriole incurred $446,400 in an unsuccessful patent defense. As a result of the adverse verdict, the patent, with a remaining unamortized cost of…arrow_forwardReffering to fair value of an asset, division, or organization, What exactly is fair value and how is it assessed?arrow_forwardThe following transactions involving intangible assets of Oriole Corporation occurred on or near December 31, 2025. 1.) Oriole paid Grand Company $520,000 for the exclusive right to market a particular product, using the Grand name and logo in promotional material. The franchise runs for as long as Oriole is in business. 2.) Oriole spent $654,000 developing a new manufacturing process. It has applied for a patent, and it believes that its application will be successful. 3.) In January 2026, Oriole's application for a patent (#2 above) was granted. Legal and registration costs incurred were $247,800. The patent runs for 20 years. The manufacturing process will be useful to Oriole for 10 years. 4.) Oriole incurred $168,000 in successfully defending one of its patents in an infringement suit. The patent expires during December 2029. Oriole incurred 5.) $446,400 in an unsuccessful patent defense. As a result of the adverse verdict, the patent, with a remaining unamortized cost of…arrow_forward

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,