Concept explainers

Videos

In the Ardmore Hotel, 20 percent of the customers pay by American Express credit card. (a) Of the next 10 customers, what is the

(a)

Find the probability that no one will pay by American Express.

Answer to Problem 23SE

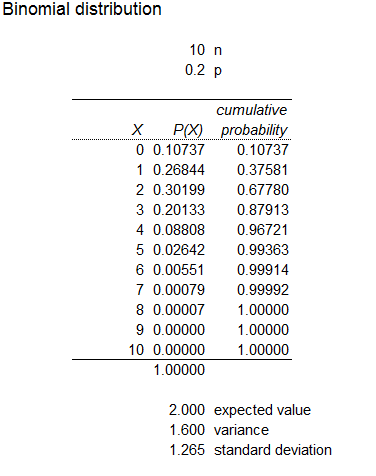

The probability for none of them pay by American express out of 10 customers is 0.1074.

Explanation of Solution

Calculation:

The given information is that in Ardmore hotel, the customers pay by American express credit card is nearly 20%.

Binomial Distribution:

The random variable X denotes the number of successes in trail of n.

The PDF of the distribution is,

Here n denotes the number of trails and

In the given situation, the random variable X variable denotes the number of customers, the value of n is 10 and the value of

The probability for no one pay by American express card in next 10 customers is

Software procedure:

Step-by-step software procedure to obtain probability value using EXCEL software is as follows:

- Open an EXCEL file.

- In cell A1, enter the formula “=BINOM.DIST(0,10,0.20,0)”

- Output using EXCEL software is given below:

From the output, the value of

Thus, the probability for none of them pay by American express out of 10 customers is 0.1074.

(b)

Find the probability that at least two customers will pay by American Express.

Answer to Problem 23SE

The probability that at least two customers will pay by American Express is 0.6242.

Explanation of Solution

Calculation:

The probability for at least two customers pay by American express card in next 10 customers is,

Probability = 1– BINOM.DIST(x, n, probability, cumulative)

Software procedure:

Step-by-step software procedure to obtain probability value using EXCEL software is as follows:

- Open an EXCEL file.

- In cell A1, enter the formula “=BINOM.DIST(1,10,0.20,1)”

- Output using EXCEL software is given below:

From the output, the value of

Then the value of

Thus, the probability for at least 2 customers will pay by American express out of 10 customers is 0.6242.

(c)

Find the probability that fewer than 3 customers will pay by American Express.

Answer to Problem 23SE

The probability that fewer than 3 customers will pay by American Express is 0.6778.

Explanation of Solution

Calculation:

The probability for fewer than 3 customers pay by American express card in next 10 customers is,

Software procedure:

Step-by-step software procedure to obtain probability value using EXCEL software is as follows:

- Open an EXCEL file.

- In cell A1, enter the formula “=BINOM.DIST(2,10,0.20,1)”

- Output using EXCEL software is given below:

From the output, the value of

Thus, the probability for fewer than 3 customers will pay by American express out of 10 customers is 0.6778.

(d)

Find the expected number of customers will by American express.

Answer to Problem 23SE

The expected number of customers will by American express is 2.

Explanation of Solution

Calculation:

The formula for expected value is,

The expected number of customers is,

Thus, the expected number of customers pay by American express is 2.

(e)

Find the standard deviation.

Answer to Problem 23SE

The standard deviation is 1.2649.

Explanation of Solution

Calculation:

The formula for standard deviation is,

Calculate the standard deviation is,

Thus, the standard deviation is 1.2649.

(f)

Construct the probability distribution.

Explanation of Solution

Calculation:

Construct the probability distribution:

Software procedure:

Step by step procedure to obtain probability distribution by using MegaStat software is as follows:

- Open an EXCEL file, Go to Add-ins, select MegaStat.

- Choose Probability, select the Discrete probability distributions.

- In Binomial, enter number of trails as 10 and probability occurrence as 0.2.

- Click on Ok.

- Output using EXCEL software is given below:

(g)

Draw the graph for PDF and shape of the distribution.

Answer to Problem 23SE

The distribution shape is right-skewed.

Explanation of Solution

Calculation:

Shape of the distribution:

Symmetric distribution:

When the left and right sides of the distribution are approximately equal or mirror images of each other, then it is symmetric distribution. For this distribution, mean and standard deviation are useful. For a symmetric distribution,

Right skewed distribution:

If the tail of the distribution is elongated towards the right, then it is a right-skewed distribution. It is also called as positively skewed. For right skewed,

Left-skewed distribution:

If the tail of the distribution is elongated towards the left, then it is a left-skewed distribution. It is also called as negatively skewed. For left skewed,

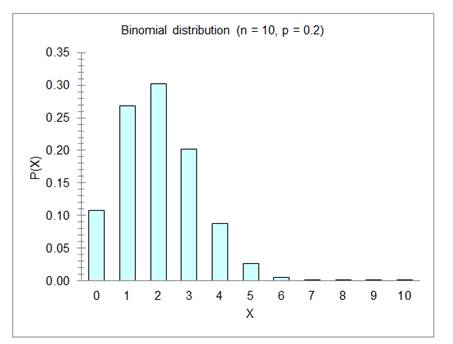

Graph of the probability distribution:

Software procedure:

Step by step procedure to obtain probability distribution by using MegaStat software is as follows:

- Open an EXCEL file, Go to Add-ins, select MegaStat.

- Choose Probability, select the Discrete probability distributions.

- In Binomial, enter number of trails as 10 and probability occurrence as 0.2.

- Select Display graph.

- Click on Ok.

- Output using EXCEL software is given below:

Observation:

From the output, the tail of the distribution is elongated towards the right.

Thus, the distribution shape is right-skewed.

Want to see more full solutions like this?

Chapter 6 Solutions

APPLIED STAT.IN BUS.+ECONOMICS

- A marketing agency wants to determine whether different advertising platforms generate significantly different levels of customer engagement. The agency measures the average number of daily clicks on ads for three platforms: Social Media, Search Engines, and Email Campaigns. The agency collects data on daily clicks for each platform over a 10-day period and wants to test whether there is a statistically significant difference in the mean number of daily clicks among these platforms. Conduct ANOVA test. You can provide your answer by inserting a text box and the answer must include: also please provide a step by on getting the answers in excel Null hypothesis, Alternative hypothesis, Show answer (output table/summary table), and Conclusion based on the P value.arrow_forwardA company found that the daily sales revenue of its flagship product follows a normal distribution with a mean of $4500 and a standard deviation of $450. The company defines a "high-sales day" that is, any day with sales exceeding $4800. please provide a step by step on how to get the answers Q: What percentage of days can the company expect to have "high-sales days" or sales greater than $4800? Q: What is the sales revenue threshold for the bottom 10% of days? (please note that 10% refers to the probability/area under bell curve towards the lower tail of bell curve) Provide answers in the yellow cellsarrow_forwardBusiness Discussarrow_forward

- The following data represent total ventilation measured in liters of air per minute per square meter of body area for two independent (and randomly chosen) samples. Analyze these data using the appropriate non-parametric hypothesis testarrow_forwardeach column represents before & after measurements on the same individual. Analyze with the appropriate non-parametric hypothesis test for a paired design.arrow_forwardShould you be confident in applying your regression equation to estimate the heart rate of a python at 35°C? Why or why not?arrow_forward

Glencoe Algebra 1, Student Edition, 9780079039897...AlgebraISBN:9780079039897Author:CarterPublisher:McGraw Hill

Glencoe Algebra 1, Student Edition, 9780079039897...AlgebraISBN:9780079039897Author:CarterPublisher:McGraw Hill Holt Mcdougal Larson Pre-algebra: Student Edition...AlgebraISBN:9780547587776Author:HOLT MCDOUGALPublisher:HOLT MCDOUGAL

Holt Mcdougal Larson Pre-algebra: Student Edition...AlgebraISBN:9780547587776Author:HOLT MCDOUGALPublisher:HOLT MCDOUGAL