Concept explainers

Videos

Complete accounting cycle

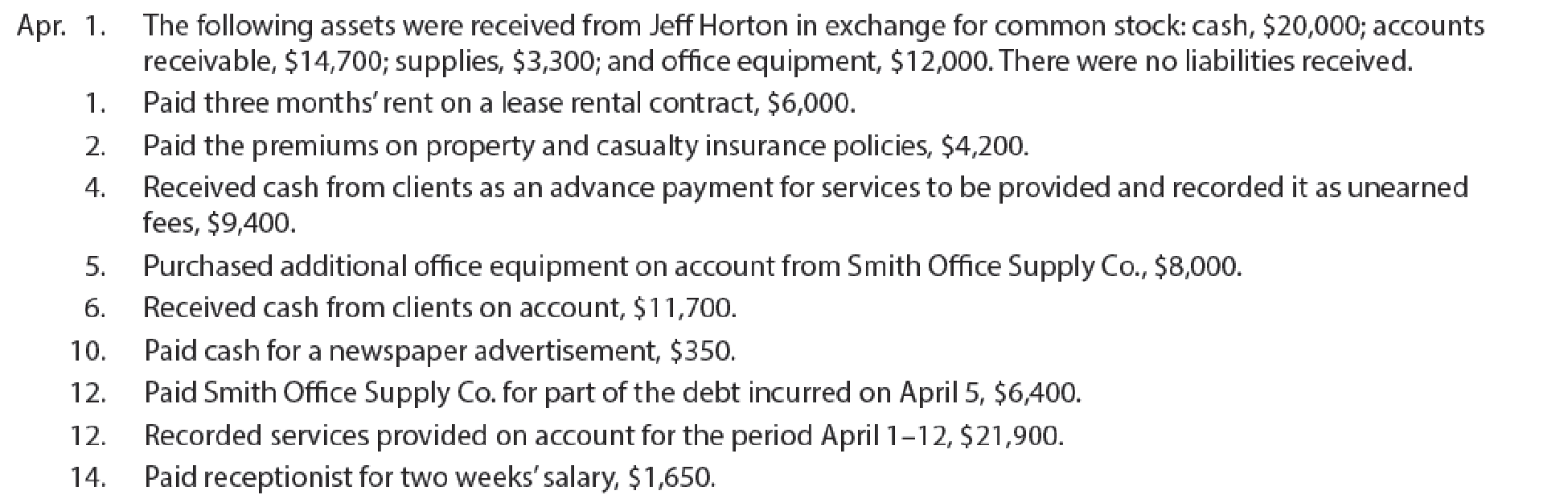

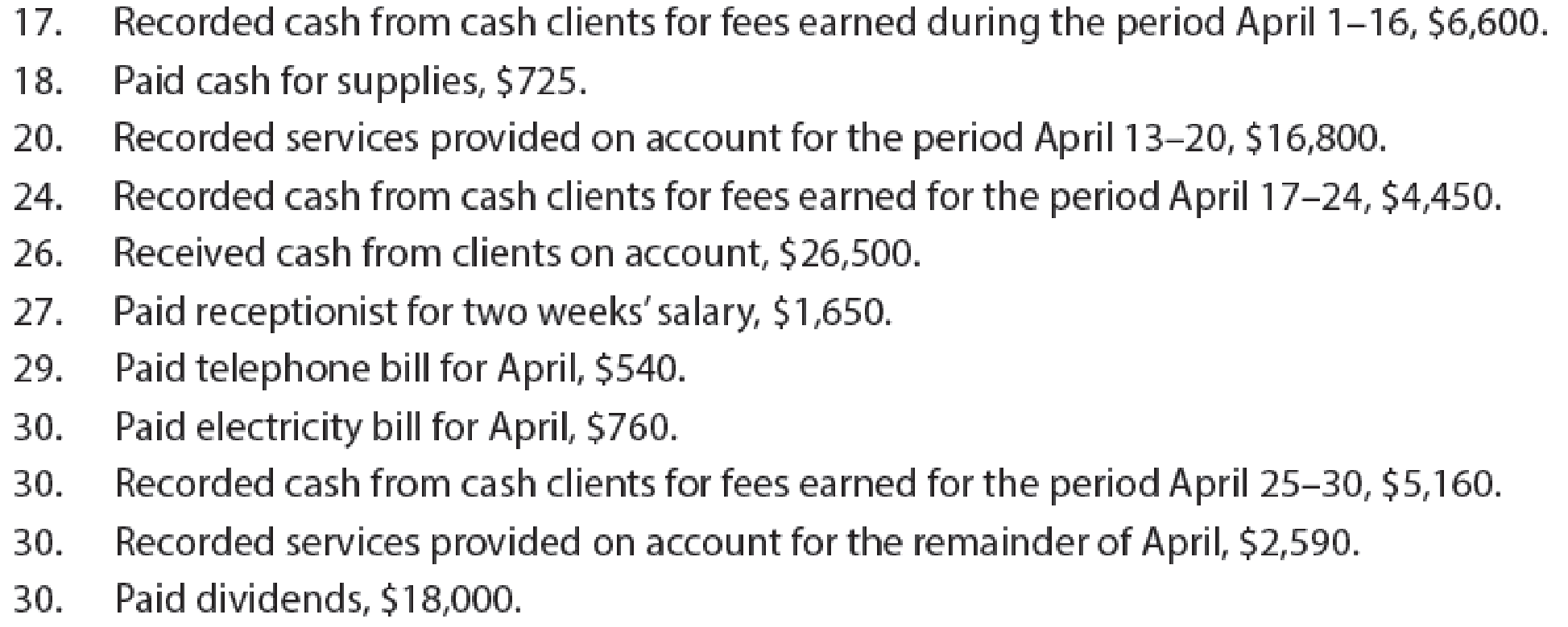

For the past several years, Jeff Horton has operated a part-time consulting business from his home. As of April 1, 20Y6, Jeff decided to move to rented quarters and to operate the business, which was to be known as Rosebud Consulting, on a full-time basis. Rosebud entered into the following transactions during April:

Record the following transactions on Page 2 of the journal:

Instructions

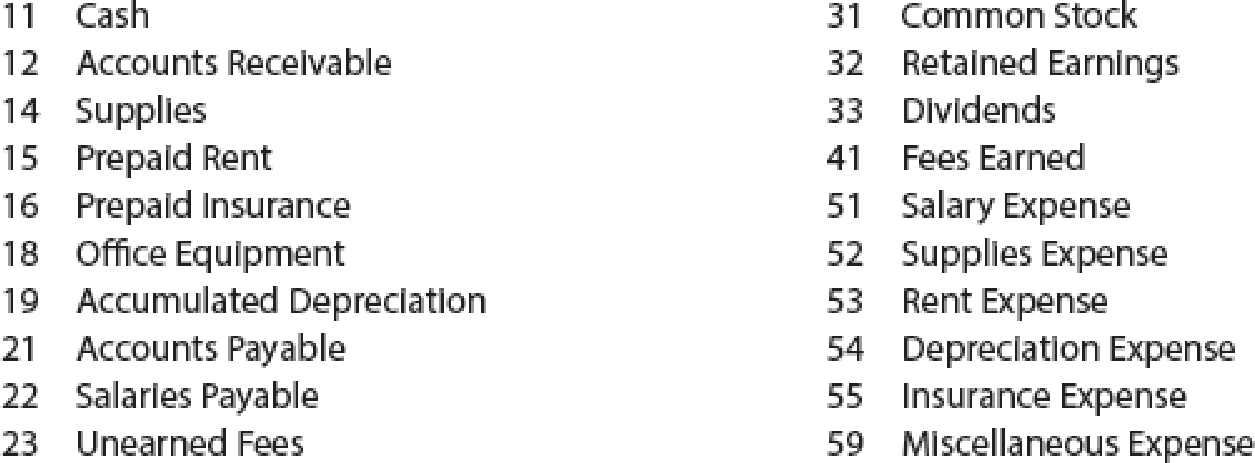

- 1. Journalize each transaction in a two-column journal starting on Page 1, referring to the following chart of accounts in selecting the accounts to be debited and credited. (Do not insert the account numbers in the journal at this time.)

- 2. Post the journal to a ledger of four-column accounts.

- 3. Prepare an unadjusted

trial balance . - 4. At the end of April, the following adjustment data were assembled. Analyze and use these data to complete parts (5) and (6).

- (a) Insurance expired during April is $350.

- (b) Supplies on hand on April 30 are $1,225.

- (c)

Depreciation of office equipment for April is $400. - (d) Accrued receptionist salary on April 30 is $275.

- (e) Rent expired during April is $2,000.

- (f) Unearned fees on April 30 are $2,350.

- 5. (Optional) Enter the unadjusted trial balance on an end-of-period spreadsheet and complete the spreadsheet.

- 6. Journalize and post the

adjusting entries . Record the adjusting entries on Page 3 of the journal. - 7. Prepare an adjusted trial balance.

- 8. Prepare an income statement, a statement of stockholders’ equity, and a balance sheet.

- 9. Prepare and

post the closing entries. Record the closing entries on Page 4 of the journal. Indicate closed accounts by inserting a line in both the Balance columns opposite the closing entry. - 10. Prepare a post-closing trial balance.

1 and 2.

Journalize the transactions of April in a two column journal beginning on page 1 and the following in page 2.

Explanation of Solution

Journal entry: Journal entry is a set of economic events which can be measured in monetary terms. These are recorded chronologically and systematically.

Journalize the transactions of April in a two column journal beginning on page 1.

| Journal Page 1 | |||||

| Date | Description | Post. Ref | Debit ($) | Credit ($) | |

| 20Y6 | Cash | 11 | 20,000 | ||

| April | 1 | Accounts receivable | 12 | 14,700 | |

| Supplies | 14 | 3,300 | |||

| Office equipment | 18 | 12,000 | |||

| Common stock | 31 | 50,000 | |||

| (To record the receipt of assets) | |||||

| 1 | Prepaid Rent | 15 | 6,000 | ||

| Cash | 11 | 6,000 | |||

| (To record the payment of rent) | |||||

| 2 | Prepaid insurance | 16 | 4,200 | ||

| Cash | 11 | 4,200 | |||

| (To record the payment of insurance premium) | |||||

| 4 | Cash | 11 | 9,400 | ||

| Unearned fees | 23 | 9,400 | |||

| (To record the cash received for the service yet to be provide) | |||||

| 5 | Office equipment | 18 | 8,000 | ||

| Accounts payable | 21 | 8,000 | |||

| (To record the purchase of supplies of account) | |||||

| 6 | Cash | 11 | 11,700 | ||

| Accounts receivable | 12 | 11,700 | |||

| (To record the cash received from clients) | |||||

| 10 | Miscellaneous expense | 59 | 350 | ||

| Cash | 11 | 350 | |||

| (To record the payment made for Miscellaneous expense) | |||||

| 12 | Accounts payable | 21 | 6,400 | ||

| Office supplies | 11 | 6,400 | |||

| (To record the payment made to creditors on account) | |||||

| 12 | Accounts receivable | 12 | 21,900 | ||

| Fees earned | 41 | 21,900 | |||

| (To record the revenue earned and billed) | |||||

| 14 | Salary Expense | 51 | 1,650 | ||

| Cash | 11 | 1,650 | |||

| (To record the payment made for salary) | |||||

Table (1)

| Journal Page 2 | |||||

| Date | Description | Post. Ref | Debit ($) | Credit ($) | |

| 20Y6 | Cash | 11 | 6,600 | ||

| April | 17 | Fees earned | 41 | 6,600 | |

| (To record the receipt of cash) | |||||

| 18 | Supplies | 14 | 725 | ||

| Cash | 11 | 725 | |||

| (To record the payment made for automobile expense) | |||||

| 20 | Accounts receivable | 12 | 16,800 | ||

| Fees earned | 41 | 16,800 | |||

| (To record the payment of advertising expense) | |||||

| 24 | Cash | 11 | 4,450 | ||

| Fees earned | 41 | 4,450 | |||

| (To record the cash received from client for fees earned) | |||||

| 26 | Cash | 11 | 26,500 | ||

| Accounts receivable | 12 | 26,500 | |||

| (To record the cash received from clients) | |||||

| 27 | Salary expense | 51 | 1,650 | ||

| Cash | 11 | 1,650 | |||

| (To record the payment of salary) | |||||

| 29 | Miscellaneous Expense | 59 | 540 | ||

| Cash | 11 | 540 | |||

| (To record the payment of telephone charges) | |||||

| 31 | Miscellaneous Expense | 59 | 760 | ||

| Cash | 11 | 760 | |||

| (To record the payment of electricity charges) | |||||

| 31 | Cash | 11 | 5,160 | ||

| Fees earned | 41 | 5,160 | |||

| (To record the cash received from client for fees earned) | |||||

| 31 | Accounts receivable | 12 | 2,590 | ||

| Fees earned | 41 | 2,590 | |||

| (To record the revenue earned and billed) | |||||

| 31 | Dividends | 33 | 18,000 | ||

| Cash | 11 | 18,000 | |||

| (To record the dividends made for personal use) | |||||

Table (2)

2, 6 and 9.

Record the balance of each account in the appropriate balance column of a four-column account and post them to the ledger.

Explanation of Solution

T-account: The condensed form of a ledger is referred to as T-account. The left-hand side of this account is known as debit, and the right hand side is known as credit.

| Account: Cash Account no. 11 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y6 | |||||||

| April | 1 | 1 | 20,000 | 20,000 | |||

| 1 | 1 | 6,000 | 14,000 | ||||

| 2 | 1 | 4,200 | 9,800 | ||||

| 4 | 1 | 9,400 | 19,200 | ||||

| 6 | 1 | 11,700 | 30,900 | ||||

| 10 | 1 | 350 | 30,550 | ||||

| 12 | 1 | 6,400 | 24,150 | ||||

| 14 | 1 | 1,650 | 22,500 | ||||

| 17 | 2 | 6,600 | 29,100 | ||||

| 18 | 2 | 725 | 28,375 | ||||

| 24 | 2 | 4,450 | 32,825 | ||||

| 26 | 2 | 26,500 | 59,325 | ||||

| 27 | 2 | 1,650 | 57,675 | ||||

| 29 | 2 | 540 | 57,135 | ||||

| 31 | 2 | 760 | 56,375 | ||||

| 31 | 2 | 5,160 | 61,535 | ||||

| 31 | 2 | 18,000 | 43,535 | ||||

Table (3)

| Account: Accounts Receivable Account no. 12 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y6 | |||||||

| April | 1 | 1 | 14,700 | 14,700 | |||

| 6 | 1 | 11,700 | 3,000 | ||||

| 12 | 1 | 21,900 | 24,900 | ||||

| 20 | 2 | 16,800 | 41,700 | ||||

| 26 | 2 | 26,500 | 15,200 | ||||

| 31 | 2 | 2,590 | 17,790 | ||||

Table (4)

| Account: Supplies Account no. 14 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y6 | |||||||

| April | 1 | 1 | 3,300 | 3,300 | |||

| 18 | 2 | 725 | 4,025 | ||||

| 31 | Adjusting | 3 | 2,800 | 1,225 | |||

Table (5)

| Account: Prepaid Rent Account no. 15 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y6 | |||||||

| April | 1 | 1 | 6,000 | 6,000 | |||

| 31 | Adjusting | 3 | 2,000 | 4,000 | |||

Table (6)

| Account: Prepaid Insurance Account no. 16 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y6 | |||||||

| April | 2 | 1 | 4,200 | 4,200 | |||

| 31 | Adjusting | 3 | 350 | 3,850 | |||

Table (7)

| Account: Office equipment Account no. 18 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y6 | |||||||

| April | 1 | 1 | 12,000 | 12,000 | |||

| 5 | 1 | 8,000 | 20,000 | ||||

Table (8)

| Account: Accumulated Depreciation-Office equipment Account no. 19 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y6 | |||||||

| April | 31 | Adjusting | 3 | 400 | 400 | ||

Table (9)

| Account: Accounts Payable Account no. 21 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y6 | |||||||

| April | 5 | 1 | 8,000 | 8,000 | |||

| 12 | 1 | 6,400 | 1,600 | ||||

Table (10)

| Account: Salaries Payable Account no. 22 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y6 | |||||||

| April | 31 | Adjusting | 3 | 275 | 275 | ||

Table (11)

| Account: Unearned Fees Account no. 23 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y6 | |||||||

| April | 4 | 1 | 9,400 | 9,400 | |||

| 31 | Adjusting | 3 | 7,050 | 2,350 | |||

Table (12)

| Account: Common Stock Account no. 31 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y6 | |||||||

| April | 1 | 1 | 50,000 | 50,000 | |||

Table (13)

| Account: Retained earnings Account no. 32 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y6 | |||||||

| April | 1 | 0 | |||||

| 31 | Closing | 4 | 53,775 | 53,775 | |||

| 31 | Closing | 4 | 18,000 | 35,775 | |||

Table (14)

| Account: Dividends Account no. 33 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y6 | |||||||

| April | 31 | 2 | 18,000 | 18,000 | |||

| 31 | Closing | 4 | 18,000 | ||||

Table (15)

| Account: Fees earned Account no. 41 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y6 | |||||||

| April | 12 | 1 | 21,900 | 21,900 | |||

| 17 | 2 | 6,600 | 28,500 | ||||

| 20 | 2 | 16,800 | 45,300 | ||||

| 24 | 2 | 4,450 | 49,750 | ||||

| 31 | 2 | 5,160 | 54,910 | ||||

| 31 | 2 | 2,590 | 57,500 | ||||

| 31 | Adjusting | 3 | 7,050 | 64,500 | |||

| 31 | Closing | 4 | 64,500 | ||||

Table (16)

| Account: Salary expense Account no. 51 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y6 | |||||||

| April | 14 | 1 | 1,650 | 1,650 | |||

| 27 | 2 | 1,650 | 3,300 | ||||

| 31 | Adjusting | 3 | 275 | 3,575 | |||

| 31 | Closing | 4 | 3,575 | ||||

Table (17)

| Account: Rent expense Account no. 52 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y6 | |||||||

| April | 31 | Adjusting | 3 | 2,000 | 2,000 | ||

| 31 | Closing | 4 | 2,000 | ||||

Table (18)

| Account: Supplies expense Account no. 53 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y6 | |||||||

| April | 31 | Adjusting | 3 | 2,800 | 2,800 | ||

| 31 | Closing | 4 | 2,800 | ||||

Table (19)

| Account: Depreciation expense Account no. 54 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y6 | |||||||

| April | 31 | Adjusting | 3 | 400 | 400 | ||

| 31 | Closing | 4 | 400 | ||||

Table (20)

| Account: Insurance expense Account no. 54 | ||||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | |||

| Debit ($) | Credit ($) | |||||||

| 20Y6 | ||||||||

| April | 31 | Adjusting | 3 | 350 | 350 | |||

| 31 | Closing | 4 | 350 | |||||

Table (21)

| Account: Miscellaneous expense Account no. 59 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y6 | |||||||

| April | 10 | 1 | 350 | 350 | |||

| 29 | 2 | 540 | 890 | ||||

| 31 | 2 | 760 | 1,650 | ||||

| 31 | Closing | 4 | 1,650 | ||||

Table (22)

3.

Prepare an unadjusted trial balance for Company.

Explanation of Solution

Unadjusted trial balance:

Unadjusted trial balance is that statement which contains complete list of accounts with their unadjusted balances. This statement is prepared at the end of every financial period.

Prepare an unadjusted trial balance for Company.

| Company RC | |||

| Unadjusted Trial Balance | |||

| As of April 31, 20Y6 | |||

| Account titles | Account No. | Debit balances | Credit balances |

| Cash | 11 | 43,535 | |

| Accounts Receivable | 12 | 17,790 | |

| Supplies | 14 | 4,025 | |

| Prepaid Rent | 15 | 6,000 | |

| Prepaid Insurance | 16 | 4,200 | |

| Office Equipment | 18 | 20,000 | |

| Accumulated Depreciation | 19 | 0 | |

| Accounts Payable | 21 | 1,600 | |

| Salaries Payable | 22 | 0 | |

| Unearned Fees | 23 | 9,400 | |

| Common Stock | 31 | 50,000 | |

| Retained Earnings | 32 | 0 | |

| Dividends | 33 | 18,000 | |

| Fees Earned | 41 | 57,500 | |

| Salary Expense | 51 | 3,300 | |

| Rent Expense | 52 | 0 | |

| Supplies Expense | 53 | 0 | |

| Depreciation Expense | 54 | 0 | |

| Insurance Expense | 55 | 0 | |

| Miscellaneous Expense | 59 | 1,650 | |

| Totals | $118,500 | $118,500 | |

Table (23)

5.

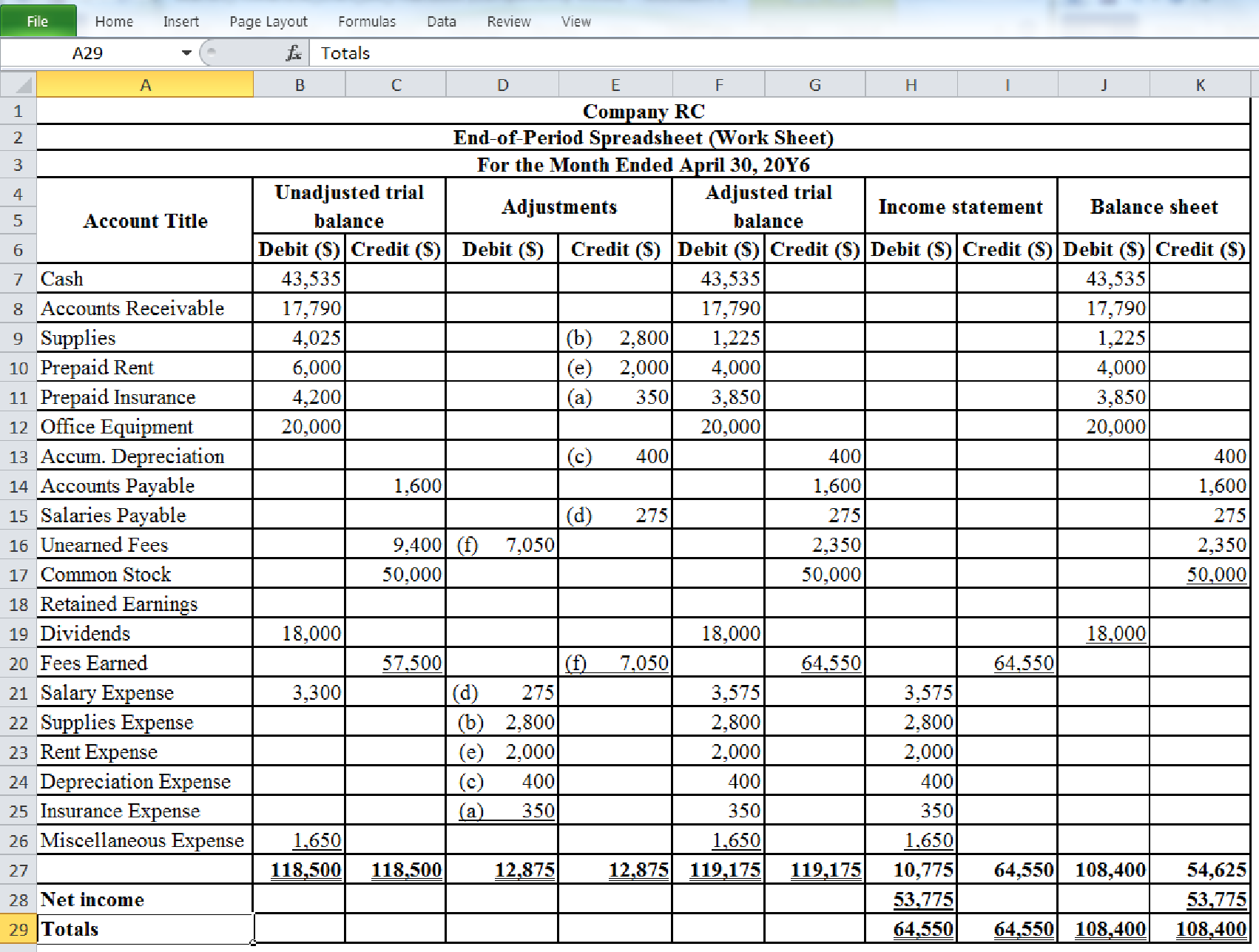

Enter the unadjusted trial balance on an end of period spreadsheet and complete the spread sheet.

Explanation of Solution

Spreadsheet: A spreadsheet is a worksheet. It is used while preparing a financial statement. It is a type of form having multiple columns and it is used in the adjustment process. The use of a worksheet is optional for any organization. A worksheet can neither be considered as a journal nor a part of the general ledger.

Prepare the end of period spreadsheet and enter the unadjusted trial balance:

Table (24)

6.

Journalize the adjusting entries of Company RC for April 31.

Explanation of Solution

Adjusting entries:

Adjusting entries refers to the entries that are made at the end of an accounting period in accordance with revenue recognition principle, and expenses recognition principle. All adjusting entries affect at least one income statement account (revenue or expense), and one balance sheet account (asset or liability).

Prepare the adjusting entries:

| Date | Accounts title and explanation | Post Ref. |

Debit ($) |

Credit ($) | |

| 20Y6 | Insurance expense | 55 | 350 | ||

| April | 31 | Prepaid insurance | 16 | 350 | |

| (To record the insurance expense for April) | |||||

| 31 | Supplies expense | 53 | 2,800 | ||

| Supplies | 14 | 2,800 | |||

| (To record the supplies expense) | |||||

| 31 | Depreciation expense | 54 | 400 | ||

| Accumulated Depreciation | 19 | 400 | |||

| (To record the depreciation and the accumulated depreciation) | |||||

| 31 | Salaries expense | 51 | 275 | ||

| Salaries payable | 22 | 275 | |||

| (To record the accrued salaries payable) | |||||

| 31 | Rent expense | 52 | 2,000 | ||

| Prepaid rent | 15 | 2,000 | |||

| (To record the rent expense for April) | |||||

| 31 | Unearned fees | 23 | 7,050 | ||

| Fees earned | 41 | 7,050 | |||

| (To record the receipt of unearned fees) | |||||

Table (25)

7.

Prepare an adjusted trial balance of Company RC for April 31, 20Y6.

Explanation of Solution

Adjusted trial balance:

Adjusted trial balance is a summary of all the ledger accounts, and it contains the balances of all the accounts after the adjustment entries are journalized, and posted.

Prepare the adjusted trial balance:

| Company RC | |||

| Adjusted Trial Balance | |||

| As of April 31, 20Y6 | |||

| Account title | Account | Debit balances ($) | Credit balances ($) |

| Cash | 11 | 43,535 | |

| Accounts Receivable | 12 | 17,790 | |

| Supplies | 14 | 1,225 | |

| Prepaid Rent | 15 | 4,000 | |

| Prepaid Insurance | 16 | 3,850 | |

| Office Equipment | 18 | 20,000 | |

| Accumulated Depreciation | 19 | 400 | |

| Accounts Payable | 21 | 1,600 | |

| Salaries Payable | 22 | 275 | |

| Unearned Fees | 23 | 2,350 | |

| Common Stock | 31 | 50,000 | |

| Retained Earnings | 32 | 0 | |

| Dividends | 33 | 18,000 | |

| Fees Earned | 41 | 64,550 | |

| Salary Expense | 51 | 3,575 | |

| Rent Expense | 52 | 2,800 | |

| Supplies Expense | 53 | 2,000 | |

| Depreciation Expense | 54 | 400 | |

| Insurance Expense | 55 | 350 | |

| Miscellaneous Expense | 59 | 1,650 | |

| Totals | $119,715 | $119,175 | |

Table (26)

8.

Prepare an income statement for the year ended April 31, 20Y6.

Explanation of Solution

Income statement: The financial statement which reports revenues and expenses from business operations and the result of those operations as net income or net loss for a particular time period is referred to as income statement.

| Company RC | ||

| Income Statement | ||

| For the year ended April 31, 20Y6 | ||

| Particulars | Amount ($) | Amount ($) |

| Revenues: | ||

| Fees Earned | 64,550 | |

| Expenses: | ||

| Salaries Expense | 3,575 | |

| Rent Expense | 2,800 | |

| Supplies Expense | 2,000 | |

| Depreciation Expense- Building | 400 | |

| Insurance Expense | 350 | |

| Miscellaneous Expense | 1,650 | |

| Total Expenses | (10,775) | |

| Net Income | 53,775 | |

Table (27)

Statement of stockholders’ equity: The statement which reports the changes in stock, paid-in capital, retained earnings, and treasury stock, during the year is referred to as statement of stockholders’ equity.

Prepare the statement of stockholders equity for the year ended April 31, 20Y6.

| Company RC | |||

| Statement of Stockholders’ Equity | |||

| For the Month Ended April 31, 20Y6 | |||

| Particulars | Common stock | Retained earnings | Total |

| Beginning balances, April 1, 20Y6 | $0 | $0 | $0 |

| Issued common stock | $50,000 | $50,000 | |

| Net income | $0 | $53,775 | $53,775 |

| Dividends | $0 | ($18,000) | ($18,000) |

| Ending balances, April 31, 20Y6 | $50,000 | $35,775 | $85,775 |

Table (28)

Balance sheet: This financial statement reports a company’s resources (assets) and claims of creditors (liabilities) and stockholders (stockholders’ equity) over those resources. The resources of the company are assets which include money contributed by stockholders and creditors. Hence, the main elements of the balance sheet are assets, liabilities, and stockholders’ equity.

Prepare the balance sheet as of April 31, 20Y6:

| Company RC | ||

| Balance Sheet | ||

| As of April 31, 20Y6 | ||

| Particulars | Amount ($) | Amount ($) |

| Assets | ||

| Current assets: | ||

| Cash | 43,535 | |

| Accounts receivable | 17,790 | |

| Supplies | 1,225 | |

| Prepaid rent | 4,000 | |

| Prepaid insurance | 3,850 | |

| Total current assets | 70,400 | |

| Property, plant, and equipment: | ||

| Office equipment | 20,000 | |

| Accumulated depreciation | (400) | |

| Total property, plant, and equipment | 19,600 | |

| Total assets | $90,000 | |

| Liabilities | ||

| Current liabilities: | ||

| Accounts payable | 1,600 | |

| Salaries payable | 275 | |

| Unearned fees | 2,350 | |

| Total liabilities | 4,225 | |

| Stockholders’ Equity | ||

| Common stock | 50,000 | |

| Retained earnings | 35,775 | |

| Total stockholders’ equity | 85,775 | |

| Total liabilities and stockholders’ equity | $90,000 | |

Table (29)

9.

Journalize the closing entries for Company RC.

Explanation of Solution

Closing entry for revenue and expense accounts:

| Date | Account title and explanation | Post. Ref. | Debit ($) | Credit ($) | |

| 20Y6 | |||||

| April | 31 | Fees Earned | 41 | 64,550 | |

| Salary Expense | 51 | 3,575 | |||

| Rent Expense | 52 | 2,800 | |||

| Supplies Expense | 53 | 2,000 | |||

| Depreciation Expense | 54 | 400 | |||

| Insurance Expense | 55 | 350 | |||

| Miscellaneous Expense | 59 | 1,650 | |||

| Retained Earnings (1) | 32 | 53,775 | |||

| (To record the closing entry for revenue and expense account to retained earnings account) | |||||

| 20Y6 | 31 | Retained Earnings | 32 | 18,000 | |

| April | Dividends | 33 | 18,000 | ||

| (To record the closing entry for dividends account) | |||||

Table (30)

Working note (1):

Calculate the amount of retained earnings account:

10.

