Concept explainers

Videos

Equity as an Option and

- a. What is the current market value of the company’s equity?

- b. What is the current market value of the company’s debt?

- c. What is the company's continuously compounded cost of debt?

- d. The company has a new project available. The project has an NPV of $1,200,000. If the company undertakes the project, what will be the new market value of equity? Assume volatility is unchanged.

- e. Assuming the company undertakes the new project and does not borrow any additional funds, what is the new continuously compounded cost of debt? What is happening here?

a.

To compute: Current market value of the company’s equity.

Option Pricing:

Option pricing helps in determining the correct or fair price in the market. It is the value of one share on the basis of which option is traded. Black-Scholes is one of the pricing methods. Further, equity is also used as an option.

Explanation of Solution

Given,

Stock price is $9,050,000.

Exercise price is $10,000,000.

Risk free rate is 0.06.

Time to expire is 10.

Formula to calculate the value of equity by using Black Scholes model is,

Where,

- S is stock price.

- E is exercise price.

- R is risk free rate.

- T is time to expire.

Substitute $9,050,000 for S, $10,000,000 for E, 0.06for R, and 10for T.

Working Note:

Calculation of

Calculation of

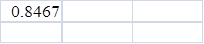

Hence, current market value of the company’s equity is $5,377,390.16.

b.

To compute: Current market value of the company’s debt.

Explanation of Solution

Given,

Value of company is $9,050,000.

Value of equity is $5,377,390.16.

Formula to calculate the value of debt is,

Substitute $9,050,000 as value of company and $5,377,390.16as value of equity.

Hence, current market value of company’s debt is $3,672,609.84.

c.

To compute: Company’s continuously compounded cost of debt.

Explanation of Solution

Given,

Value of debt is $3,672,609.84.

Face value is $10,000,000.

Time to expire is 10 years.

Formula to calculate the firm’s continuously cost of debt is,

Where,

- R is firm’s continuously cost of debt.

- t is maturity time.

Substitute $3,672,609.84as value of debt, $10,000,000 as face value and 10 for t.

Simplify the above equation.

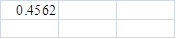

Hence, the company’s continuously cost of debt is 10.02%.

d.

To compute: New market value of equity.

Explanation of Solution

Given,

Exercise price is 10,000,000.

Risk free rate is 0.06.

Time to expire is 10 years.

Calculated stock price:

The stock price is $10,250,000.

Formula to calculate the value of equity by using Black Scholes model is,

Where,

- S is stock price.

- E is exercise price.

- R is risk free rate.

- T is time to expire.

Substitute $10,250,000for S, 10,000,000 for E, 0.06 for R, and 10 for T.

Working Note:

Calculation of

Calculation of

Calculate the revised stock price,

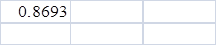

Hence, new market value of equity is $6,406,471.3.

e.

To compute: The new continuously compounded cost of debt.

Explanation of Solution

Given,

Value of company is $9,050,000.

Value of equity is $6,406,471.3.

Time to expire is 10 years.

Calculated value:

Value of equity is $6,406,471.3.

Value of the stock is $10,250,000.

Formula to calculate the value of debt is,

Substitute $10,250,000as value of company and $6,406,471.3 as value of equity.

Formula to calculate the new continuously cost of debt is,

Where,

- R is firm’s continuously cost of debt.

- t is maturity time.

Substitute $3,843,528.7 as value of debt, $10,000,000 as face value and 10 for t.

Simplify the above equation.

Hence, the company’s new continuously cost of debt is 9.56%.

Want to see more full solutions like this?

Chapter 22 Solutions

UPENN: LOOSE LEAF CORP.FIN W/CONNECT

- Explain why financial institutions generally engage in foreign exchange tradingactivities. Provide specific purposes or motivations behind such activities.arrow_forwardA. In 2008, during the global financial crisis, Lehman Brothers, one of the largest investment banks, collapsed and defaulted on its corporate bonds, causing significant losses for bondholders. This event highlighted several risks that investors in corporate bonds might face. What are the key risks an investor would encounter when investing in corporate bonds? Explain these risks with examples or academic references. [15 Marks]arrow_forwardTwo companies, Blue Plc and Yellow Plc, have bonds yielding 4% and 5.3%respectively. Blue Plc has a credit rating of AA, while Yellow Plc holds a BB rating. If youwere a risk-averse investor, which bond would you choose? Explain your reasoning withacademic references.arrow_forward

- B. Using the probabilities and returns listed below, calculate the expected return and standard deviation for Sparrow Plc and Hawk Plc, then justify which company a risk- averse investor might choose. Firm Sparrow Plc Hawk Plc Outcome Probability Return 1 50% 8% 2 50% 22% 1 30% 15% 2 70% 20%arrow_forward(2) Why are long-term bonds more susceptible to interest rate risk than short-term bonds? Provide examples to explain. [10 Marks]arrow_forwardDon't used Ai solutionarrow_forward

- Don't used Ai solutionarrow_forwardScenario one: Under what circumstances would it be appropriate for a firm to use different cost of capital for its different operating divisions? If the overall firm WACC was used as the hurdle rate for all divisions, would the riskier division or the more conservative divisions tend to get most of the investment projects? Why? If you were to try to estimate the appropriate cost of capital for different divisions, what problems might you encounter? What are two techniques you could use to develop a rough estimate for each division’s cost of capital?arrow_forwardScenario three: If a portfolio has a positive investment in every asset, can the expected return on a portfolio be greater than that of every asset in the portfolio? Can it be less than that of every asset in the portfolio? If you answer yes to one of both of these questions, explain and give an example for your answer(s). Please Provide a Referencearrow_forward

- Hello expert Give the answer please general accountingarrow_forwardScenario 2: The homepage for Coca-Cola Company can be found at coca-cola.com Links to an external site.. Locate the most recent annual report, which contains a balance sheet for the company. What is the book value of equity for Coca-Cola? The market value of a company is (# of shares of stock outstanding multiplied by the price per share). This information can be found at www.finance.yahoo.com Links to an external site., using the ticker symbol for Coca-Cola (KO). What is the market value of equity? Which number is more relevant to shareholders – the book value of equity or the market value of equity?arrow_forwardFILE HOME INSERT Calibri Paste Clipboard BIU Font A1 1 2 34 сл 5 6 Calculating interest rates - Excel PAGE LAYOUT FORMULAS DATA 11 Α΄ Α΄ % × fx A B C 4 17 REVIEW VIEW Alignment Number Conditional Format as Cell Cells Formatting Table Styles▾ Styles D E F G H Solve for the unknown interest rate in each of the following: Complete the following analysis. Do not hard code values in your calculations. All answers should be positive. 7 8 Present value Years Interest rate 9 10 11 SA SASA A $ 181 4 $ 335 18 $ 48,000 19 $ 40,353 25 12 13 14 15 16 $ SA SA SA A $ Future value 297 1,080 $ 185,382 $ 531,618arrow_forward

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning