Concept explainers

Videos

(a)

T- Accounts:

T-accounts are referred as T-account because its format represents the letter “T”. The T-accounts consists of the following:

- The title of accounts.

- The debit side (Dr) and,

- The credit side (Cr).

To Enter: The beginning balancesin the general ledger as of April 30, 2017.

(a)

Explanation of Solution

The beginning balancesare entered in the general ledger using T- Accounts as on April 30, 2017 as follows:

| Cash | |||

| Apr. 30 | $5,000 | ||

| Bal. | $ 5,000 | ||

Table (1)

| Supplies | |||

| Apr. 30 | $ 500 | ||

| Bal. | $ 500 | ||

Table (2)

| Equipment | |||

| Apr. 30 | $ 24,000 | ||

| Bal. | $ 24,000 | ||

Table (3)

| Accounts Payable | |||

| Apr. 30 | $2,100 | ||

| Bal. | $ 2,100 | ||

Table (4)

| Notes Payable | |||

| Apr. 30 | $10,000 | ||

| Bal. | $10,000 | ||

Table (5)

| Unearned Service Revenue | |||

| Apr. 30 | $ 1,000 | ||

| Bal. | $ 1,000 | ||

Table (6)

| Common Stock | |||

| Apr. 30 | $ 5,000 | ||

| Bal. | $ 5,000 | ||

Table (7)

|

| |||

| Apr. 30 | $11,400 | ||

| Bal. | $11,400 | ||

Table (8)

(b)

Journal:

Journal is the book of original entry. Journal consists of the day-to-day financial transactions in a chronological order. The journal has two aspects; they are debit aspect and the credit aspect.

To journalize: The business transactions as given for Incorporation P.

(b)

Explanation of Solution

| Date | Account Title and Explanation | Debit ($) | Credit ($) |

| May 1 | Rent Expenses | 1,000 | |

| Cash | 1,000 | ||

| (To record the payment of rent) | |||

| May 4 | Accounts Payable | 1,100 | |

| Cash | 1,100 | ||

| (To record the payment of account payable at April 30) | |||

| May 7 | Cash | 1,500 | |

| Unearned Service revenue | 1,500 | ||

| (To record the cash received in advance for the services yet to be provided) | |||

| May 8 | Cash | 1,200 | |

| Service Revenue | 1,200 | ||

| (To record the cash received for the services performed) | |||

| May 14 | Salaries Expenses | 1,200 | |

| Cash | 1,200 | ||

| (To record the payment of salaries to employees) | |||

| May 15 | Cash | 800 | |

| Service Revenue | 800 | ||

| (To record the collection of cash for the services performed) | |||

| May 15 | Unearned Service revenue | 700 | |

| Service Revenue | 700 | ||

| (To record the recognition of service revenue from the unearned service revenue account) | |||

| May 21 | Accounts Payable | 1,000 | |

| Cash | 1,000 | ||

| (To record the payment of cash on account from the remaining balance due on April 30) | |||

| May 22 | Cash | 1,000 | |

| Service Revenue | 1,000 | ||

| (To record the cash received for the services performed) | |||

| May 22 | Supplies | 700 | |

| Accounts Payable | 700 | ||

| (To record the purchase of supplies on account) | |||

| May 25 | Advertising Expenses | 500 | |

| Accounts Payable | 500 | ||

| (To record the advertising expenses, due to be paid on June 13) | |||

| May 25 | Utilities Expenses | 400 | |

| Cash | 400 | ||

| (To record the payment of utilities expenses) | |||

| May 29 | Cash | 1,700 | |

| Service Revenue | 1,700 | ||

| (To record the cash received for the services performed) | |||

| May 29 | Unearned Service revenue | 600 | |

| Service Revenue | 600 | ||

| ( To record the recognition of service revenue from the unearned service revenue account) | |||

| May 31 | Interest Expenses | 50 | |

| Cash | 50 | ||

| (To record the payment of interest on notes payable) | |||

| May 31 | Salaries Expenses | 1,200 | |

| Cash | 1,200 | ||

| (To record the salaries paid to the employees) | |||

| May 31 | Income Tax Expenses | 150 | |

| Cash | 150 | ||

| (To record the payment of income tax) |

Table(1)

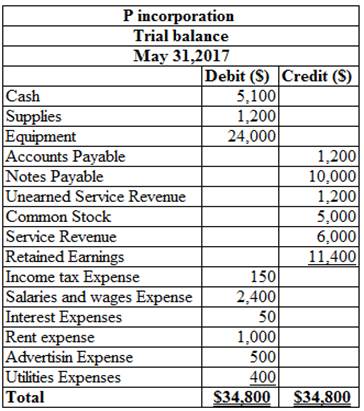

(c)

A trial balance is the summary of all the ledger accounts. The trial balance is prepared to check the total balance of the debit with the total of the balance of the credit column, which must be equal. The trial balance is usually prepared to check accuracy of ledger balances. In trial balance the debit balances are listed in the left column, and credit balances are listed in the right column.

To

(c)

Explanation of Solution

| Cash | |||

| Apr. 30 | $ 5,000 | May. 1 | $1,000 |

| May. 7 | $ 1,500 | 4 | $1,100 |

| 8 | $ 1,200 | 14 | $1,200 |

| 15 | $ 800 | 21 | $1,000 |

| 22 | $ 1,000 | 25 | $ 400 |

| 29 | $ 1,700 | 31 | $ 50 |

| 31 | $1,200 | ||

| 31 | $ 150 | ||

| Total | 11,200 | Total | 6,100 |

| Bal. | $ 5,100 | ||

Table (1)

| Supplies | |||

| Apr. 30 | $ 500 | ||

| Bal. | $ 500 | ||

Table (2)

| Equipment | |||

| Apr. 30 | $24,000 | ||

| Bal. | $24,000 | ||

Table (3)

| Accounts Payable | |||

| Apr. 30 | $2,100 | ||

| May 4 | $1,100 | May 22 | $ 700 |

| May 21 | $1,000 | 25 | $ 500 |

| Total | $2,100 | Total | $3,300 |

| Bal. | $1,200 | ||

Table (4)

| Notes Payable | |||

| Apr. 30 | $10,000 | ||

| Bal. | $10,000 | ||

Table (5)

| Unearned Service Revenue | |||

| Apr. 30 | $ 1,000 | ||

| May 15 | $ 700 | May 7 | $ 1,500 |

| May 29 | $ 600 | ||

| Total | $ 1,300 | Total | $2,500 |

| Bal. | $1,200 | ||

Table (6)

| Common Stock | |||

| Apr. 30 | $ 5,000 | ||

| Bal. | $ 5,000 | ||

Table (7)

| Retained earnings | |||

| Apr. 30 | $11,400 | ||

| Bal. | $11,400 | ||

Table (8)

| Service Revenue | |||

| May. 8 | $1,200 | ||

| 15 | $ 800 | ||

| 15 | $ 700 | ||

| 22 | $1,000 | ||

| 29 | $1,700 | ||

| 29 | $ 600 | ||

| Bal. | $6,000 | ||

Table (9)

| Salaries and wages expenses | |||

| May 14 | $ 1,200 | ||

| May 31 | $ 1,200 | ||

| Bal. | $ 2,400 | ||

Table (10)

| Rent Expense | |||

| May. 1 | $1,000 | ||

| Bal. | $1,000 | ||

Table (11)

| Supplies Expense | |||

| May. 22 | $ 700 | ||

| Bal. | $ 700 | ||

Table (12)

| Advertising Expense | |||

| May. 25 | $ 500 | ||

| Bal. | $ 500 | ||

Table (13)

| Utilities Expense | |||

| May. 25 | $ 400 | ||

| Bal. | $ 400 | ||

Table (14)

| Interest Expense | |||

| May. 31 | $ 50 | ||

| Bal. | $ 50 | ||

Table (15)

| Income tax Expense | |||

| May. 31 | $ 150 | ||

| Bal. | $ 150 | ||

Table (16)

(d)

To Prepare: The trial balance of Incorporation P as on May 31, 2017.

(d)

Explanation of Solution

Table-1

Want to see more full solutions like this?

Chapter 3 Solutions

Financial Accounting 8th Edition

- Problem No. 3 The business assets of Glea Yares and Eunice Alico appear below: Yares Alico Cash P 10,000 P 25,000 Accounts Receivable 245,000 565,000 Inventories 122,000 260,000 Land 664,000 Building 938,000 Furniture and Fixtures Total 87,000 P1,128,000 36,000 P1,824,000 000,00 000,000 19 000,008 Account Payable Notes Payable P 178,000 200,000 Yare, Capital diw 750,000 P 245,000 345,000 adi to omen Alicol, Capital Total P1,128,000 1,234,000 P1,824,000 On March 5, 2025, Yares and Alico agreed to form a partnership contributing their assets and equities subject to the following adjustments: qining arboj su to nam a. Accounts receivable of P15,000 in Yares' books and P30,000 in Alico's are uncollectible. b. Inventories of P5,500 and P6,500 are worthless in Yares' and Alico's respective books. Required: 1. In the books of Yares, prepare the necessary journal entries: a. To record the adjustments to Yares' assets b. To close the books of Yares of viande no 251qgque oroa snemu ni 2. In the…arrow_forwardCritically evaluate the progress and challenges in achieving a single set of global accounting standards. Discuss the benefits and drawbacks of globalization in accounting, providing relevant examples. Critically assess the role of the Conceptual Framework in financial reporting and its influence on accounting theory and practice. Discuss how the qualitative characteristics outlined in the Conceptual Framework enhance financial reporting and contribute to decision-usefulness. Provide examples to support your analysis. a) Define research methodology in the context of accounting theory and discuss the importance of selecting appropriate research methodology. Evaluate the strengths and limitations of quantitative and qualitative approaches in accounting research. (10 marks) b) Assess the role of modern accounting theories in guiding research in accounting. Discuss how contemporary theories, such as stakeholder theory, legitimacy theory, and behavioral accounting theory, shape…arrow_forwardCritically evaluate the progress and challenges in achieving a single set of global accounting standards. Discuss the benefits and drawbacks of globalization in accounting, providing relevant examples. Critically assess the role of the Conceptual Framework in financial reporting and its influence on accounting theory and practice. Discuss how the qualitative characteristics outlined in the Conceptual Framework enhance financial reporting and contribute to decision-usefulness. Provide examples to support your analysis. a) Define research methodology in the context of accounting theory and discuss the importance of selecting appropriate research methodology. Evaluate the strengths and limitations of quantitative and qualitative approaches in accounting research. (10 marks) b) Assess the role of modern accounting theories in guiding research in accounting. Discuss how contemporary theories, such as stakeholder theory, legitimacy theory, and behavioral accounting theory, shape…arrow_forward

- Problem No. 2 The trial balance of Cleint Lumanao Nacho Supplies on February 10, 2025, before accepting Shila Tajonera as partner is shown as follows: Account Title Debit Credit Ato Cash reening smuo P 100,000 Accounts Receivable 250,000 Allowance for Uncollectible Accounts P 20,000 o Merchandise Inventory Equipment Accumulated Depreciation Accounts Payable Notes Payable 120,000 275,000 55,000 50,000 82,000 538,000 Lumanao, Capital Total P 745,000 P 745,000 Tajonera offered to invest cash to get a capital credit equal to one-half of Lumanao's capital after giving effect to the adjustments below. Lumanao accepted the offer. Valuation of some of the assets and liabilities of Lumanao, as agreed by the partners, are the following: • The merchandise is to be valued at P93,000. The accounts receivable is estimated to be 90% collectible. • The equipment is to be valued at P200,000. The partners also agreed that the name of the partnership will be Nacho Business. Required: 1. In the books of…arrow_forwardIf data is unclear in image or image blurr then comment.arrow_forwardSolve correctly without using aiarrow_forward

- Give solution correctly no chatgptarrow_forwardProblem No. 1 On January 1, 2025, Manuel Cruz and Sherimae Diasalo agreed to form a partnership that will manufacture and sell biscuits. The partnership agreement specified that Cruz is to invest cash of P1,000,000 and Diasalo is to contribute land and building to serve as the office and factory of the business. The following amounts are applicable to the property of Diasalo: Acquisition Cost Fair Market Value Land Building P1,000,000 500,000 P1,500,000 850,000 During the formation, it was found out that Cruz has accounts receivable amounting to P70,000 and the partners agreed that it will be assumed by the partnership. The name of the partnership will be Fita Pan. Required: 1. Prepare journal entry to record: a. The investment of Cruz to the partnership b. The investment of Diasalo to the partnershipood relay ni 000,219 2. Prepare the statement of financial position of the partnership as of January 1, 2025 Problem No. 2 The trial balance of Cleint Lumanao Nacho Supplies on February…arrow_forwardA company's stock price is $80, with earnings per share (EPS) of $10 and an expected growth rate of 12%.arrow_forward

- Kazama owns JKL Corporation stock with a basis of $20,000. He exchanges this for $24,000 of STU stock and $8,000 of STU securities as part of a tax-free reorganization. What is Kazama's basis in the STU stock?arrow_forwardKensington Textiles, Inc. manufactures customized tablecloths. An experienced worker can sew and embroider 10 tablecloths per hour. Due to the repetitive nature of the work, employees take a 10-minute break after every 10 tablecloths. Additionally, before starting each batch of 10 tablecloths, workers spend 8 minutes cleaning and setting up their sewing machines. Calculate the standard quantity of direct labor for one tablecloth.arrow_forwardSolvearrow_forward

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax CollegePrinciples of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax CollegePrinciples of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning