Concept explainers

Videos

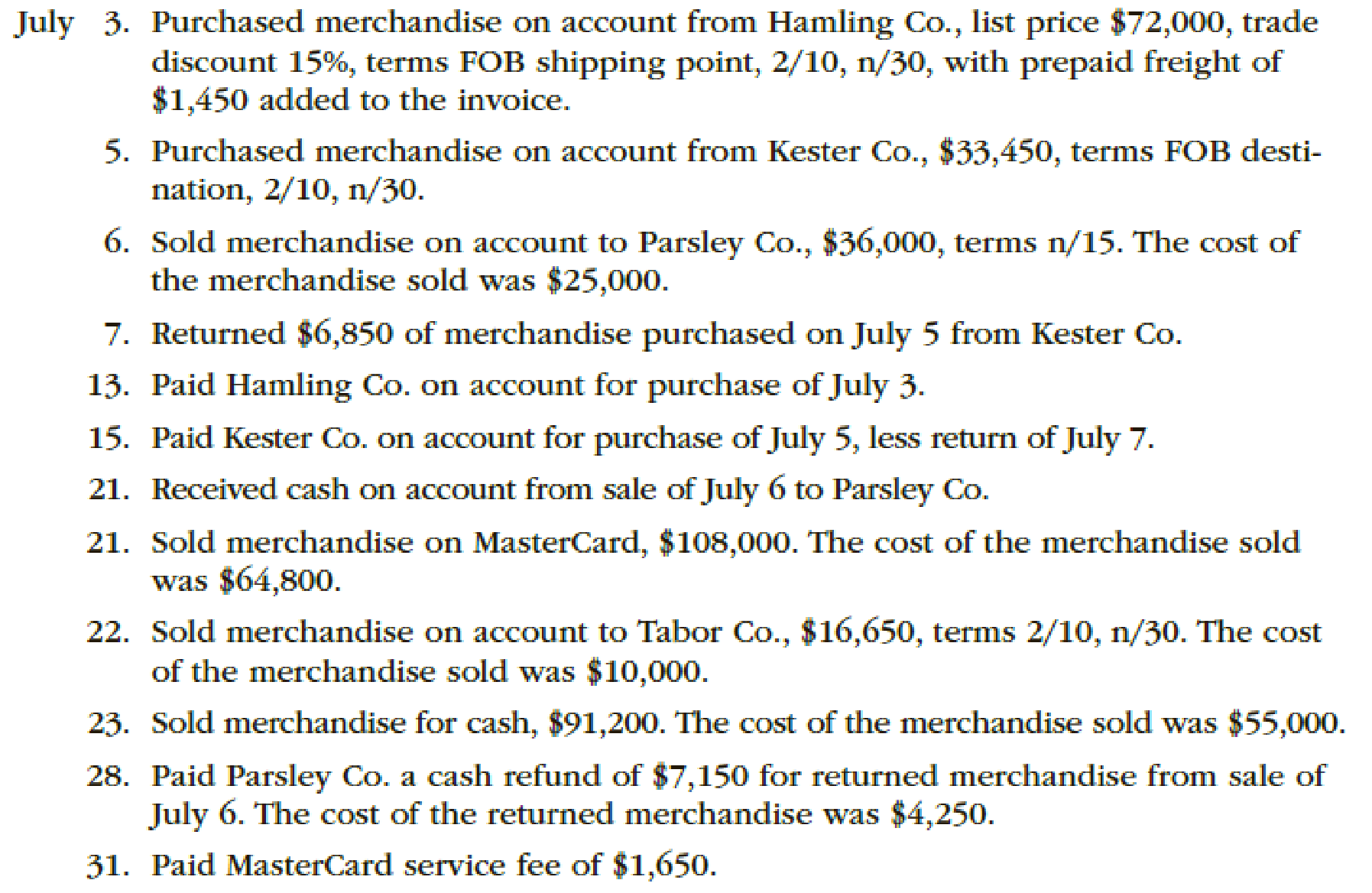

The following were selected from among the transactions completed by Essex Company during July of the current year:

Instructions

Journalize the transactions.

Prepare journal entries to record the transactions of Company E during the month of July using perpetual inventory system.

Explanation of Solution

Perpetual Inventory System refers to the Merchandise Inventory system that maintains the detailed records of every Merchandise Inventory transactions related to purchases and sales on a continuous basis. It shows the exact on-hand-merchandise inventory at any point of time.

Journal entry: Journal is the book of original entry whereby all the financial transactions are recorded in chronological order. Under this method each transaction has two sides, debit side and credit side. Total amount of debit side must be equal to the total amount of credit side. In addition, it is the primary books of accounts for any entity to record the daily transactions and processed further till the presentation of the financial statements.

The following are the rules of debit and credit:

- 1. Increase in assets and expenses accounts are debited. Decrease in liabilities and stockholders’ equity accounts are debited.

- 2. Increase in liabilities, revenues, and stockholders’ equity accounts are credited. Decreases in all asset accounts are credited.

Record the journal entry of Company E during July.

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| July 3 | Merchandise Inventory | 61,426 | ||

| Accounts payable | 61,426 (1) | |||

| (To record purchase on account) |

Table (1)

- Merchandise Inventory is an asset and it is increased by $61,426. Therefore, debit Merchandise Inventory account with $61,426.

- Accounts payable is a liability and it is increased by $61,426. Therefore, credit accounts payable account with $61,426.

Working Note (1):

Calculate the amount of accounts payable.

Purchases = $72,000

Trade discount percentage = 15%

Discount percentage = 2%

Freight = $1,450

Record the journal entry of Company E.

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| July 5 | Merchandise Inventory | 32,781 | ||

| Accounts payable | 32,781 (2) | |||

| (To record purchase on account) |

Table (2)

- Merchandise Inventory is an asset and it is increased by $32,781. Therefore, debit Merchandise Inventory account with $32,781.

- Accounts payable is a liability and it is increased by $32,781. Therefore, credit accounts payable account with $32,781.

Working Note (2):

Calculate the amount of accounts payable.

Purchases = $33,450

Discount percentage = 2%

Record the journal entry for the sale of inventory on cash.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 6 | Accounts Receivable | 36,000 | |

| Sales Revenue | 36,000 | ||

| (To record the sale of inventory on cash) |

Table (3)

- Accounts receivable is an asset and it is increased by $36,000. Therefore, debit accounts receivable with $36,000.

- Sales revenue is revenue and it increases the value of equity by $36,000. Therefore, credit sales revenue with $36,000.

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 6 | Cost of Merchandise Sold | 25,000 | |

| Merchandise Inventory | 25,000 | ||

| (To record the cost of goods sold) |

Table (4)

- Cost of merchandise sold is an expense account and it decreases the value of equity by $25,000. Therefore, debit cost of merchandise sold account with $25,000.

- Merchandise Inventory is an asset and it is decreased by $25,000. Therefore, credit inventory account with $25,000.

Record the journal entry of Company E.

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| July 7 | Accounts payable | 6,713 (3) | ||

| Merchandise Inventory | 6,713 | |||

| (To record purchase return) |

Table (5)

- Accounts payable is a liability and it is decreased by $6,713. Therefore, debit accounts payable account with $6,713.

- Merchandise Inventory is an asset and it is decreased by $6,713. Therefore, credit Merchandise Inventory account with $6,713.

Working Note (3):

Calculate the amount of accounts payable.

Purchases return = $6,850

Discount percentage = 2%

Record the journal entry of Company E.

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| July 13 | Accounts payable | 61,426 | ||

| Cash | 61,426 | |||

| (To record payment made in full settlement less discounts) |

Table (6)

- Accounts payable is a liability and it is decreased by $61,426. Therefore, debit accounts payable account with $61,426.

- Cash is an asset and it is decreased by $61,426. Therefore, credit cash account with $61,426.

Record the journal entry of Company B.

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| July 15 | Accounts payable | 26,068 (4) | ||

| Cash | 26,068 | |||

| (To record payment made in full settlement less discounts) |

Table (7)

- Accounts payable is a liability and it is decreased by $26,068. Therefore, debit accounts payable account with $26,068.

- Cash is an asset and it is decreased by $26,068. Therefore, credit cash account with $26,068.

Working Note (4):

Calculate the amount of net accounts payable.

Merchandise Inventory = $32,781 (2)

Purchase returns = $6,713 (3)

Record the journal entry for the cash receipt against accounts receivable.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 21 | Cash | 36,000 | |

| Accounts Receivable | 36,000 | ||

| (To record the receipt of cash against accounts receivables) |

Table (8)

- Cash is an asset and it is increased by $36,000. Therefore, debit cash account with $36,000.

- Accounts Receivable is an asset and it is increased by $36,000. Therefore, debit accounts receivable with $36,000.

Record the journal entry for the sale of inventory on cash.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 21 | Cash | 108,000 | |

| Sales Revenue | 108,000 | ||

| (To record the sale of inventory on cash) |

Table (9)

- Cash is an asset and it is increased by $108,000. Therefore, debit cash account with $108,000.

- Sales revenue is revenue and it increases the value of equity by $108,000. Therefore, credit sales revenue with $108,000.

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 21 | Cost of Merchandise Sold | 64,800 | |

| Merchandise Inventory | 64,800 | ||

| (To record the cost of goods sold) |

Table (10)

- Cost of merchandise sold is an expense account and it decreases the value of equity by $64,800. Therefore, debit cost of merchandise sold account with $64,800.

- Merchandise Inventory is an asset and it is decreased by $64,800. Therefore, credit inventory account with $64,800.

Record the journal entry for the sale of inventory on account.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 22 | Accounts Receivable | 16,317 (5) | |

| Sales Revenue | 16,317 | ||

| (To record the sale of inventory on account) |

Table (11)

- Accounts Receivable is an asset and it is increased by $16,317. Therefore, debit accounts receivable with $16,317.

- Sales revenue is revenue and it increases the value of equity by $16,317. Therefore, credit sales revenue with $16,317.

Working Note (5):

Calculate the amount of accounts receivable.

Sales = $16,650

Discount percentage = 2%

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 22 | Cost of Merchandise Sold | 10,000 | |

| Merchandise Inventory | 10,000 | ||

| (To record the cost of goods sold) |

Table (12)

- Cost of merchandise sold is an expense account and it decreases the value of equity by $10,000. Therefore, debit cost of merchandise sold account with $10,000.

- Merchandise Inventory is an asset and it is decreased by $10,000. Therefore, credit inventory account with $10,000.

Record the journal entry for the sale of inventory on cash.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 23 | Cash | 91,200 | |

| Sales Revenue | 91,200 | ||

| (To record the sale of inventory on cash) |

Table (13)

- Cash is an asset and it is increased by $91,200. Therefore, debit cash account with $91,200.

- Sales revenue is revenue and it increases the value of equity by $91,200. Therefore, credit sales revenue with $91,200.

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 23 | Cost of Merchandise Sold | 55,000 | |

| Merchandise Inventory | 55,000 | ||

| (To record the cost of goods sold) |

Table (14)

- Cost of merchandise sold is an expense account and it decreases the value of equity by $55,000. Therefore, debit cost of merchandise sold account with $55,000.

- Merchandise Inventory is an asset and it is decreased by $55,000. Therefore, credit inventory account with $55,000.

Record the journal entry for sales return.

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| July 28 | Customer Refunds Payable | 7,150 | ||

| Cash | 7,150 | |||

| (To record sales returns) |

Table (15)

- Customer refunds payable is a liability account and it is decreased by $7,150. Therefore, debit customer refunds payable account with $7,150.

- Accounts Receivable is an asset and it is decreased by $7,150. Therefore, credit account receivable with $7,150.

Record the journal entry for the return of the merchandise.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 28 | Merchandise Inventory | 4,250 | |

| Estimated Returns Inventory | 4,250 | ||

| (To record the return of the merchandise) |

Table (16)

- Merchandise Inventory is an asset and it is increased by $4,250. Therefore, debit inventory account with $4,250.

- Estimated returns inventory is an expense account and it increases the value of equity by $4,250. Therefore, credit estimated returns inventory account with $4,250.

Record the journal entry for credit card expense.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 31 | Credit card expense | 1,650 | |

| Cash | 1,650 | ||

| (To record the payment of credit card expenses) |

Table (17)

- Credit card expense is an expense account and it decreases the value of equity by $1,650. Therefore, debit credit card expense account with $1,650.

- Cash is an asset and it is decreased by $1,650. Therefore, credit cash account with $1,650.

Want to see more full solutions like this?

Chapter 6 Solutions

Financial Accounting

- I need help solving this general accounting question with the proper methodology.arrow_forwardI need help solving this general accounting question with the proper methodology.arrow_forwardI am looking for the correct answer to this general accounting question with appropriate explanations.arrow_forward

- I am looking for the correct answer to this general accounting question with appropriate explanations.arrow_forwardCan you explain the correct methodology to solve this general accounting problem?arrow_forwardCan you help me solve this general accounting problem using the correct accounting process?arrow_forward

- Please help me solve this general accounting question using the right accounting principles.arrow_forwardPlease provide the answer to this general accounting question with proper steps.arrow_forwardPlease provide the accurate answer to this general accounting problem using valid techniques.arrow_forward

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

College Accounting (Book Only): A Career ApproachAccountingISBN:9781305084087Author:Cathy J. ScottPublisher:Cengage Learning

College Accounting (Book Only): A Career ApproachAccountingISBN:9781305084087Author:Cathy J. ScottPublisher:Cengage Learning