Prepare a post–closing trial balance of D Consulting for the month ended April 31, 20Y6.

Explanation of Solution

Post-closing trial balance:

The post-closing trial balance is a summary of all ledger accounts, and it shows the debit and the credit balances after the closing entries are journalized and posted. The post-closing trial balance contains only permanent (balance sheet) accounts, and the debit and the credit balances of permanent accounts should agree.

Prepare a post–closing trial balance for the year ended April 31, 20Y6:

| Company RC | |||

| Post-Closing Trial Balance | |||

| As of April 31, 20Y6 | |||

| Account title | Account No. | Debit Balances | Credit Balances |

| Cash | 11 | 43,535 | |

| Accounts Receivable | 12 | 17,790 | |

| Supplies | 14 | 1,225 | |

| Prepaid Rent | 15 | 4,000 | |

| Prepaid Insurance | 16 | 3,850 | |

| Office Equipment | 18 | 20,000 | |

| Accumulated Depreciation | 19 | 400 | |

| Accounts Payable | 21 | 1,600 | |

| Salaries Payable | 22 | 275 | |

| Unearned Fees | 23 | 2,350 | |

| Common Stock | 31 | 50,000 | |

| Retained Earnings | 32 | 35,775 | |

| Totals | $90,400 | $90,400 | |

Table (31)

Want to see more full solutions like this?

Chapter 4 Solutions

Financial And Managerial Accounting

- Dear tutor. I mistakenly submitted blurr image please comment i will write values. please dont Solve with incorrect values otherwise unhelpful.arrow_forwardno aiWhich of the following errors will not be detected by a trial balance?A. Debiting cash instead of accounts receivableB. Recording revenue twiceC. Failing to record a transactionD. A $100 debit matched with a $100 creditarrow_forwardDon't use chatgpt Which of the following errors will not be detected by a trial balance?A. Debiting cash instead of accounts receivableB. Recording revenue twiceC. Failing to record a transactionD. A $100 debit matched with a $100 creditarrow_forward

- 7. If inventory is overstated at year-end, which of the following is true?A. Net income is understatedB. Expenses are overstatedC. Net income is overstatedD. Assets are understated i need help in this question quiarrow_forwardI need correct answer 7. If inventory is overstated at year-end, which of the following is true?A. Net income is understatedB. Expenses are overstatedC. Net income is overstatedD. Assets are understatedarrow_forwardNo chatgpt 7. If inventory is overstated at year-end, which of the following is true?A. Net income is understatedB. Expenses are overstatedC. Net income is overstatedD. Assets are understatedarrow_forward

- 7. If inventory is overstated at year-end, which of the following is true?A. Net income is understatedB. Expenses are overstatedC. Net income is overstatedD. Assets are understatedneed anarrow_forwardNo ai 7. If inventory is overstated at year-end, which of the following is true?A. Net income is understatedB. Expenses are overstatedC. Net income is overstatedD. Assets are understatedarrow_forward7. If inventory is overstated at year-end, which of the following is true?A. Net income is understatedB. Expenses are overstatedC. Net income is overstatedD. Assets are understatedarrow_forward

- I mistakenly submitted blurr image please comment i will write values. please dont Solve with incorrect values otherwise unhelpful.arrow_forwardDevelopment costs in preparing the mine $ 3,400,000 Mining equipment 159,600 Construction of various structures on site 77,900 After the minerals are removed from the mine, the equipment will be sold for an estimated residual value of $12,000. The structures will be torn down. Geologists estimate that 820,000 tons of ore can be extracted from the mine. After the ore is removed, the land will revert back to the state of New Mexico. The contract with the state requires Hecala to restore the land to its original condition after mining operations are completed in approximately four years. Management has provided the following possible outflows for the restoration costs: Cash Outflow Probability $ 620,000 40% 720,000 30% 820,000 30% Hecala’s credit-adjusted risk-free interest rate is 7%. During 2024, Hecala extracted 122,000 tons of ore from the mine. The company’s fiscal year ends on December 31. Required: Determine the amount at which Hecala will record the mine. Calculate the…arrow_forwardI mistakenly submitted blurr image please comment i will write values. please dont Solve with incorrect values otherwise unhelpful.arrow_forward

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub- Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning