2. Net income, $185,000 Appendix 2 PR 5-10A Periodic inventory accounts, multiple-step income statement, closing entries On December 31, 20Y5, the balances of the accounts appearing in the ledger of Wyman Company are as follows: Instructions 1. Does Wyman Company use a periodic or perpetual inventory system? Explain. 2. Prepare a multiple-step income statement for Wyman Company for the year ended December 31, 20Y5. The inventory as of December 31, 20Y5, was $305,000. The estimated cost of customer returns inventory for December 31, 20Y5, is estimated to increase to $40,000. 3. Prepare the closing entries for Wyman Company as of December 31, 20Y5. 4. What would be the net income if the perpetual inventory system had been used?

2. Net income, $185,000 Appendix 2 PR 5-10A Periodic inventory accounts, multiple-step income statement, closing entries On December 31, 20Y5, the balances of the accounts appearing in the ledger of Wyman Company are as follows: Instructions 1. Does Wyman Company use a periodic or perpetual inventory system? Explain. 2. Prepare a multiple-step income statement for Wyman Company for the year ended December 31, 20Y5. The inventory as of December 31, 20Y5, was $305,000. The estimated cost of customer returns inventory for December 31, 20Y5, is estimated to increase to $40,000. 3. Prepare the closing entries for Wyman Company as of December 31, 20Y5. 4. What would be the net income if the perpetual inventory system had been used?

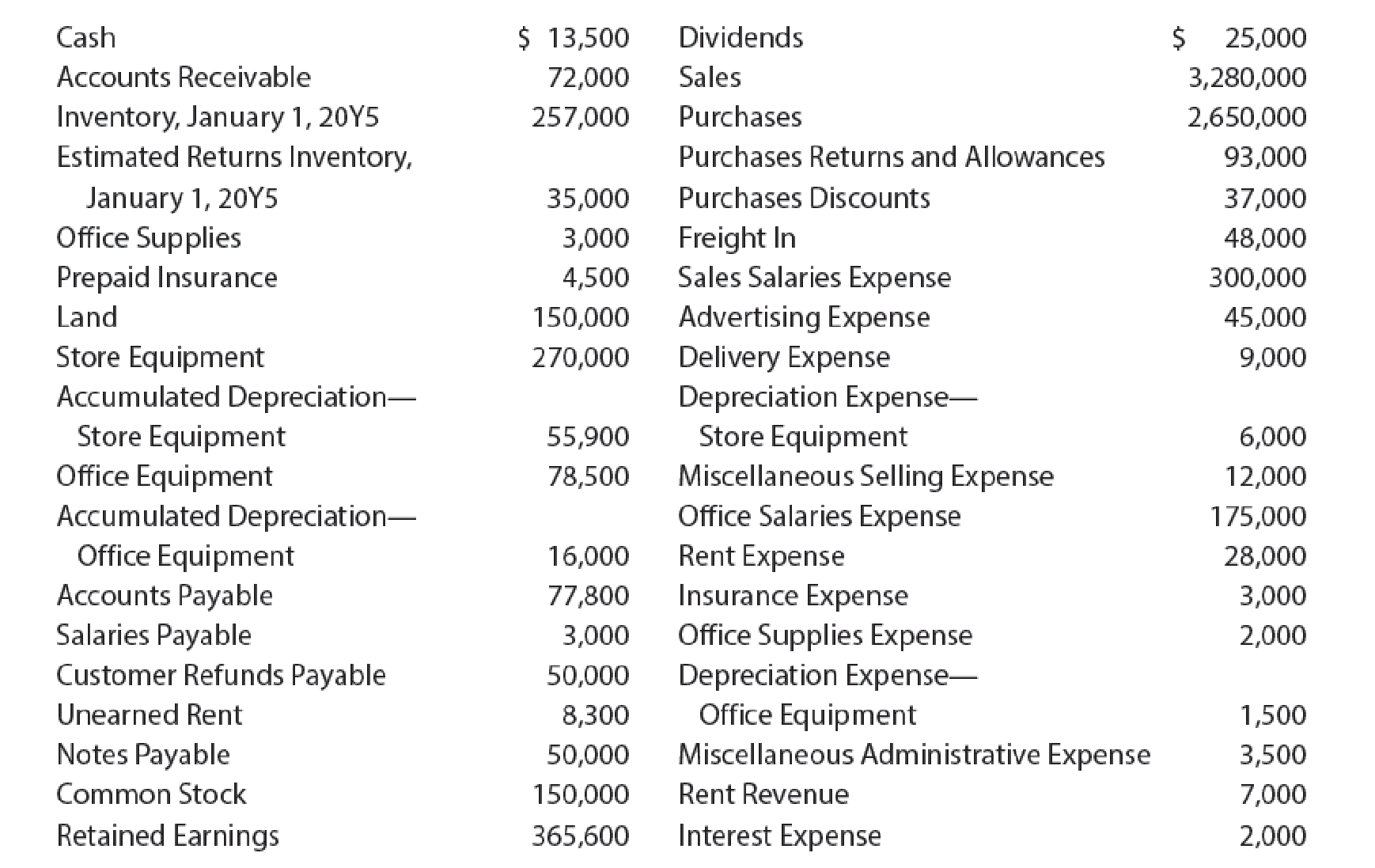

PR 5-10A Periodic inventory accounts, multiple-step income statement, closing entries

On December 31, 20Y5, the balances of the accounts appearing in the ledger of Wyman Company are as follows:

Instructions

1. Does Wyman Company use a periodic or perpetual inventory system? Explain.

2. Prepare a multiple-step income statement for Wyman Company for the year ended December 31, 20Y5. The inventory as of December 31, 20Y5, was $305,000. The estimated cost of customer returns inventory for December 31, 20Y5, is estimated to increase to $40,000.

3. Prepare the closing entries for Wyman Company as of December 31, 20Y5.

4. What would be the net income if the perpetual inventory system had been used?

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.

Accounting for Merchandising Operations Recording Purchases of Merchandise; Author: Socrat Ghadban;https://www.youtube.com/watch?v=iQp5UoYpG20;License: Standard Youtube License

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning

Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning

College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning