Videos

Capital rationing decision for a service company involving

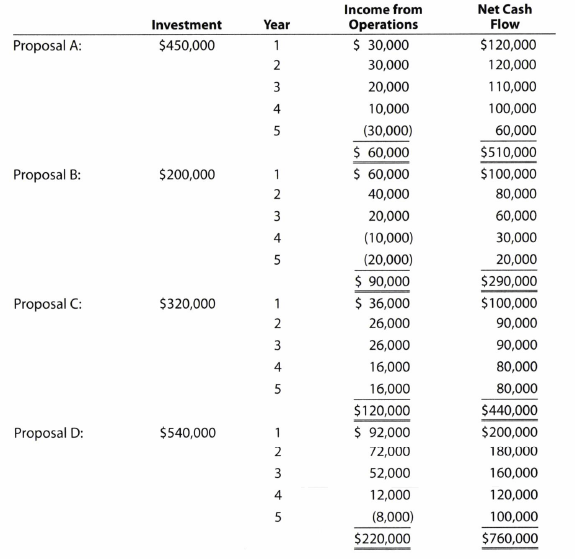

Clearcast Communications Inc. is considering allocating a limited amount of capital investment funds among four proposals. The amount of proposed investment, estimated income from operations, and net cash flow for each proposal are as follows:

The company's capital rationing policy requires a maximum cash payback period of three years. In addition, a minimum average

Instructions

- 1. Compute the cash payback period for each of the four proposals.

- 2. Giving effect to straight-line depreciation on the investments and assuming no estimated residual value, compute the average rate of return for each of the four proposals. Round to one decimal place.

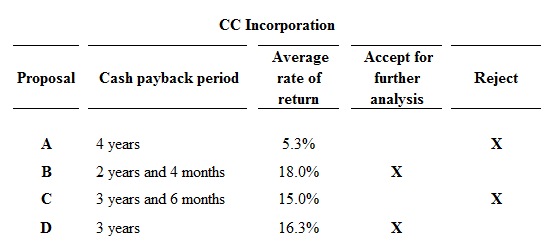

- 3. Using the following format, summarize the results of your computations in parts (1) and (2). By placing the calculated amounts in the first two columns on the left and by placing a check mark in the appropriate column to the right, indicate which proposals should be accepted for further analysis and which should be rejected.

- 4. For the proposals accepted for further analysis in part (3), compute the net present value. Use a rate of 12% and the present value of $1 table appearing in this chapter (Exhibit 2).

- 5. Compute the present value index for each of the proposals in part (4). Round to two decimal places.

- 6. Rank the proposals from most attractive to least attractive, based on the present values of net

cash flows computed in part (4). - 7. Rank the proposals from most attractive to least attractive, based on the present value indexes computed in part (5). Round to two decimal places.

- 8. Based on the analyses, comment on the relative attractiveness of the proposals ranked in parts (6) and (7).

1.

Cash payback method:

Cash payback period is the expected time period which is required to recover the cost of investment. It is one of the capital investment method used by the management to evaluate the long-term investment (fixed assets) of the business.

Average rate of return method:

Average rate of return is the amount of income which is earned over the life of the investment. It is used to measure the average income as a percent of the average investment of the business, and it is also known as the accounting rate of return.

The average rate of return is computed as follows:

Net present value method:

Net present value method is the method which is used to compare the initial cash outflow of investment with the present value of its cash inflows. In the net present value, the interest rate is desired by the business based on the net income from the investment, and it is also called as the discounted cash flow method.

Present value index:

Present value index is a technique, which is used to rank the proposals of the business. It is used by the management when the business has more investment proposals, and limited fund.

The present value index is computed as follows:

The cash payback period for the given proposals.

Explanation of Solution

The cash payback period for the given proposals is as follows:

Proposal A:

Initial investment=$450,000

| Cash payback period of Proposal A | ||||

| Year | Net cash flows | Cumulative net cash flows | ||

| 1 | 120,000 | 120,000 | ||

| 2 | 120,000 | 240,000 | ||

| 3 | 110,000 | 350,000 | ||

| 4 | 100,000 | 450,000 | ||

Table (1)

Hence, the cash payback period of proposal A is 4 years.

Proposal B:

Initial investment=$200,000

| Cash payback period of Proposal B | ||||

| Year | Net cash flows | Cumulative net cash flows | ||

| 1 | 100,000 | 100,000 | ||

| 2 | 80,000 | 180,000 | ||

| 4 months (1) | 20,000 | 200,000 | ||

Table (2)

Hence, the cash payback period of proposal B is 2 years and 4 months.

Working note:

1. Calculate the no. of months in the cash payback period:

Proposal C:

Initial investment=$320,000

| Cash payback period of Proposal C | ||||

| Year | Net cash flows | Cumulative net cash flows | ||

| 1 | 100,000 | 100,000 | ||

| 2 | 90,000 | 190,000 | ||

| 3 | 90,000 | 280,000 | ||

| 6 months (2) | 40,000 | 320,000 | ||

Table (3)

Hence, the cash payback period of proposal C is 3 years and 6 months.

Working note:

1. Calculate the no. of months in the cash payback period:

Proposal D:

Initial investment=$540,000

| Cash payback period of Proposal D | ||||

| Year | Net cash flows | Cumulative net cash flows | ||

| 1 | 200,000 | 200,000 | ||

| 2 | 180,000 | 380,000 | ||

| 3 | 160,000 | 540,000 | ||

Table (4)

Hence, the cash payback period of proposal D is 3 years.

2.

The average rate of return for the give proposals.

Explanation of Solution

The average rate of return for the given proposals is as follows:

Proposal A:

Hence, the average rate of return for Proposal A is 5.3%.

Proposal B:

Hence, the average rate of return for Proposal B is 18.0%.

Proposal C:

Hence, the average rate of return for Proposal C is 15.0%.

Proposal D:

Hence, the average rate of return for Proposal D is 16.3%.

3.

To indicate: The proposals which should be accepted for further analysis, and which should be rejected.

Answer to Problem 26.6BPR

The proposals which should be accepted for further analysis, and which should be rejected is as follows:

Figure (1)

Explanation of Solution

Proposals A and C are rejected, because proposal A and C fails to meet the required maximum cash back period of 3 years, and they has less rate of return than the other proposals. Hence, Proposals B and D are preferable.

4.

The net present value of preferred proposals.

Explanation of Solution

Calculate the net present value of the proposals which has 12% rate of return as follows:

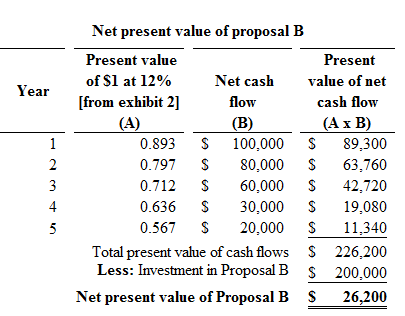

Proposal B:

Figure (2)

Hence, the net present value of proposal B is $26,200.

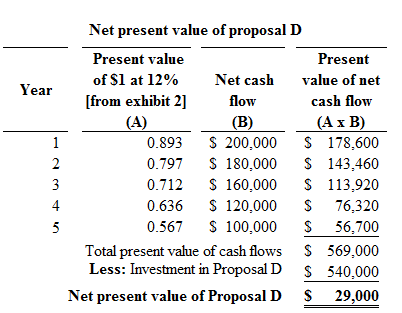

Proposal D:

Figure (3)

Hence, the net present value of proposal D is $29,000.

5.

To determine: The present value index for each proposal.

Explanation of Solution

The present value index for each proposal is as follows:

Proposal B:

Calculate the present value index for proposal B:

Hence, the present value index for proposal B is 1.13.

Proposal D:

Calculate the present value index for proposal D:

Hence, the present value index for proposal D is 1.05.

6.

To rank: The proposal from most attractive to least attractive, based on the present value of net cash flows.

Explanation of Solution

Proposals are arranged by rank is as follows:

| Proposals | Net present value | Rank |

| Proposal D | $ 29,000 | 1 |

| Proposal B | $ 26,200 | 2 |

Table (5)

7.

To rank: The proposal from most attractive to least attractive based on the present value of index.

Explanation of Solution

Proposals are arranged by rank is as follows:

| Proposals | Present value index | Rank |

| Proposal B | 1.13 | 1 |

| Proposal D | 1.05 | 2 |

Table (6)

8.

To analysis: The proposal which is favor to investment, and comment on the relative attractiveness of the proposals based on the rank.

Explanation of Solution

On the basis of net present value:

The net present value of Proposal B is $26,200, and Proposal D is $29,000. In this case, the net present value of proposal D is more than the net present value of proposal B. Hence, investment in Proposal D is preferable.

On the basis of present value index:

The present value index of Proposal B is 1.13, and the present value index of Proposal D is 1.05. In this case, Proposal B has the favorable present value index, because the present value index of Proposal B (1.13) is more than Proposal D (1.05). Thus, the investment in Proposal B is preferable (favorable).

Every business tries to get maximum profit with minimum investment. Hence, the cost of investment in Proposal B is less than the proposal D. Thus, investment in Proposal B is preferable.

Want to see more full solutions like this?

Chapter 26 Solutions

Working Papers, Chapters 1-17 for Warren/Reeve/Duchac's Accounting, 26th and Financial Accounting, 14th

- Can you explain this general accounting question using accurate calculation methods?arrow_forwardNonearrow_forwardJoe and Ethan form JH Corporation with the following consideration: Basis to Transferor FMV Number of Shares Issued From Joe Cash $50,000 $50,000 Installment Note $240,000 $350,000 40 From Ethan Inventory $60,000 $50,000 Equipment $125,000 $250,000 Patentable Invention $15,000 $300,000 60 The installment note has a face amount of $350,000 and was acquired last year from the sale of land held for investment purposes (adjusted basis of $240,000). As to these transactions, provide the following information: a. Joe’s recognized gain or loss. b. Joe’s basis in the Owl Corporation stock. c. JH’s basis in the installment note. d. Ethan’s recognized gain or loss. e. Ethan’s basis in…arrow_forward

- Can you solve this financial accounting problem using appropriate financial principles?arrow_forwardI need help solving this financial accounting question with the proper methodology.arrow_forwardI need the correct answer to this financial accounting problem using the standard accounting approach.arrow_forward

- Please provide the solution to this financial accounting question using proper accounting principles.arrow_forwardOn May 31, 2026, Oriole Company paid $3,290,000 to acquire all of the common stock of Pharoah Corporation, which became a division of Oriole. Pharoah reported the following balance sheet at the time of the acquisition: Current assets $846,000 Current liabilities $564,000 Noncurrent assets 2,538,000 Long-term liabilities 470,000 Stockholder's equity 2,350,000 Total assets $3,384,000 Total liabilities and stockholder's equity $3,384,000 It was determined at the date of the purchase that the fair value of the identifiable net assets of Pharoah was $2,914,000. At December 31, 2026, Pharoah reports the following balance sheet information: Current assets $752,000 Noncurrent assets (including goodwill recognized in purchase) 2,256,000 Current liabilities (658,000) Long-term liabilities (470,000) Net assets $1,880,000 It is determined that the fair value of the Pharoah division is $2,068,000.arrow_forwardOn May 31, 2026, Oriole Company paid $3,290,000 to acquire all of the common stock of Pharoah Corporation, which became a division of Oriole. Pharoah reported the following balance sheet at the time of the acquisition: Current assets $846,000 Current liabilities $564,000 Noncurrent assets 2,538,000 Long-term liabilities 470,000 Stockholder's equity 2,350,000 Total assets $3,384,000 Total liabilities and stockholder's equity $3,384,000 It was determined at the date of the purchase that the fair value of the identifiable net assets of Pharoah was $2,914,000. At December 31, 2026, Pharoah reports the following balance sheet information: Current assets $752,000 Noncurrent assets (including goodwill recognized in purchase) 2,256,000 Current liabilities (658,000) Long-term liabilities (470,000) Net assets $1,880,000 It is determined that the fair value of the Pharoah division is $2,068,000.arrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning

Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning