Videos

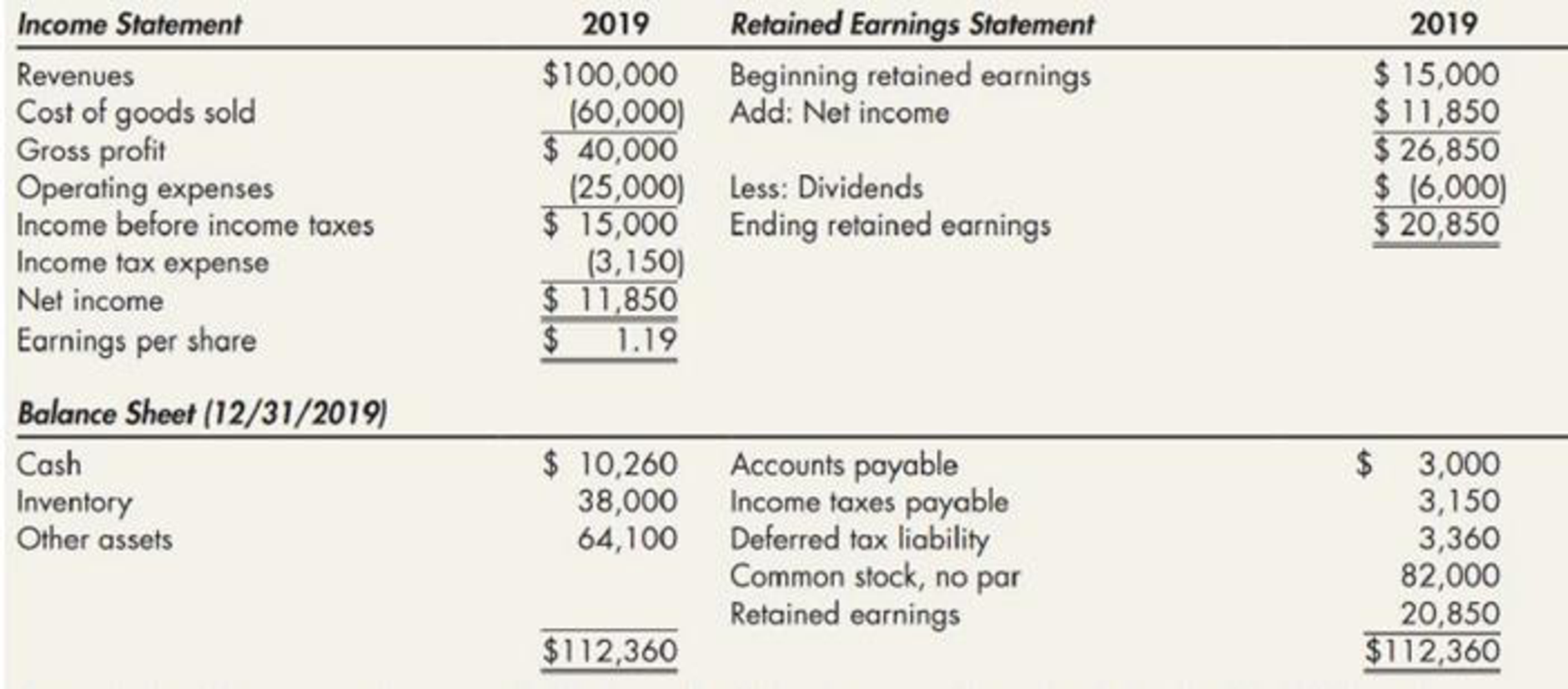

Koopman Company began operations on January 1, 2018, and uses they FIFO inventory method for financial reporting and the average cost inventory method for income taxes. At the beginning of 2020, Koopman decided to switch to the average cost inventory method for financial reporting. It had previously reported the following financial statement information for 2019:

An analysis of the accounting records discloses the following cost of goods sold under the FIFO and average cost inventory methods:

There are no indirect effects of the change in inventory method. Revenues for 2020 total $130,000; operating expenses for 2020 total $30,000. Koopman is subject to a 21% income tax rate in all years; it pays the income taxes payable of a current year in the first quarter of the next year. Koopman had 10,000 shares of common stock outstanding during all years; it paid dividends of $1 per share in 2020. At the end of 2020, Koopman had cash of $10,000, inventory of $24,000, other assets of $70,800, accounts payable of $4,500, and income taxes payable of $6,000. It desires to show financial statements for the current year and previous year in its 2020 annual report.

Required:

- 1. Prepare the

journal entry to reflect the change in methods at the beginning of 2020. Show supporting calculations. - 2. Prepare the 2020 financial statements. Notes to the financial statements are not necessary. Show supporting calculations.

1.

Journalize the cumulative effect of the retrospective adjustment on Company K’s prior year income that would be reported in 2020.

Explanation of Solution

Journal entry: Journal entry is a set of economic events which can be measured in monetary terms. These are recorded chronologically and systematically.

Debit and credit rules:

- Debit an increase in asset account, increase in expense account, decrease in liability account, and decrease in stockholders’ equity accounts.

- Credit decrease in asset account, increase in revenue account, increase in liability account, and increase in stockholders’ equity accounts.

Journalize the cumulative effect of the retrospective adjustment of decrease in pretax income, on Company K’s prior year income that would be reported in 2020.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| Retained Earnings | 12,640 | |||||

| Deferred Tax Liability | 3,360 | |||||

| Inventory | 16,000 | |||||

| (Record the cumulative effect of pretax income due to change from FIFO to average cost) | ||||||

Table (1)

Description:

- Retained Earnings is an equity account. Earnings decreased due to decrease in pretax income due to decrease in cumulative difference out of the change from FIFO to average cost, and a decrease in equity is debited.

- Deferred Tax Liability is a liability account. The obligation to pay taxes has decreased on saved income taxes, due to decrease in cumulative difference. The liability has decreased and a decrease in liability is debited.

- Inventory is an asset account. Since the cumulative difference has decreased due to change from FIFO to average cost flow, inventory has decreased, and a decrease in asset is credited.

Working Notes:

Compute the deferred tax liability amount.

Compute retained earnings amount.

2.

Prepare comparative financial statements for Company K for the year 2020.

Explanation of Solution

Income statement: The financial statement which reports revenues and expenses from business operations, and the result of those operations as net income or net loss for a particular time period is referred to as income statement.

Prepare comparative income statements of Company K for the year 2020.

| Company K | ||

| Comparative Income Statements | ||

| For the Years Ended December 31 | ||

| 2020 |

2019 (As Adjusted) | |

| Revenues | $130,000 | $100,000 |

| Cost of goods sold | (80,000) | (69,000) |

| Gross profit | 50,000 | 31,000 |

| Operating expenses | (30,000) | (25,000) |

| Income before income taxes | 20,000 | 6,000 |

| Income tax expense | (4,200) | (1,260) |

| Net income | $15,800 | $4,740 |

| Earnings per share: | ||

| Net income | $1.58 | $0.47 |

Table (2)

Working Notes:

Compute the income tax expense for 2020.

Compute the income tax expense for 2019.

Compute the earnings per share (EPS) for 2020.

Compute the earnings per share (EPS) for 2019.

Statement of retained earnings: This statement reports the beginning retained earnings and all the changes which led to ending retained earnings. Net income from income statement is added to and dividends is deducted from beginning retained earnings to arrive at the end result, ending retained earnings.

Prepare comparative statements of retained earnings of Company K for the year 2020.

| Company K | ||

| Comparative Statement of Retained Earnings | ||

| For the Years Ended December 31 | ||

| 2020 | 2019 | |

| Beginning unadjusted retained earnings | $20,850 | $15,000 |

| Less: Adjustment for the cumulative effect on prior years of retrospectively applying the average cost inventory method (net of taxes) | (12,640) | (5,530) |

| Adjusted beginning retained earnings | 8,210 | 9,470 |

| Add: Net income | 15,800 | 4,740 |

| 24,010 | 14,210 | |

| Less: Dividends | (10,000) | (6,000) |

| Ending retained earnings | $14,010 | $8,210 |

Table (3)

Working Notes:

Compute the adjustment value for 2020.

Compute the adjustment value for 2019.

Prepare comparative balance sheets of Company K for the year 2020.

| Company K | ||

| Comparative Balance Sheets | ||

| December 31 | ||

| 2020 |

2019 (As Adjusted) | |

| Assets | ||

| Cash | $9,910 | $10,260 |

| Inventory | 24,000 | 22,000 |

| Other assets | 70,800 | 64,100 |

| Total assets | $104,710 | $96,360 |

| Liabilities and Shareholders’ Equity | ||

| Accounts payable | $4,500 | $3,000 |

| Income taxes payable | 4,200 | 3,150 |

| Common stock, no par | 82,000 | 82,000 |

| Retained earnings | 14,010 | 8,210 |

| Total liabilities and shareholders’ equity | $104,710 | $96,360 |

Table (4)

Working Notes:

Refer to Table (2) for value and computation of income tax expense, which is the income taxes payable in 2020.

Compute adjusted inventory value for 2019.

Want to see more full solutions like this?

Chapter 22 Solutions

INTERM.ACCT.:REPORTING...-CENGAGENOWV2

- its net income?arrow_forwardSilver Star Manufacturing has $20 million in sales, an ROE of 15%, and a total assets turnover of 5 times. Common equity on the firm's balance sheet is 30% of its total assets. What is its net income? Round the answer to the nearest cent.arrow_forwardHi expert please give me answer general accounting questionarrow_forward

- Horizon Consulting started the year with total assets of $80,000 and total liabilities of $30,000. During the year, the business recorded $65,000 in service revenues and $40,000 in expenses. Additionally, Horizon issued $12,000 in stock and paid $18,000 in dividends. By how much did stockholders' equity change from the beginning of the year to the end of the year?arrow_forwardх chat gpt - Sea Content Content × CengageNOW × Wallet X takesssignment/takeAssignmentMax.co?muckers&takeAssignment Session Loca agenow.com Instructions Labels and Amount Descriptions Income Statement Instructions A-One Travel Service is owned and operated by Kate Duffner. The revenues and expenses of A-One Travel Service Accounts (revenue and expense items) < Fees earned Office expense Miscellaneous expense Wages expense Required! $1,480,000 350,000 36,000 875,000 Prepare an income statement for the year ended August 31, 2016 Labels and Amount Descriptions Labels Expenses For the Year Ended August 31, 20Y6 Check My Work All work saved.arrow_forwardEvergreen Corp. began the year with stockholders' equity of $350,000. During the year, the company recorded revenues of $500,000 and expenses of $320,000. The company also paid dividends of $30,000. What was Evergreen Corp.'s stockholders' equity at the end of the year?arrow_forward

- Evergreen corp.'s stockholders' equity at the end of the yeararrow_forwardHarrison Corp. reported earnings per share (EPS) of $15 in 2022 and paid dividends of $4 per share. The current market price per share is $90, and the book value per share is $65. What is Harrison Corp.'s price- earnings ratio (P/E ratio)?arrow_forwardEverest Manufacturing produces and sells a single product. The company has provided its contribution format income statement for March: • Sales (4,500 units): $135,000 • Variable expenses: $58,500 • Contribution margin: $76,500 • Fixed expenses: $50,000 • Net operating income: $26,500 If the company sells 5,200 units, what is the total contribution margin?arrow_forward

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning