Concept explainers

Videos

Ledger accounts,

The unadjusted

| Lakota Freight Co. Unadjusted Trial Balance March 31, 2018 |

|||

| Account No. | Debit Balances | Credit Balances | |

| Cash................................................ | 11 | 12,000 | |

| Supplies............................................ | 13 | 30,000 | |

| Prepaid Insurance.................................... | 14 | 3,600 | |

| Equipment.......................................... | 16 | 110,000 | |

| 17 | 25,000 | ||

| Trucks............................................... | 18 | 60,000 | |

| Accumulated Depreciation—Trucks................... | 19 | 15,000 | |

| Accounts Payable.................................... | 21 | 4,000 | |

| Common Stock...................................... | 31 | 26,000 | |

| 32 | 70,000 | ||

| Dividends........................................... | 33 | 15,000 | |

| Service Revenue..................................... | 41 | 160,000 | |

| Wages Expense...................................... | 51 | 45,000 | |

| Rent Expense........................................ | 53 | 10,600 | |

| Truck Expense....................................... | 54 | 9,000 | |

| Miscellaneous Expense............................... | 59 | 4,800 | |

| 300,000 | 300,000 | ||

The data needed to determine year-end adjustments are as follows:

(A) Supplies on hand at March 31 are $7,500.

(B) Insurance premiums expired during year are $1,800.

(C) Depreciation of equipment during year is $8,350.

(D) Depreciation of trucks during year is $6,200.

(E) Wages accrued but not paid at March 31 are $600.

Instructions

1. For each account listed in the trial balance, enter the balance in the appropriate Balance column of a four-column account and place a check mark (✓) in the Posting Reference column.

2. (Optional) Enter the unadjusted trial balance on an end-of-period spread sheet and complete the spreadsheet. Add the accounts listed in part (3) as needed.

3. Journalize and post the adjusting entries, inserting balances in the accounts affected. Record the adjusting entries on Page 26 of the journal. The following additional accounts from Lakota Freight Co.’s chart of accounts should be used: Wages Payable, 22; Supplies Expense, 52; Depreciation Expense—Equipment, 55; Depreciation Expense—Trucks, 56; Insurance Expense, 57.

4. Prepare an adjusted trial balance.

5. Prepare an income statement, a retained earnings statement, and a

6. Journalize and

7. Prepare a post-closing trial balance.

1.

Journal:

Journal is the book of original entry. Journal consists of the day-to-day financial transactions in a chronological order. The journal has two aspects; they are debit aspect and the credit aspect.

T-Accounts:

T-accounts are referred as T-account because its format represents the letter “T”. The T-accounts consists of the following:

- The title of accounts.

- The debit side (Dr) and,

- The credit side (Cr).

Adjusted trial balance:

The unadjusted trial balance is the summary of all the ledger accounts that appears on the ledger accounts before making adjusting journal entries.

Adjusting entries:

An adjusting entry is prepared when the trial balance is not up-to-date, and complete, and they are usually prepared at the end of the accounting period. This adjusting entry is essential for preparing the financial statements of the business.

Spreadsheet:

A spreadsheet is a worksheet. It is used while preparing a financial statement. It is a type of form having multiple columns and it is used in the adjustment process. The use of a worksheet is optional for any organization. A worksheet can neither be considered as a journal nor a part of the general ledger.

Statement of owners’ equity:

This statement reports the beginning owner’s equity and all the changes, which led to ending owners’ equity. Additional capital, net income from income statement is added to and drawing is deducted from beginning owner’s equity to arrive at the end result, ending owner’s equity.

Income statement:

An income statement is one of the financial statements which shows the revenues, and expenses of the company. The income statement is prepared to ascertain the net income/loss of the company, by deducting the expenses from the revenues.

Balance sheet:

A balance sheet is a financial statement consists of the assets, liabilities, and the stockholder’s equity of the company. The balance of the assets account must be equal to that of the liabilities and the stockholder’s equity account.

Closing entries:

Closing entries are recorded in order to close the temporary accounts such as incomes and expenses by transferring them to the permanent accounts. It is passed at the end of the accounting period, to transfer the final balance.

Post-Closing Trial Balance:

After passing all the journal entries and the closing entries of the permanent accounts and then further posting them to each of the respective accounts, a post-closing trial balance is prepared which consists of a list of all the permanent accounts. A post-closing trial balance serves as an evidence to prove that the balance of the permanent accounts is equal.

To prepare: The T-accounts.

Explanation of Solution

Record the transactions directly in their respective T-accounts, and determine their balances.

| Account: Cash Account no. 11 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Balance | ✓ | 12,000 | |||

| Account: Supplies Account no. 13 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Balance | ✓ | 30,000 | |||

| 31 | Adjusting | 26 | 22,500 | 7,500 | |||

| Account: Prepaid Insurance Account no. 14 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Balance | ✓ | 3,600 | |||

| 31 | Adjusting | 26 | 1,800 | 1,800 | |||

| Account: Equipment Account no. 16 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Balance | ✓ | 110,000 | |||

| Account: Accumulated Depreciation-Office equipment Account no. 17 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Balance | ✓ | 25,000 | |||

| 31 | Adjusting | 26 | 8,350 | 33,350 | |||

| Account: Trucks Account no. 18 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Balance | ✓ | 60,000 | |||

| Account: Accumulated Depreciation- Truck Account no. 19 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Balance | ✓ | 15,000 | |||

| 31 | Adjusting | 26 | 6,200 | 21,200 | |||

| Account: Accounts Payable Account no. 21 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Balance | ✓ | 4,000 | |||

| Account: Wages Payable Account no. 22 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Adjusting | 26 | 600 | 600 | ||

| Account: Common Stock Account no. 31 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Balance | ✓ 1 | 26,000 | 26,000 | ||

| Account: Retained Earnings Account no. 32 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Balance | ✓ | 70,000 | |||

| 31 | Closing | 27 | 51,150 | 121,150 | |||

| 31 | Closing | 27 | 15,000 | 106,150 | |||

| Account: Dividends Account no. 33 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Balance | ✓ 1 | 15,000 | |||

| 31 | Closing | 27 | 15,000 | ||||

| Account: Income Summary Account no. 34 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Closing | 27 | 160,000 | 160,000 | ||

| 31 | Closing | 27 | 108,850 | 51,150 | |||

| 31 | Closing | 27 | 51,150 | ||||

| Account: Service revenue Account no. 41 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Balance | ✓ | 160,000 | |||

| 31 | Closing | 27 | 160,000 | ||||

| Account: Wages expense Account no. 51 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Balance | ✓ | 45,000 | |||

| 31 | Adjusting | 26 | 600 | 45,600 | |||

| 31 | Closing | 27 | 45,600 | ||||

| Account: Supplies Expense Account no. 52 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Adjusting | 26 | 22,500 | 22,500 | ||

| 31 | Closing | 27 | 22,500 | ||||

| Account: Rent expense Account no. 53 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Balance | ✓ | 10,600 | |||

| 31 | Closing | 27 | 10,600 | ||||

| Account: Truck Expense Account no. 54 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Balance | ✓ | 9,000 | |||

| 31 | Closing | 27 | 9,000 | ||||

| Account: Depreciation Expense- Equipment Account no. 55 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Adjusting | 26 | 8,350 | 8,350 | ||

| 31 | Closing | 27 | 8,350 | ||||

| Account: Depreciation Expense- Equipment Account no. 55 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Adjusting | 26 | 8,350 | 8,350 | ||

| 31 | Closing | 27 | 8,350 | ||||

| Account: Depreciation Expense- Trucks Account no. 56 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Adjusting | 26 | 6,200 | 6,200 | ||

| 31 | Closing | 27 | 6,200 | ||||

| Account: Insurance expense Account no. 57 | |||||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||||

| Debit ($) | Credit ($) | ||||||||

| 2018 | |||||||||

| March | 31 | Adjusting | 26 | 1,800 | 1,800 | ||||

| 31 | Closing | 27 | 1,800 | ||||||

| Account: Miscellaneous expense Account no. 59 | |||||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||||

| Debit ($) | Credit ($) | ||||||||

| 2018 | |||||||||

| March | 31 | Balance | ✓ | 4,800 | |||||

| 31 | Closing | 27 | 4,800 | ||||||

2.

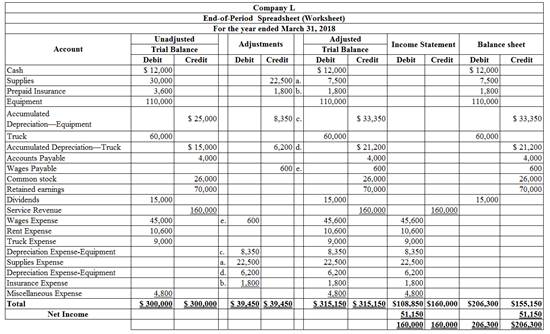

To enter: The unadjusted trial balance on an end-of-period spreadsheet, and complete the spreadsheet.

Explanation of Solution

The unadjusted trial balance on an end-of-period spreadsheet is prepared as follows:

Table (1)

Hence, the unadjusted trial balance on an end-of-period spreadsheet is prepared and completed.

3.

To Journalize and post: The adjusting entries.

Explanation of Solution

The adjusting entries are journalized as follows:

| Date | Description |

Post Ref. |

Debit ($) | Credit ($) | |

| 2018 | Supplies expense | 52 | 22,500 | ||

| March | 31 | Supplies

|

13 | 22,500 | |

| (To record the supplies used) | |||||

Table (2)

- Supplies expense is an expense account, and it is increased. Hence, debit the supplies expense account by $22,500.

- Supplies are the asset account, and it is increased. Hence, credit the supplies account by $22,500.

| Date | Description |

Post Ref. |

Debit ($) | Credit ($) | |

| 2018 | Insurance expense | 57 | 1,800 | ||

| March | 31 | Prepaid insurance | 14 | 1,800 | |

| (To record the insurance expired) | |||||

Table (3)

- Insurance expense is an expense account, and it is increased. Hence, debit the insurance expense account by $1,800.

- Prepaid insurance is an asset account, and it is decreased. Hence, credit the prepaid insurance account by $1,800.

| Date | Description |

Post Ref. |

Debit ($) | Credit ($) | |

| 2018 | Depreciation expense-Equipment | 55 | 8,350 | ||

| March | 31 | Accumulated depreciation- Equipment | 17 | 8,350 | |

| (To record the equipment depreciation) | |||||

Table (4)

- Depreciation expense is an expense account, and it is increased. Hence, debit the wages expense account by $8,350.

- Accumulated depreciation is a contra asset account, and it is increased. Hence, credit the accumulated depreciation account by $8,350.

| Date | Description |

Post Ref. |

Debit ($) | Credit ($) | |

| 2018 | Depreciation expense-Truck | 56 | 6,200 | ||

| March | 31 | Accumulated depreciation- Truck | 19 | 6,200 | |

| (To record the truck depreciation) | |||||

Table (5)

- Depreciation expense is an expense account, and it is increased. Hence, debit the wages expense account by $6,200.

- Accumulated depreciation is a contra asset account, and it is increased. Hence, credit the accumulated depreciation account by $6,200.

| Date | Description |

Post Ref. |

Debit ($) | Credit ($) | |

| 2018 | Wages expense | 51 | 600 | ||

| March | 31 | Wages payable | 22 | 600 | |

| (To record the wages accrued) | |||||

Table (6)

- Wages expense is an expense account, and it is increased. Hence, debit the wages expense account by $600.

- Wages payable is a liability account, and it is increased. Hence, credit the wages payable account by $600.

4.

To prepare: An adjusted trial balance for Company L, as of March 31, 2018.

Explanation of Solution

Prepare an adjusted trial balance for Company L, as of March 31, 2018.

| Company L | |||

| Adjusted Trial Balance | |||

| March 31, 2018 | |||

| Accounts | Account Number | Debit Balances | Credit Balances |

| Cash | 11 | 12,000 | |

| Supplies | 13 | 7,500 | |

| Prepaid Insurance | 14 | 1,800 | |

| Equipment | 16 | 110,000 | |

| Accumulated depreciation- Equipment | 17 | 33,350 | |

| Trucks | 18 | 60,000 | |

| Accumulated depreciation- Trucks | 19 | 21,200 | |

| Accounts payable | 21 | 4,000 | |

| Wages Payable | 22 | 600 | |

| Common stock | 31 | 26,000 | |

| Retained earnings | 32 | 70,000 | |

| Dividends | 15,000 | ||

| Service revenue | 41 | 160,000 | |

| Wages expense | 51 | 45,600 | |

| Supplies expense | 52 | 22,500 | |

| Rent Expense | 53 | 10,600 | |

| Truck Expense | 54 | 9,000 | |

| Depreciation Expense- Equipment | 55 | 8,350 | |

| Depreciation Expense- Trucks | 56 | 6,200 | |

| Insurance Expense | 57 | 1,800 | |

| Miscellaneous Expense | 59 | 4,800 | |

| 315,150 | 315,150 | ||

Table (7)

5.

Explanation of Solution

The net income of Company L for the month of March is $51,150.

| Company L | ||

| Income Statement | ||

| For the year ended March 31, 2018 | ||

| Particulars | Amount ($) | Amount ($) |

| Revenue: | ||

| Service revenue | $160,000 | |

| Expenses: | ||

| Wages Expense | 45,600 | |

| Supplies Expense | 22,500 | |

| Rent Expense | 10,600 | |

| Truck Expense | 9,000 | |

| Depreciation Expense-Equipment | 8,350 | |

| Depreciation Expense-Trucks | 6,200 | |

| Insurance Expense | 1,800 | |

| Miscellaneous Expense | 4,800 | |

| Total Expenses | 108,850 | |

| Net Income | $51,150 | |

Table (8)

Hence, the net income of Company L for the year ended March 31, 2018 is $51,150.

6.

To Journalize: The closing entries for Company L.

Explanation of Solution

Closing entry for revenue and expense accounts:

| Date | Accounts title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| March 31, 2018 | Service revenue | 41 | 160,000 | |

| Income summary | 34 | 160,000 | ||

| (To close the balances of revenue account) | ||||

| March 31, 2018 | Income summary | 34 | 108,850 | |

| Wages expense | 51 | 45,600 | ||

| Supplies Expense | 52 | 22,500 | ||

| Rent Expense | 53 | 10,600 | ||

| Truck Expense | 54 | 9,000 | ||

| Depreciation Expense–Equipment | 55 | 8,350 | ||

| Depreciation Expense–Trucks | 56 | 6,200 | ||

| Insurance Expense | 57 | 1,800 | ||

| Miscellaneous Expense | 59 | 4,800 | ||

| (To close the balances of expense account) | ||||

| March 31, 2018 | Income summary | 34 | 51,150 | |

| Retained earnings | 32 | 51,150 | ||

| (To Close the excess of revenue to expenses) | ||||

| March 31, 2018 | Retained earnings | 32 | 15,000 | |

| Dividends | 33 | 15,000 | ||

| (To close the dividend account to retained earnings account) | ||||

Table (11)

- Laundry revenue is revenue account. Since the amount of revenue is closed and transferred to Income summary account. Here, Company L earned an income of $160,000. Therefore, it is debited.

- Wages Expense, Rent Expense, Insurance Expense, Supplies Expense, Depreciation Expenses, and Miscellaneous Expense are expense accounts. Since the amount of expenses are closed to Income Summary account. Therefore, it is credited.

- Closing entries are also passed in order to close the excess of revenue over the expenses, and the dividend account.

7.

To prepare: The post–closing trial balance of Company L for the month ended March 31, 2018.

Explanation of Solution

Prepare a post–closing trial balance of Company L for the month ended March 31, 2018 as follows:

|

Company L Post-closing Trial Balance March 31, 2018 |

|||

| Particulars |

Account Number |

Debit $ | Credit $ |

| Cash | 11 | 12,000 | |

| Supplies | 13 | 7,500 | |

| Prepaid insurance | 14 | 1,800 | |

| Equipment | 16 | 110,000 | |

| Accumulated depreciation- Equipment | 17 | 33,350 | |

| Trucks | 18 | 60,000 | |

| Accumulated depreciation- Trucks | 19 | 21,200 | |

| Accounts payable | 21 | 4,000 | |

| Wages payable | 22 | 600 | |

| Common stock | 31 | 26,000 | |

| Retained earnings | 106,150 | ||

| Total | 191,300 | 191,300 | |

Table (12)

The debit column and credit column of the post–closing trial balance are agreed, both having balance of $191,300

Want to see more full solutions like this?

Chapter 4 Solutions

Bundle: Financial & Managerial Accounting, Loose-Leaf Version, 14th + CengageNOWv2, 2 terms Printed Access Card

Additional Business Textbook Solutions

Financial Accounting, Student Value Edition (5th Edition)

Foundations of Financial Management

MARKETING:REAL PEOPLE,REAL CHOICES

Understanding Business

Operations Management: Processes and Supply Chains (12th Edition) (What's New in Operations Management)

Horngren's Cost Accounting: A Managerial Emphasis (16th Edition)

- I want to correct answer general accounting questionarrow_forwardQuestion Content Area Work in Process Account Data for Two Months; Cost of Production Reports Pittsburgh Aluminum Company uses process costing to record the costs of manufacturing rolled aluminum, which consists of the smelting and rolling processes. Materials are entered from smelting at the beginning of the rolling process. The inventory of Work in Process—Rolling on September 1 and debits to the account during September were as follows:arrow_forwardQuestion Content Area Work in Process Account Data for Two Months; Cost of Production Reports Pittsburgh Aluminum Company uses process costing to record the costs of manufacturing rolled aluminum, which consists of the smelting and rolling processes. Materials are entered from smelting at the beginning of the rolling process. The inventory of Work in Process—Rolling on September 1 and debits to the account during September were as follows:arrow_forward

- A B CORRECT ANSWER PLEASarrow_forwardKindly help me with accounting questionsarrow_forward1. I want to know how to solve these 2 questions and what the answers are 3. Field & Co. expects its EBIT to be $125,000 every year forever. The firm can borrow at 7%. The company currently has no debt, and its cost of equity is 12%. If the tax rate is 24%, what is the value of the firm? What will the value be if the company borrows $205,000 and uses the proceeds to purchase shares? 2. Firms HD and LD each have $30m in invested capital, $8m of EBIT, and a tax rate of 25%. Firm HD has a D/E ratio of 50% with an interest rate of 8% on their debt. Firm LD has a debt-to-capital ratio of 30%, however, pays 9% interest on its debt. Calculate the following: a. Return on invested capital for firm LDb. Return on equity for each firmc. If HD’s CFO is thinking of lowering the D/E from 50% to 40%, which will lower their interest rate further from 8% to 7%, calculate the new ROE for firm HD.arrow_forward

- what is the variable cost per minute?arrow_forwardI want to know how to solve these 2 questions and what the answers are 1. Stella Motors has $50m in assets, which is financed with 40% debt and 60% common equity. The company’s beta is currently 1.25 and its tax rate is 30%. Find Stella’s unlevered beta. 2. Sugar Corp. uses no debt. The weighted average cost of capital is 7.9%. If the current market value of the equity is $15.6 million and there are no taxes, what is the company’s EBIT?arrow_forwardI don't need ai answer general accounting questionarrow_forward

- Can you help me with accounting questionsarrow_forwardCariveh Co sells automotive supplies from 25 different locations in one country. Each branch has up to 30 staff working there, although most of the accounting systems are designed and implemented from the company's head office. All accounting systems, apart from petty cash, are computerised, with the internal audit department frequently advising and implementing controls within those systems. Cariveh has an internal audit department of six staff, all of whom have been employed at Cariveh for a minimum of five years and some for as long as 15 years. In the past, the chief internal auditor appoints staff within the internal audit department, although the chief executive officer (CEO) is responsible for appointing the chief internal auditor. The chief internal auditor reports directly to the finance director. The finance director also assists the chief internal auditor in deciding on the scope of work of the internal audit department. You are an audit manager in the internal audit…arrow_forwardCariveh Co sells automotive supplies from 25 different locations in one country. Each branch has up to 30 staff working there, although most of the accounting systems are designed and implemented from the company's head office. All accounting systems, apart from petty cash, are computerised, with the internal audit department frequently advising and implementing controls within those systems. Cariveh has an internal audit department of six staff, all of whom have been employed at Cariveh for a minimum of five years and some for as long as 15 years. In the past, the chief internal auditor appoints staff within the internal audit department, although the chief executive officer (CEO) is responsible for appointing the chief internal auditor. The chief internal auditor reports directly to the finance director. The finance director also assists the chief internal auditor in deciding on the scope of work of the internal audit department. You are an audit manager in the internal audit…arrow_forward

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning

Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage LearningCentury 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage LearningCentury 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning