Concept explainers

Videos

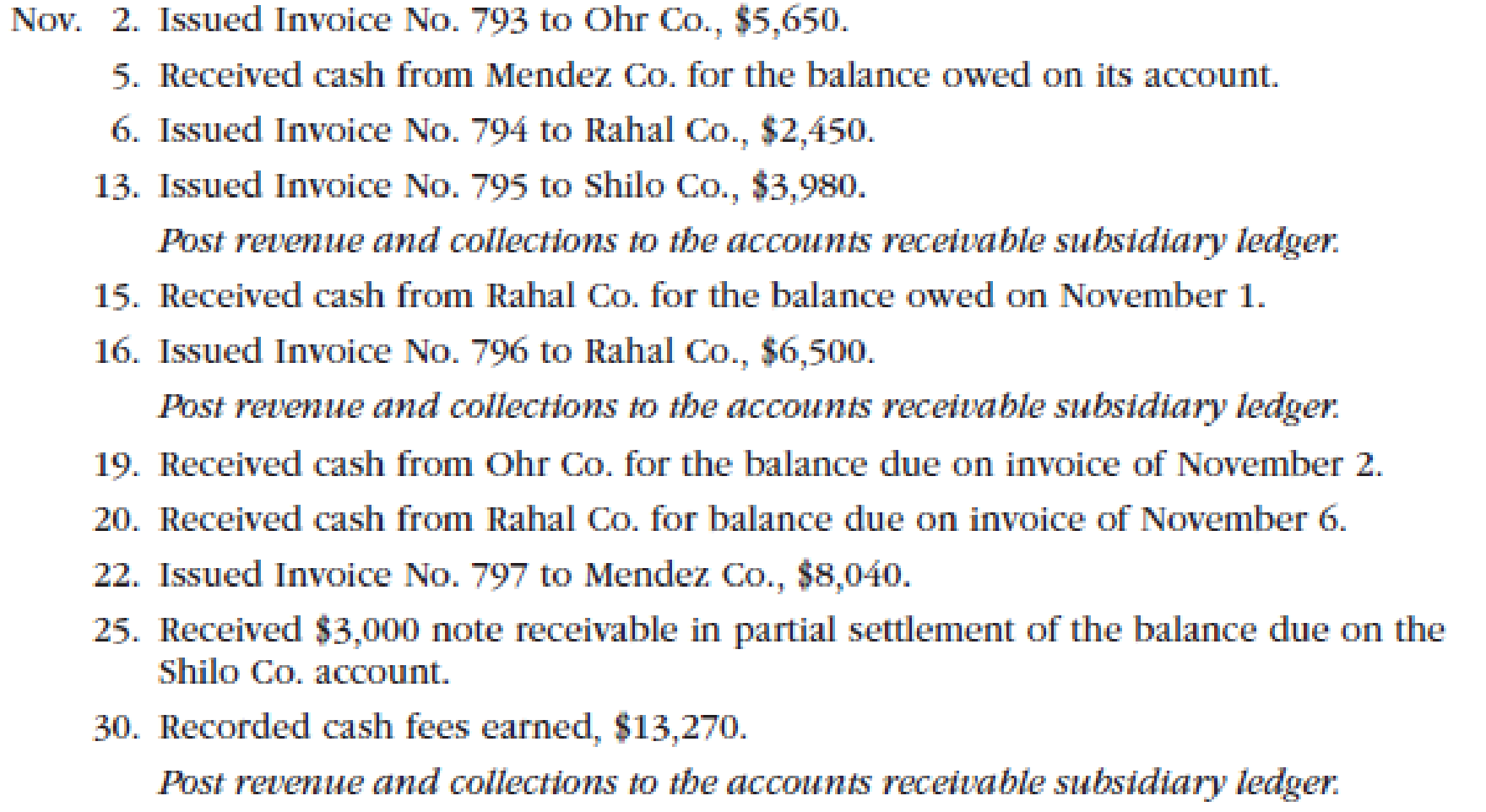

Transactions related to revenue and cash receipts completed by Albany Architects Co. during the period November 2–30, 2016, are as follows:

Instructions

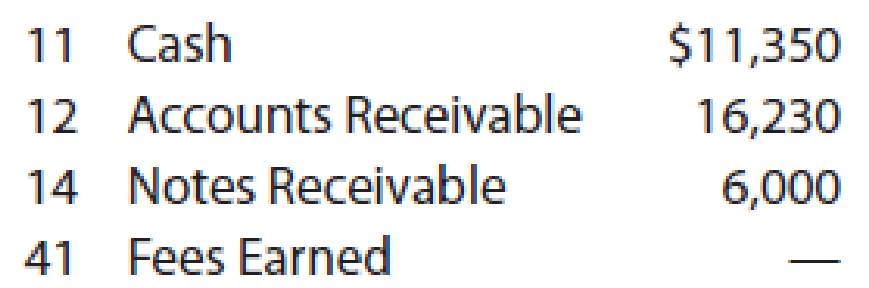

- 1. Insert the following balances in the general ledger as of November 1:

- 2. Insert the following balances in the

accounts receivable subsidiary ledger as of November 1:

- 3. Prepare a single-column revenue journal (p. 40) and a cash receipts journal (p. 36). Use the following column headings for the cash receipts journal: Fees Earned Cr., Accounts Receivable Cr., and Cash Dr. The Fees Earned column is used to record cash fees. Insert a check mark (✓) in the Post. Ref. column when recording cash fees.

- 4. Using the two special journals and the two-column general journal (p. 1), journalize the transactions for November. Post to the accounts receivable subsidiary ledger, and insert the balances at the points indicated in the narrative of transactions. Determine the balance in the customer’s account before recording a cash receipt.

- 5. Total each of the columns of the special journals, and

post the individual entries and totals to the general ledger. Insert account balances after the last posting. - 6. Determine that the sum of the customer balances agrees with the accounts receivable controlling account in the general ledger.

- 7. Why would an automated system omit postings to a controlling account as performed in step 5 for Accounts Receivable?

1. and 5.

Prepare general ledger for given accounts.

Explanation of Solution

General Ledger: General ledger refers to the ledger that records all the transactions of the business related to the company’s assets, liabilities, owners’ equities, revenues and expenses. Each subsidiary ledger is represented in the general ledger by summarizing the account.

Accounts receivable subsidiary ledger: Account receivable subsidiary ledger is the ledger which is used to post the customer transaction in one particular ledger account. It helps the business for locate the error in the customer ledger balance. After all transactions are posted, the balances in the accounts receivable subsidiary ledger should be totaled, and compare with the balance in the general ledger of accounts receivable. If both the balance does not agree, the error has been located and corrected.

Revenue journal: Revenue journal refers to the journal that is used to record the fees earned on account. In the revenue journal, all revenue transactions are recorded only when the business performed service to customer on account (credit).

Cash receipts journal: Cash receipts journal refers to the journal that is used to record the all transaction which is involve the cash receipts. For example, the business received cash from customer (service performed in cash).

Prepare the general ledger for given accounts as follows:

| Account: Cash Account no. 11 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| NOV | 1 | Balance | ✓ | 11,350 | |||

| 30 | CR36 | 37,600 | 48,950 | ||||

Table (1)

| Account: Accounts Receivable Account no. 12 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| NOV | 1 | Balance | ✓ | 16,230 | |||

| 25 | J1 | 3,000 | 13,230 | ||||

| 30 | R40 | 26,620 | 39,850 | ||||

| 30 | CR36 | 24,330 | 15,520 | ||||

Table (2)

| Account: Notes Receivable Account no. 14 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| NOV | 1 | Balance | ✓ | 6,000 | |||

| 25 | J1 | 3,000 | 9,000 | ||||

Table (3)

| Account: Fees earned Account no. 41 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| NOV | 30 | Balance | R40 | 26,620 | 26,620 | ||

| 30 | CR36 | 13,270 | 39,890 | ||||

Table (4)

| Journal Page 01 | |||||

| Date | Description | Post. Ref | Debit ($) | Credit ($) | |

| NOV | 25 | Notes receivable | 14 | 3,000 | |

| Accounts receivable | 12 | 3,000 | |||

| (To record payable note raised against the accounts receivable from customer Company S) | |||||

Table (5)

2. and 4.

Prepare accounts receivable subsidiary ledger for given customers.

Explanation of Solution

The accounts receivable subsidiary ledger for given customers are as follows:

Accounts receivable subsidiary ledger

| Name: Company M | ||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) |

Balance ($) | |

| 2016 | ||||||

| NOV | 1 | Balance | ✓ | 9,4608 | ||

| 5 | CR36 | 9,460 | - | |||

| 22 | R40 | 8,040 | 8,040 | |||

Table (6)

| Name: Company O | ||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) |

Balance ($) | |

| 2016 | ||||||

| NOV | 2 | R40 | 5,650 | 5,650 | ||

| 19 | CR36 | 5,650 | - | |||

Table (7)

| Name: Company R | ||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) |

Balance ($) | |

| 2016 | ||||||

| NOV | 1 | Balance | ✓ | 6,770 | ||

| 6 | R40 | 2,450 | 9,220 | |||

| 15 | CR36 | 6,770 | 2,450 | |||

| 16 | R40 | 6,500 | 8,950 | |||

| 20 | CR36 | 2,450 | 6,500 | |||

Table (8)

| Name: Company S | ||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) |

Balance ($) | |

| 2016 | ||||||

| NOV | 13 | R40 | 3,980 | 3,980 | ||

| 25 | J1 | 3,000 | 980 | |||

Table (9)

3.

Prepare single column revenue journal and cash receipt journal.

Explanation of Solution

Revenue journal

Revenue journal of C Business service in the month of November 2016 is as follows:

Revenue journal

Page 40

| Date | Invoice No. | Account debited | Post Ref. |

Account receivable Dr. Fees earned Cr. ($) | |

| 2016 | |||||

| NOV | 2 | 793 | Company O | ✓ | 5,650 |

| 6 | 794 | Company R | ✓ | 2,450 | |

| 13 | 795 | Company S | ✓ | 3,980 | |

| 16 | 796 | Company R | ✓ | 6,500 | |

| 22 | 797 | Company M | ✓ | 8,040 | |

| 30 | $26,620 | ||||

| (12) (41) | |||||

Table (10)

Cash receipt journal

Cash receipt journal of C Business service in the month of November, 2016 is as follows:

Cash receipt journal

Page 36

| Date | Account Credited | Post Ref. | Fees earned Cr. | Accounts receivable Cr. | Cash Dr. | |

| 2016 | ||||||

| NOV | 5 | Company M | ✓ | 9,460 | 9,460 | |

| 15 | Company R | ✓ | 6,770 | 6,770 | ||

| 19 | Company O | ✓ | 5,650 | 5,650 | ||

| 20 | Company R | ✓ | 2,450 | 2,450 | ||

| 30 | Fees earned | 13,270 | 13,270 | |||

| 30 | 13,270 | 24,330 | 37,600 | |||

| (41) | (12) | (11) | ||||

Table (11)

6.

Prepare accounts receivable customers balance, and verify that the total agrees with the ending balance of accounts receivable control account.

Explanation of Solution

Accounts receivable customer balance

Accounts receivable customers balance is as follows:

| C Business service | |

| Accounts receivable customers balances | |

| NOV 30 | |

| Amount ($) | |

| Company M | 8,040 |

| Company R | 6,500 |

| Company S | 980 |

| Total accounts receivable | 15,520 |

Table (12)

Accounts receivable controlling account

Ending balance of accounts receivable controlling account is as follows:

| C Business service | |

| Accounts receivable (Controlling account) | |

| NOV 30 | |

| Amount ($) | |

| Opening balance on NOV 1 | 16,230 |

| Add: | |

| Total debits (from revenue journal) | 26,620 |

| Less: | |

| Total credits (from cash receipts journal and journal) (1) | (27,330) |

| Total accounts receivable | 15,520 |

Table (13)

Working note: Calculate the total credits in the accounts receivable

In this case, accounts receivable subsidiary ledger is used to identify and locate the error by way of cross check the customer balance and accounts receivable controlling account. From the above calculation, we can understand that the both balance of accounts receivable is agree, hence there is no error in the recording and posing of transactions.

7.

Discuss reason of an automated system omit to posting a controlling accounting system.

Explanation of Solution

At the time of the original transactions are entered, the individual sales transactions are posted automatically in the computer system. So, there is no need to post the summary totals to the general ledger accounts.

Want to see more full solutions like this?

Chapter 5 Solutions

Financial Accounting

- Accounting Problem [5 Points]: Mona's TVs has current liabilities of $26.7 million. Cash makes up 41 percent of the current assets and accounts receivable make up another 13 percent of current assets. Mona's current ratio = 1.06 times. What is the value of inventory listed on the firm's balance sheet?arrow_forwardHelparrow_forwardAt the beginning of the recent period there were 1,440 units of product in a department, one-half completed. These units were finished and an additional 6,850 units were started and completed during the period. 1,260 units were still in process at the end of the period, one-fifth completed. Using the weighted-average valuation method the equivalent units produced by the department were ____ units.arrow_forward

- I am looking for help with this general accounting question using proper accounting standards.arrow_forwardI need the correct answer to this financial accounting problem using the standard accounting approach.arrow_forwardBurlington Audio Works was organized on January 3, 2016. During 2018, Burlington Audio issued 30,000 shares at $18 per share, purchased 5,000 shares of treasury stock at $20 per share, and had a net income of $210,000. What is the total amount of stockholders' equity at December 31, 2018?arrow_forward

- Please provide the correct answer to this general accounting problem using accurate calculations.arrow_forwardComputer the increase in net income Baldwin will realize by accepting the special order ,assuming the company has sufficient excess operating capity.arrow_forwardI need assistance with this general accounting question using appropriate principles.arrow_forward

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage