Concept explainers

Videos

Calculate ending inventory and cost of goods sold for four inventory methods (LO6–3)

PROBLEMS: SET B

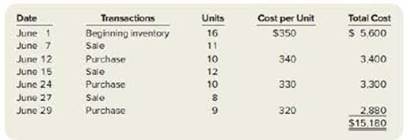

Jimmie’s Fishing Hole has the following transactions related to its top-selling Shimano fishing reel for the month of June:

Requited:

1. Calculate ending inventory and cost of goods sold at June 30, using the specific identification method The June 7 sale consists of fishing reels from beginning inventory, the June 15 sale consists of three fishing reels from beginning inventory and nine fishing reels from the June 12 purchase, and the June 27 sale consists of one fishing reel from beginning inventory and seven fishing reels from the June 21 purchase.

2. Using FIFO, calculate ending inventory and cost of goods sold at June 30.

3. Using LIFO, calculate ending inventory arid cost of goods sold at June 30.

4. Using weighted average cost, calculate ending inventory and cost of goods sold at June 30.

Want to see the full answer?

Check out a sample textbook solution

Chapter 6 Solutions

Financial Accounting

- I am searching for the accurate solution to this general accounting problem with the right approach.arrow_forwardPlease explain the solution to this general accounting problem with accurate principles.arrow_forwardCan you show me the correct approach to solve this financial accounting problem using suitable standards?arrow_forward

- Can you solve this financial accounting question with accurate accounting calculations?arrow_forwardI need assistance with this financial accounting problem using valid financial procedures.arrow_forwardBowen Corporation had sales revenue of $925,000 and cost of goods sold of $555,000. Operating expenses were $245,000, which included depreciation expense of $35,000. The company also recorded interest expense of $28,000. What was Bowen Corporation's income before taxes?arrow_forward

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning

Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,