Concept explainers

Videos

Kelly Pitney began her consulting business, Kelly Consulting, on April 1, 2016. The accounting cycle for Kelly Consulting for April, including financial statements, was illustrated in this chapter. During May, Kelly Consulting entered into the following transactions:

Instructions

- 1. The chart of accounts for Kelly Consulting is shown in Exhibit 9, and the post-closing

trial balance as of April 30, 2016, is shown in Exhibit 17. For each account in the post-closing trial balance, enter the balance in the appropriate Balance column of a four-column account. Date the balances May 1, 2016, and place a check mark (✔) in the Posting Reference column. Journalize each of the May transactions in a two column journal starting on Page 5 of the journal and using Kelly Consulting’s chart of accounts. (Do not insert the account numbers in the journal at this time.) - 2. Post the journal to a ledger of four-column accounts.

- 3. Prepare an unadjusted trial balance.

- 4. At the end of May, the following adjustment data were assembled. Analyze and use these data to complete parts (5) and (6)

- a. Insurance expired during May is $275.

- b. Supplies on hand on May 31 are $715.

- c.

Depreciation of office equipment for May is $330. - d. Accrued receptionist salary on May 31 is $325.

- e. Rent expired during May is $1,600.

- f. Unearned fees on May 31 are $3,210.

5. (Optional) Enter the unadjusted trial balance on an end-of-period spreadsheet and complete the spreadsheet.

6. Journalize and post the

7. Prepare an adjusted trial balance.

8. Prepare an income statement, a statement of owner’s equity, and a

9. Prepare and post the closing entries. Record the closing entries on Page 8 of the journal. (Income Summary is account #33 in the chart of accounts.) Indicate closed accounts by inserting a line in both the Balance columns opposite the closing entry.

10. Prepare a post-closing trial balance.

(1)

Journalize transactions of May in a two column journal beginning on page 5.

Explanation of Solution

Journal: Journal is the book of original entry. Journal consists of the day-to-day financial transactions in a chronological order. The journal has two aspects; they are debit aspect and the credit aspect.

T-Accounts: T-accounts are referred as T-account because its format represents the letter “T”. The T-accounts consists of the following:

- The title of accounts.

- The debit side (Dr) and,

- The credit side (Cr).

Adjusted trial balance: The unadjusted trial balance is the summary of all the ledger accounts that appears on the ledger accounts before making adjusting journal entries.

Adjusting entries: An adjusting entry is prepared when the trial balance is not up-to-date, and complete, and they are usually prepared at the end of the accounting period. This adjusting entry is essential for preparing the financial statements of the business.

Spreadsheet: A spreadsheet is a worksheet. It is used while preparing a financial statement. It is a type of form having multiple columns and it is used in the adjustment process. The use of a worksheet is optional for any organization. A worksheet can neither be considered as a journal nor a part of the general ledger.

Statement of owners’ equity: This statement reports the beginning owner’s equity and all the changes, which led to ending owners’ equity. Additional capital, net income from income statement is added to and drawing is deducted from beginning owner’s equity to arrive at the end result, ending owner’s equity.

Income statement: An income statement is one of the financial statements which shows the revenues, and expenses of the company. The income statement is prepared to ascertain the net income/loss of the company, by deducting the expenses from the revenues.

Balance sheet: A balance sheet is a financial statement consists of the assets, liabilities, and the stockholder’s equity of the company. The balance of the assets account must be equal to that of the liabilities and the stockholder’s equity account.

Closing entries: Closing entries are recorded in order to close the temporary accounts such as incomes and expenses by transferring them to the permanent accounts. It is passed at the end of the accounting period, to transfer the final balance.

Post-Closing Trial Balance: After passing all the journal entries and the closing entries of the permanent accounts and then further posting them to each of the respective accounts, a post-closing trial balance is prepared which consists of a list of all the permanent accounts. A post-closing trial balance serves as an evidence to prove that the balance of the permanent accounts is equal.

Journalize the transactions of May in a two column journal beginning on page 5.

| Journal Page 5 | |||||

| Date | Description | Post. Ref | Debit ($) | Credit ($) | |

| 2016 | 3 | Cash | 11 | 4,500 | |

| May | Unearned fees | 23 | 4,500 | ||

| (To record the cash received for the service yet to be provide) | |||||

| 5 | Cash | 11 | 2,450 | ||

| Accounts receivable | 12 | 2,450 | |||

| (To record the cash received from clients) | |||||

| 9 | Miscellaneousexpense | 59 | 225 | ||

| Cash | 11 | 225 | |||

| (To record the payment made for Miscellaneous expense) | |||||

| 13 | Accounts payable | 21 | 640 | ||

| Cash | 11 | 640 | |||

| (To record the payment made to creditors on account) | |||||

| 15 | Accounts receivable | 12 | 9,180 | ||

| Fees earned | 41 | 9,180 | |||

| (To record the revenue earned and billed) | |||||

| 14 | Salary Expense | 51 | 630 | ||

| Salaries payable | 22 | 120 | |||

| Cash | 11 | 750 | |||

| (To record the payment made for salary) | |||||

| Cash | 11 | 8,360 | |||

| 17 | Fees earned | 41 | 8,360 | ||

| (To record the receipt of cash) | |||||

Table (1)

| Journal Page 6 | |||||

| Date | Description | Post. Ref | Debit ($) | Credit ($) | |

| 2016 | 18 | Supplies | 14 | 735 | |

| May | Accounts payable | 21 | 735 | ||

| (To record the payment made for automobile expense) | |||||

| 21 | Accounts receivable | 12 | 4,820 | ||

| Fees earned | 41 | 4,820 | |||

| (To record the payment of advertising expense) | |||||

| 25 | Cash | 11 | 7,900 | ||

| Fees earned | 41 | 7,900 | |||

| (To record the cash received from client for fees earned) | |||||

| 27 | Cash | 11 | 9,520 | ||

| Accounts receivable | 12 | 9,520 | |||

| (To record the cash received from clients) | |||||

| 28 | Salary expense | 51 | 750 | ||

| Cash | 11 | 750 | |||

| (To record the payment of salary) | |||||

| 30 | Miscellaneous Expense | 59 | 260 | ||

| Cash | 11 | 260 | |||

| (To record the payment of telephone charges) | |||||

| 31 | Miscellaneous Expense | 59 | 810 | ||

| Cash | 11 | 810 | |||

| (To record the payment of electricity charges) | |||||

| 31 | Cash | 11 | 3,300 | ||

| Fees earned | 41 | 3,300 | |||

| (To record the cash received from client for fees earned) | |||||

| 31 | Accounts receivable | 12 | 2,650 | ||

| Fees earned | 41 | 2,650 | |||

| (To record the revenue earned and billed) | |||||

| 31 | Dividends | 33 | 10,500 | ||

| Cash | 11 | 10,500 | |||

| (To record the drawing made for personal use) | |||||

Table (2)

(2), (6) and (9)

Record the balance of each account in the appropriate balance column of a four-column account and post them to the ledger.

Explanation of Solution

| Account: Cash Account no.11 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 1 | Balance | ✓ | 22,100 | |||

| 3 | 5 | 4,500 | 26,600 | ||||

| 5 | 5 | 2,450 | 29,050 | ||||

| 9 | 5 | 225 | 28,825 | ||||

| 13 | 5 | 640 | 28,185 | ||||

| 16 | 5 | 750 | 27,435 | ||||

| 17 | 5 | 8,360 | 35,795 | ||||

| 25 | 6 | 7,900 | 43,695 | ||||

| 27 | 6 | 9,520 | 53,215 | ||||

| 28 | 6 | 750 | 52,465 | ||||

| 30 | 6 | 260 | 52,205 | ||||

| 31 | 6 | 810 | 51,395 | ||||

| 31 | 6 | 3,300 | 54,695 | ||||

| 31 | 6 | 10,500 | 44,195 | ||||

Table (3)

| Account: Accounts Receivable Account no.12 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 1 | Balance | ✓ | 3,400 | |||

| 5 | 5 | 2,450 | 950 | ||||

| 15 | 5 | 9,180 | 10,130 | ||||

| 21 | 6 | 4,820 | 14,950 | ||||

| 27 | 6 | 9,520 | 5,430 | ||||

| 31 | 6 | 2,650 | 8,080 | ||||

Table (4)

| Account: Supplies Account no.14 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 1 | Balance | ✓ | 1,350 | |||

| 20 | 6 | 735 | 2,085 | ||||

| 30 | Adjusting | 7 | 1,350 | 715 | |||

Table (5)

| Account: Prepaid Rent Account no.15 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 1 | Balance | ✓ | 3,200 | |||

| 31 | Adjusting | 7 | 1,600 | 1,600 | |||

Table (6)

| Account: Prepaid Insurance Account no.16 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 1 | Balance | ✓ | 1,500 | |||

| 31 | Adjusting | 7 | 275 | 1,225 | |||

Table (7)

| Account: Office equipment Account no.18 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 1 | Balance | ✓ | 14,500 | |||

Table (8)

| Account: Accumulated Depreciation-Office equipment Account no.19 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 1 | Balance | ✓ | 330 | |||

| 31 | Adjusting | 7 | 330 | 660 | |||

Table (9)

| Account: Accounts Payable Account no.21 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 1 | Balance | ✓ | 800 | |||

| 13 | 5 | 640 | 160 | ||||

| 20 | 6 | 735 | 895 | ||||

Table (10)

| Account: Salaries Payable Account no.22 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 1 | Balance | ✓ | 120 | |||

| 16 | 5 | 120 | |||||

| 31 | Adjusting | 7 | 325 | 325 | |||

Table (11)

| Account: Unearned Fees Account no.23 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 1 | Balance | ✓ | 2,500 | |||

| 3 | 5 | 4,500 | 7,000 | ||||

| 31 | Adjusting | 7 | 3,790 | 3,210 | |||

Table (12)

|

Account: Common Stock Account no.31 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 1 | Balance | ✓ | 42,300 | |||

| 31 | Closing | 8 | 33,425 | 75,725 | |||

| 31 | Closing | 8 | 10,500 | 65,225 | |||

Table (13)

| Account: Dividends Account no.33 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 31 | 6 | 10,500 | 10,500 | |||

| 31 | Closing | 8 | 10,500 | ||||

Table (14)

| Account: Income Summary Account no.34 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 31 | Closing | 8 | 40,000 | 40,000 | ||

| 31 | Closing | 8 | 6,575 | 33,425 | |||

| 31 | Closing | 8 | 33,425 | ||||

Table (15)

| Account: Fees earned Account no.41 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 15 | 5 | 9,180 | 9,180 | |||

| 17 | 5 | 8,360 | 17,540 | ||||

| 21 | 6 | 4,820 | 22,360 | ||||

| 25 | 6 | 7,900 | 30,260 | ||||

| 31 | 6 | 3,300 | 33,560 | ||||

| 31 | 6 | 2,650 | 36,210 | ||||

| 31 | Adjusting | 7 | 3,790 | 40,000 | |||

| 31 | Closing | 8 | 40,000 | ||||

Table (16)

| Account: Salary expense Account no.51 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 16 | 5 | 630 | 630 | |||

| 28 | 6 | 750 | 1,380 | ||||

| 31 | Adjusting | 7 | 325 | 1,705 | |||

| 31 | Closing | 8 | 1,705 | ||||

Table (17)

| Account: Rent expense Account no.52 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 31 | Adjusting | 7 | 1,600 | 1,600 | ||

| 31 | Closing | 8 | 1,600 | ||||

Table (18)

| Account: Supplies expense Account no.53 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 31 | Adjusting | 7 | 1,370 | 1,370 | ||

| 31 | Closing | 8 | 1,370 | ||||

Table (19)

| Account: Depreciation expense Account no.54 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 31 | Adjusting | 7 | 330 | 330 | ||

| 31 | Closing | 8 | 330 | ||||

Table (20)

| Account: Insurance expense Account no.54 | |||||||

| Date | Item | PostRef. |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 31 | Adjusting | 7 | 275 | 275 | ||

| 31 | Closing | 8 | 275 | ||||

Table (21)

| Account: Miscellaneous expense Account no.59 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 9 | 5 | 225 | 225 | |||

| 30 | 6 | 260 | 485 | ||||

| 31 | 6 | 810 | 1,295 | ||||

| 31 | Closing | 8 | 1,295 | ||||

Table (22)

(3)

Prepare the unadjusted trial balance of Consulting K at May, 31.

Explanation of Solution

Prepare an unadjusted trial balance of Consulting K for the month ended May, 31 as follows:

|

K Consulting Unadjusted Trial Balance May 31, 2016 | |||

| Particulars |

Account No. | Debit $ | Credit $ |

| Cash | 11 | 44,195 | |

| Accounts receivable | 12 | 8,080 | |

| Supplies | 14 | 2,085 | |

| Prepaid rent | 15 | 3,200 | |

| Prepaid insurance | 16 | 1,500 | |

| Office Equipment | 18 | 14,500 | |

| Accumulated depreciation-Office equipment | 19 | 330 | |

| Accounts payable | 21 | 895 | |

| Salaries payable | 22 | 0 | |

| Unearned fees | 23 | 7,000 | |

| KP Capital | 31 | 42,300 | |

| KP Drawings | 33 | 10,500 | |

| Fees earned | 41 | 36,210 | |

| Salary expense | 51 | 1,380 | |

| Rent expense | 52 | 0 | |

| Supplies expense | 53 | 0 | |

| Depreciation expense | 54 | 0 | |

| Insurance expense | 55 | 0 | |

| Miscellaneous expense | 59 | 1,295 | |

| Total | $86,735 | $86,735 | |

Table (23)

The debit column and credit column of the unadjusted trial balance are agreed, both having balance of $86,735.

(5)

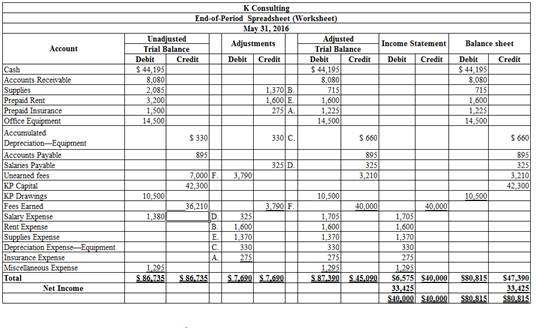

Enter unadjusted trial balance on an end-of-period spreadsheet.

Explanation of Solution

The unadjusted trial balance on an end-of-period spreadsheet is prepared as follows:

Table (24)

Hence, the unadjusted trial balance on an end-of-period spreadsheet is prepared and completed.

(6)

Journalize the adjusting entries of Consulting K for May 31.

Explanation of Solution

The adjusting entries of Consulting K for May 31, 2016are as follows:

| Date | Accounts title and explanation | Post Ref. |

Debit ($) |

Credit ($) | |

| 2016 | Insurance expense | 55 | 275 | ||

| May | 31 | Prepaid insurance | 16 | 275 | |

| (To record the insurance expense for May ) | |||||

| 31 | Supplies expense | 53 | 1,370 | ||

| Supplies | 14 | 1,370 | |||

| (To record the supplies expense) | |||||

| 31 | Depreciation expense | 54 | 330 | ||

| Accumulated Depreciation | 19 | 330 | |||

| (To record the depreciation and the accumulated depreciation) | |||||

| 31 | Salaries expense | 51 | 325 | ||

| Salaries payable | 22 | 325 | |||

| (To record the accrued salaries payable) | |||||

| 31 | Rent expense | 52 | 1,600 | ||

| Prepaid rent | 15 | 1,600 | |||

| (To record the rent expense for May ) | |||||

| 31 | Unearned fees | 23 | 3,790 | ||

| Fees earned | 41 | 3,790 | |||

| (To record the receipt of unearned fees) | |||||

Table (25)

Working notes:

(7)

Prepare an adjusted trial balance of Consulting K for May 31, 2016.

Explanation of Solution

An adjusted trial balance of Consulting K for May 31, 2016 is prepared as follows:

|

K Consulting Adjusted Trial Balance May 31, 2016 | |||

| Particulars |

Account No. | Debit $ | Credit $ |

| Cash | 11 | 44,195 | |

| Accounts receivable | 12 | 8,080 | |

| Supplies | 14 | 715 | |

| Prepaid insurance | 16 | 1,600 | |

| Prepaid rent | 15 | 1,225 | |

| Office Equipment | 18 | 14,500 | |

| Accumulated Depreciation-Office equipment | 19 | 660 | |

| Accounts payable | 21 | 895 | |

| Salaries payable | 22 | 325 | |

| Unearned fees | 23 | 3,210 | |

| Common stock | 31 | 30,000 | |

| Retained earnings | 32 | 12,300 | |

| Dividends | 33 | 10,500 | |

| Fees earned | 41 | 40,000 | |

| Salary expense | 51 | 1,705 | |

| Rent expense | 52 | 1,600 | |

| Supplies Expense | 53 | 1,370 | |

| Depreciation expense | 54 | 330 | |

| Insurance expense | 55 | 275 | |

| Miscellaneous expense | 59 | 1,295 | |

| Total | $87,390 | $87,390 | |

Table (25)

The debit column and credit column of the adjusted trial balance are agreed, both having balance of $87,390.

(8)

Prepare income statement for the year ended May 31, 2016.

Explanation of Solution

An income statement for the year ended May 31, 2016 is as follows:

| K Consulting | ||

| Income Statement | ||

| For the year ended May 31, 2016 | ||

| Particulars | Amount ($) | Amount ($) |

| Revenues: | ||

| Fees Earned | 40,000 | |

| Expenses: | ||

| Salaries Expense | 1,705 | |

| Rent Expense | 1,600 | |

| Supplies Expense | 1,370 | |

| Depreciation Expense- Building | 330 | |

| Insurance Expense | 275 | |

| Miscellaneous Expense | 1,295 | |

| Total Expenses | 6,575 | |

| Net Income | $33,425 | |

Table (26)

Hence, the net income of K Consulting for the year ended May 31, 2016is $33,425.

Prepare owners’ equity statement for the year ended May 31, 2016.

Explanation of Solution

The statement of owners’ equity for the year ended May 31, 2016 is as follows:

| G Consulting | ||

| Owners’ Equity Statement | ||

| For the Year Ended May 31, 2016 | ||

| Particulars | Amount ($) | Amount ($) |

| KP Capital, May 1, 2016 | 42,300 | |

| Add: Net income | 33,425 | |

| Less: KP Drawings | (10,500) | |

| Change in owners’ equity | 22,925 | |

| KP Capital, May 31, 2016 | $65,225 | |

Table (27)

Hence, owners’ equity for the year ended May 31, 2016is $65,225.

Prepare balance sheet of K Consulting at May 31, 2016.

Answer to Problem 1CPP

| K Consulting | |||

| Balance Sheet | |||

| May 31, 2016 | |||

| Assets | |||

| Current Assets: | $ | $ | |

| Cash | 44,195 | ||

| Accounts Receivable | 8,080 | ||

| Supplies | 715 | ||

| Prepaid Rent | 1,600 | ||

| Prepaid Insurance | 1,225 | ||

| Total Current Assets | 55,815 | ||

| Property, plant and equipment: | |||

| Office Equipment | 14,500 | ||

| Less: Accumulated Depreciation | (660) | ||

| Total Plant Assets | 13,840 | ||

| Total Assets | $69,655 | ||

| Liabilities | |||

| Current Liabilities: | |||

| Accounts Payable | 895 | ||

| Salaries Payable | 325 | ||

| Unearned rent | 3,210 | ||

| Total Liabilities | $4,430 | ||

| Owners’ Equity | |||

| Capital | 65,225 | ||

| Total owners ‘equity | 65,225 | ||

| Total Liabilities and Owners’ Equity | $69,655 | ||

Table (28)

Explanation of Solution

It is one of the financial statements, which shows the assets, liabilities, and stockholders’ equity of a company at a particular point of time. It reveals the financial health of a company. Thus, this statement is also called as the Statement of Financial Position. It helps the users to know about the creditworthiness of a company as to whether the company has enough assets to pay off its liabilities.

Therefore, the total assets and total liabilities plus stockholders’ equity of Consulting Kat May 31, 2016 is $69,655.

(9)

Journalize closing entries for K Consulting.

Answer to Problem 1CPP

Closing entry for revenue and expense accounts:

| Date | Accounts title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| May 31, 2016 | Fees earned | 41 | 40,000 | |

| Income summary | 34 | 40,000 | ||

| (To close the balances of revenue account) | ||||

| May 31, 2016 | Income summary | 34 | 6,575 | |

| Salary expense | 51 | 1,705 | ||

| Rent Expense | 52 | 1,600 | ||

| Supplies Expense | 53 | 1,370 | ||

| Depreciation Expense | 54 | 330 | ||

| Insurance Expense | 55 | 275 | ||

| Miscellaneous Expense | 59 | 1,295 | ||

| (To close the balances of expense account) | ||||

| July 31 | Income Summary | 33 | 33,425 | |

| KP Capital | 31 | 33,425 | ||

| (To close balance of income summary are transferred to owners’ capital account) | ||||

| July 31 | KP’s Capital | 31 | 10,500 | |

| KP’s Drawing | 32 | 10,500 | ||

| (To Close the capital and drawings account) | ||||

Table (29)

Explanation of Solution

- A Service fee earned is revenue account. Since the amount of revenue is closed and transferred to JH’s capital account. Here, G Consulting earned an income of $64,550, and $18,000. Therefore, it is debited.

- Salaries Expense, Rent Expense, Insurance Expense, Utilities Expense, Supplies Expense, Depreciation Expense, Advertising Expense, JH Capital, and Miscellaneous Expense are expense accounts. Since the amount of expenses are closed to Income Summary account. Therefore, it is credited.

- Owner’s capital is a component of owner’s equity. Thus, owners ‘equity is debited since the capital is decreased on owners’ drawings.

- Owner’s drawings are a component of owner’s equity. It is credited because the balance of owners’ drawing account is transferred to owners ‘capital account.

(10)

Journalize the closing entries for K Consulting.

Explanation of Solution

Prepare a post–closing trial balance of K Consulting for the month ended May 31, 2016 as follows:

|

Consulting K Post-closing Trial Balance May, 31, 2016 | |||

| Particulars | Account Number | Debit $ | Credit $ |

| Cash | 11 | 44,195 | |

| Accounts receivable | 12 | 8,080 | |

| Supplies | 14 | 715 | |

| Prepaid rent | 15 | 1,600 | |

| Prepaid insurance | 16 | 1,225 | |

| Office Equipment | 18 | 14,500 | |

| Accumulated depreciation –Office Equipment | 19 | 660 | |

| Accounts payable | 21 | 895 | |

| Salaries payable | 22 | 325 | |

| Unearned rent | 23 | 3,210 | |

| Common stock | 31 | 30,000 | |

| Retained earnings | 32 | 35,225 | |

| Total | $70,315 | $70,315 | |

Table (30)

The debit column and credit column of the post–closing trial balance are agreed, both having balance of $70,315.

Want to see more full solutions like this?

Chapter 4 Solutions

Financial Accounting

- What is the actual total direct materials cost for the current e?arrow_forwardPlease My problem with accountingarrow_forwardRick Industries reported beginning total assets of $18,500,000 and ending total assets of $21,700,000 for the year 2023. The company's asset turnover ratio was 2.1 times. Based on this information, what was the net sales for the year 2023?arrow_forward

- A change in accounting estimate affects? A. Prior periods only B. All periods equally C. Current period only D. Current and future periods MCQarrow_forwardCan you solve this financial accounting problem using accurate calculation methods?arrow_forwardI need guidance with this financial accounting problem using the right financial principles.arrow_forward

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College