Concept explainers

Videos

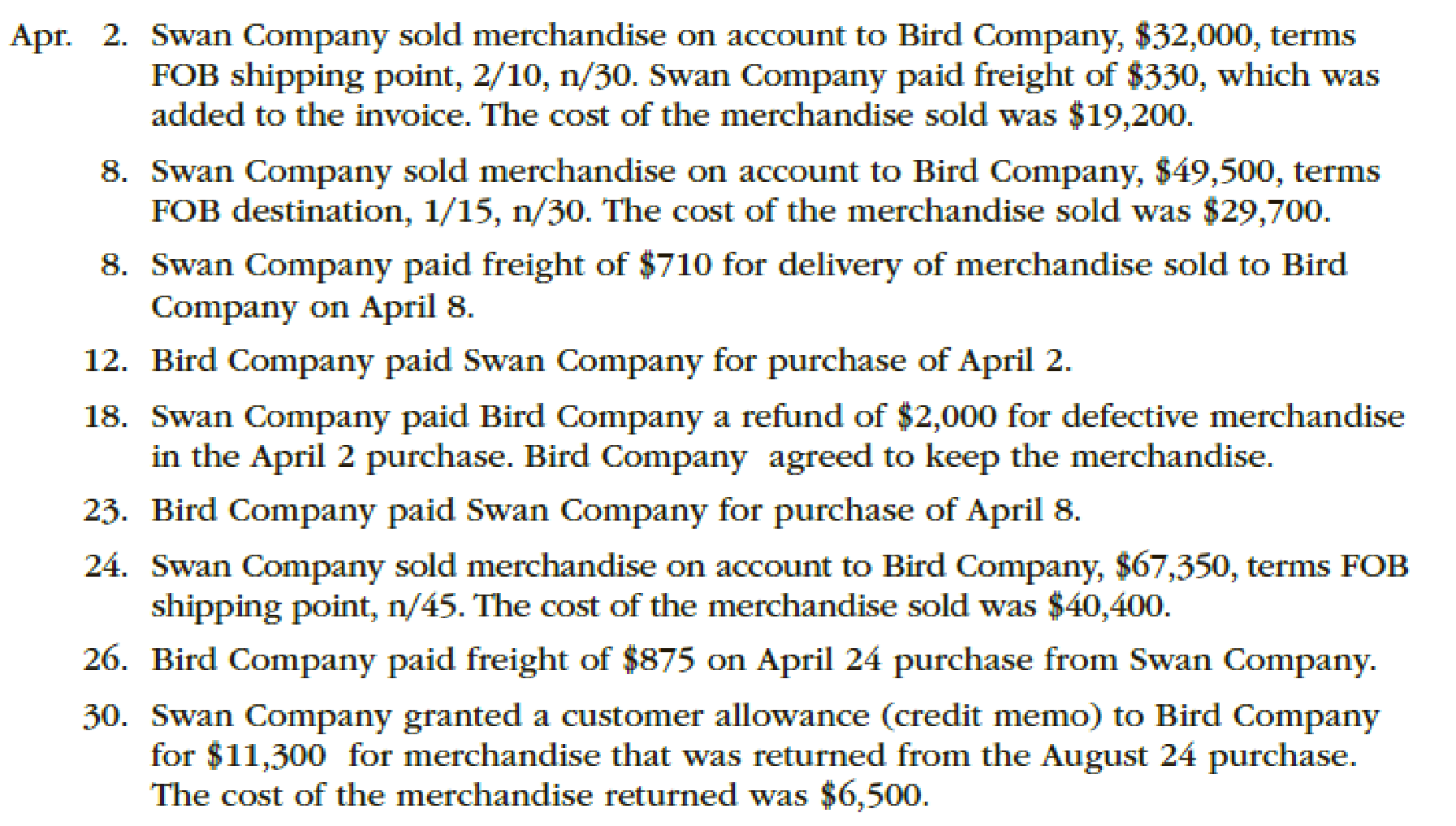

The following selected transactions were completed during April between Swan Company and Bird Company:

Instructions

Journalize the April transactions for (1) Swan Company and (2) Bird Company.

(1)

Prepare journal entries to record the transactions of Company S during the month of April using perpetual inventory system.

Explanation of Solution

Journal entry: Journal is the book of original entry whereby all the financial transactions are recorded in chronological order. Under this method each transaction has two sides, debit side and credit side. Total amount of debit side must be equal to the total amount of credit side. In addition, it is the primary books of accounts for any entity to record the daily transactions and processed further till the presentation of the financial statements.

The following are the rules of debit and credit:

- 1. Increase in assets and expenses accounts are debited. Decrease in liabilities and stockholders’ equity accounts are debited.

- 2. Increase in liabilities, revenues, and stockholders’ equity accounts are credited. Decreases in all asset accounts are credited.

Perpetual Inventory System refers to the Merchandise Inventory system that maintains the detailed records of every Merchandise Inventory transactions related to purchases and sales on a continuous basis. It shows the exact on-hand-merchandise inventory at any point of time.

Record the journal entry for the sale of inventory on account.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| April 2 | Accounts Receivable | 31,360 (1) | |

| Sales Revenue | 31,360 | ||

| (To record the sale of inventory on account) |

Table (1)

- Accounts receivable is an asset and it is increased by $31,360. Therefore, debit accounts receivable with $31,360.

- Sales revenue is revenue and it increases the value of equity by $31,360. Therefore, credit sales revenue with $31,360.

Working Note (1):

Calculate the amount of accounts receivable.

Sales = $32,000

Discount percentage = 2%

Record the journal entry for the freight paid.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| April 2 | Accounts Receivable | 330 | |

| Cash | 330 | ||

| (To record the freight paid) |

Table (2)

- Accounts receivable is an asset and it is increased by $330. Therefore, debit accounts receivable with $330.

- Cash is an asset and it is decreased by $330. Therefore, credit cash account with $330.

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| April 2 | Cost of Merchandise Sold | 19,200 | |

| Merchandise Inventory | 19,200 | ||

| (To record the cost of goods sold) |

Table (3)

- Cost of merchandise sold is an expense account and it decreases the value of equity by $19,200. Therefore, debit cost of merchandise sold account with $19,200.

- Merchandise Inventory is an asset and it is decreased by $19,200. Therefore, credit inventory account with $19,200.

Record the journal entry for the sale of inventory on account.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| April 8 | Accounts Receivable | 49,005 (2) | |

| Sales Revenue | 49,005 | ||

| (To record the sale of inventory on account) |

Table (4)

- Accounts receivable is an asset and it is increased by $49,005. Therefore, debit accounts receivable with $49,005.

- Sales revenue is revenue and it increases the value of equity by $49,005. Therefore, credit sales revenue with $49,005.

Working Note (2):

Calculate the amount of accounts receivable.

Sales = $49,500

Discount percentage = 1%

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| April 8 | Cost of Merchandise Sold | 29,700 | |

| Merchandise Inventory | 29,700 | ||

| (To record the cost of goods sold) |

Table (5)

- Cost of merchandise sold is an expense account and it decreases the value of equity by $29,700. Therefore, debit cost of merchandise sold account with $29,700.

- Merchandise Inventory is an asset and it is decreased by $29,700. Therefore, credit inventory account with $29,700.

Record the journal entry for delivery expense.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| April 8 | Delivery expense | 710 | |

| Cash | 710 | ||

| (To record the payment of delivery expenses) |

Table (6)

- Delivery expense is an expense account and it decreases the value of equity by $710. Therefore, debit delivery expense account with $710.

- Cash is an asset and it is decreased by $710. Therefore, credit cash account with $710.

Record the journal entry for the cash receipt against accounts receivable.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| April 12 | Cash | 31,690 (3) | |

| Accounts Receivable | 31,690 | ||

| (To record the receipt of cash against accounts receivables) |

Table (7)

Working Note (3):

Calculation the amount of cash receipt.

Net accounts receivable = $31,360

Accounts receivable for freight paid = $330

- Cash is an asset and it is increased by $31,690. Therefore, debit cash account with $31,690.

- Accounts Receivable is an asset and it is increased by $31,690. Therefore, debit accounts receivable with $31,690.

Record the journal entry for sales return.

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| April 18 | Customer Refunds Payable | 2,000 | ||

| Cash | 2,000 | |||

| (To record sales returns) |

Table (8)

- Customer refunds payable is a liability account and it is decreased by $2,000. Therefore, debit customer refunds payable account with $2,000.

- Accounts Receivable is an asset and it is decreased by $2,000. Therefore, credit account receivable with $2,000.

Record the journal entry for the cash receipt against accounts receivable.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| April 23 | Cash | 49,005 | |

| Accounts Receivable | 49,005 | ||

| (To record the receipt of cash against accounts receivables) |

Table (9)

- Cash is an asset and it is increased by $49,005. Therefore, debit cash account with $49,005.

- Accounts Receivable is an asset and it is increased by $49,005. Therefore, debit accounts receivable with $49,005.

Record the journal entry for the sale of inventory on account.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| April 24 | Accounts Receivable | 67,350 | |

| Sales Revenue | 67,350 | ||

| (To record the sale of inventory on account) |

Table (10)

- Accounts receivable is an asset and it is increased by $67,350. Therefore, debit accounts receivable with $67,350.

- Sales revenue is revenue and it increases the value of equity by $67,350. Therefore, credit sales revenue with $67,350.

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| April 24 | Cost of Merchandise Sold | 40,400 | |

| Merchandise Inventory | 40,400 | ||

| (To record the cost of goods sold) |

Table (11)

- Cost of merchandise sold is an expense account and it decreases the value of equity by $40,400. Therefore, debit cost of merchandise sold account with $40,400.

- Merchandise Inventory is an asset and it is decreased by $40,400. Therefore, credit inventory account with $40,400.

Record the journal entry for sales return.

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| April 30 | Customer Refunds Payable | 11,300 | ||

| Accounts Receivable | 11,300 | |||

| (To record sales returns) |

Table (12)

- Customer refunds payable is a liability account and it is decreased by $11,300. Therefore, debit customer refunds payable account with $11,300.

- Accounts Receivable is an asset and it is decreased by $11,300. Therefore, credit account receivable with $11,300.

Record the journal entry for the return of the merchandise.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| April 30 | Merchandise Inventory | 6,500 | |

| Estimated Returns Inventory | 6,500 | ||

| (To record the return of the merchandise) |

Table (13)

- Merchandise Inventory is an asset and it is increased by $6,500. Therefore, debit inventory account with $6,500.

- Estimated returns inventory is an expense account and it increases the value of equity by $6,500. Therefore, credit estimated returns inventory account with $6,500.

(2)

Prepare journal entries to record the transactions of Company B during the month of April using perpetual inventory system.

Explanation of Solution

Record the journal entry of Company B.

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| April 2 | Merchandise Inventory | 31,690 | ||

| Accounts payable | 31,690 (4) | |||

| (To record purchase on account) |

Table (14)

- Merchandise Inventory is an asset and it is increased by $31,690. Therefore, debit Merchandise Inventory account with $31,690.

- Accounts payable is a liability and it is increased by $31,690. Therefore, credit accounts payable account with $31,690.

Working Note (4):

Calculate the amount of accounts payable.

Purchases = $31,360

Freight charges = $330

Record the journal entry of Company B.

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| August 8 | Merchandise Inventory | 49,005 | ||

| Accounts payable | 49,005 (5) | |||

| (To record purchase on account) |

Table (15)

- Merchandise Inventory is an asset and it is increased by $49,005. Therefore, debit Merchandise Inventory account with $49,005.

- Accounts payable is a liability and it is increased by $49,005. Therefore, credit accounts payable account with $49,005.

Working Note (5):

Calculate the amount of accounts payable.

Purchases = $49,500

Discount percentage = 1%

Record the journal entry of Company B.

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| April 12 | Accounts payable | 31,690 | ||

| Cash | 31,690 | |||

| (To record payment made in full settlement less discounts) |

Table (16)

- Accounts payable is a liability and it is decreased by $31,690. Therefore, debit accounts payable account with $31,690.

- Cash is an asset and it is decreased by $31,690. Therefore, credit cash account with $31,690.

Record the journal entry of Company B.

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| April 18 | Cash | 2,000 | ||

| Merchandise Inventory | 2,000 | |||

| (To record purchase return) |

Table (17)

- Cash is an asset and it is increased by $2,000. Therefore, debit cash account with $2,000.

- Merchandise Inventory is an asset and it is decreased by $2,000. Therefore, credit Merchandise Inventory account with $2,000.

Record the journal entry of Company B.

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| April 23 | Accounts payable | 49,005 | ||

| Cash | 49,005 | |||

| (To record payment made in full settlement less discounts) |

Table (18)

- Accounts payable is a liability and it is decreased by $49,005. Therefore, debit accounts payable account with $49,005.

- Cash is an asset and it is decreased by $49,005. Therefore, credit cash account with $49,005.

Record the journal entry of Company B.

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| April 24 | Merchandise Inventory | 67,350 | ||

| Accounts payable | 67,350 | |||

| (To record purchase on account) |

Table (19)

- Merchandise Inventory is an asset and it is increased by $67,350. Therefore, debit Merchandise Inventory account with $67,350.

- Accounts payable is a liability and it is increased by $67,350. Therefore, credit accounts payable account with $67,350.

Record the journal entry of Company B.

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| April 26 | Merchandise Inventory | 875 | ||

| Cash | 875 | |||

| (To record freight paid) |

Table (20)

- Merchandise Inventory is an asset and it is increased by $875. Therefore, debit Merchandise Inventory account with $875.

- Cash is an asset and it is decreased by $875. Therefore, credit cash account with $875.

Record the journal entry of Company B.

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| April 30 | Accounts payable | 11,300 | ||

| Merchandise Inventory | 11,300 | |||

| (To record purchase return) |

Table (21)

- Accounts payable is a liability and it is decreased by $11,300. Therefore, debit accounts payable account with $11,300.

- Merchandise Inventory is an asset and it is decreased by $11,300. Therefore, credit Merchandise Inventory account with $11,300.

Want to see more full solutions like this?

Chapter 6 Solutions

FINAN.ACCOUNTING-W/DGT ACCESS (LOOSE)

- I need help with accountingarrow_forwardMeryl Manufacturing had a Work-in-Process balance of $168,000 on January 1, 2023. The year-end balance of Work-in-Process was $192,000, and the Cost of Goods Manufactured was $745,000. Use this information to determine the total manufacturing costs incurred during the fiscal year 2023.arrow_forwardThe following is budgeted per-unit information for 2021:arrow_forward

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub