Concept explainers

Videos

Calen Company manufactures and sells three products in a factory of three departments. Both labor and machine time are applied to the products as they pass through each department. The nature of the machine processing and of the labor skills required in each department is such that neither machines nor labor can be switched from one department to another.

Calen’s management is attempting to plan its production schedule for the next several months. The planning is complicated by the fact that labor shortages exist in the community and some machines will be down several months for repairs.

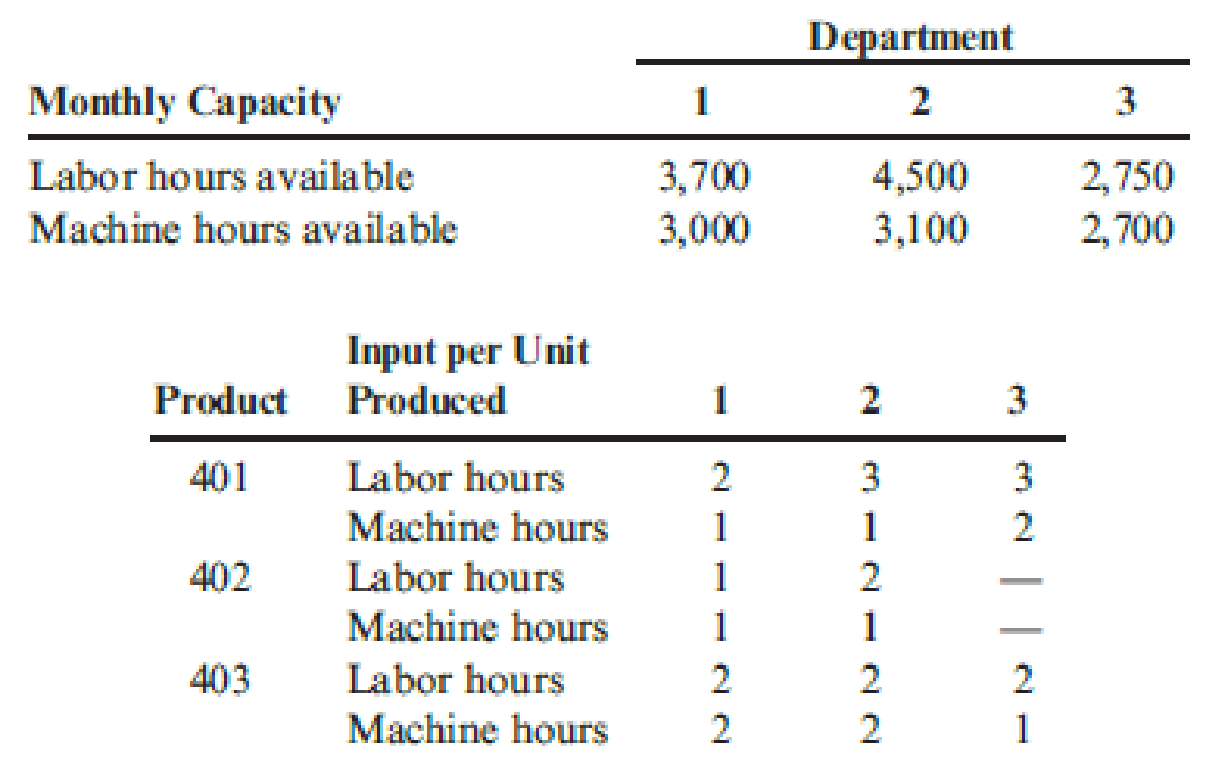

Following is information regarding available machine and labor time by department and the machine hours and direct labor hours required per unit of product. These data should be valid for at least the next six months.

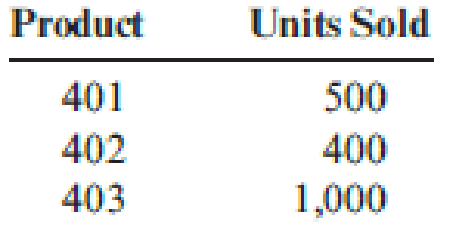

Calen believes that the monthly demand for the next six months will be as follows:

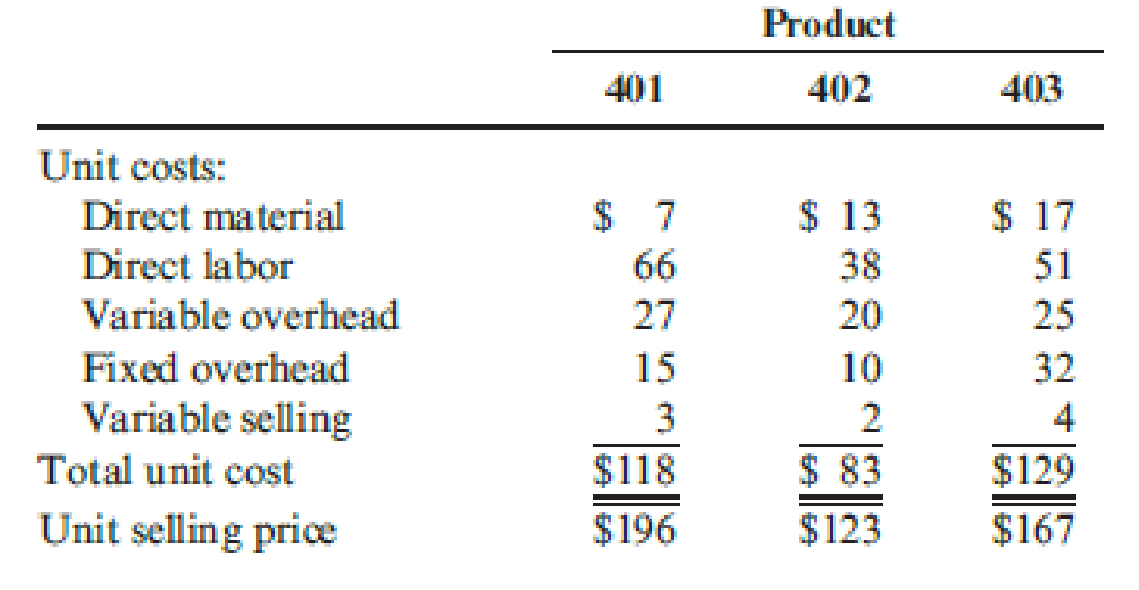

Inventory levels will not be increased or decreased during the next six months. The unit cost and price data for each product are as follows:

Required:

- 1. Calculate the monthly requirement for machine hours and direct labor hours for producing Products 401, 402, and 403 to determine whether or not the factory can meet the monthly sales demand.

- 2. Determine the quantities of 401, 402, and 403 that should be produced monthly to maximize profits. Prepare a schedule that shows the contribution to profits of your product mix.

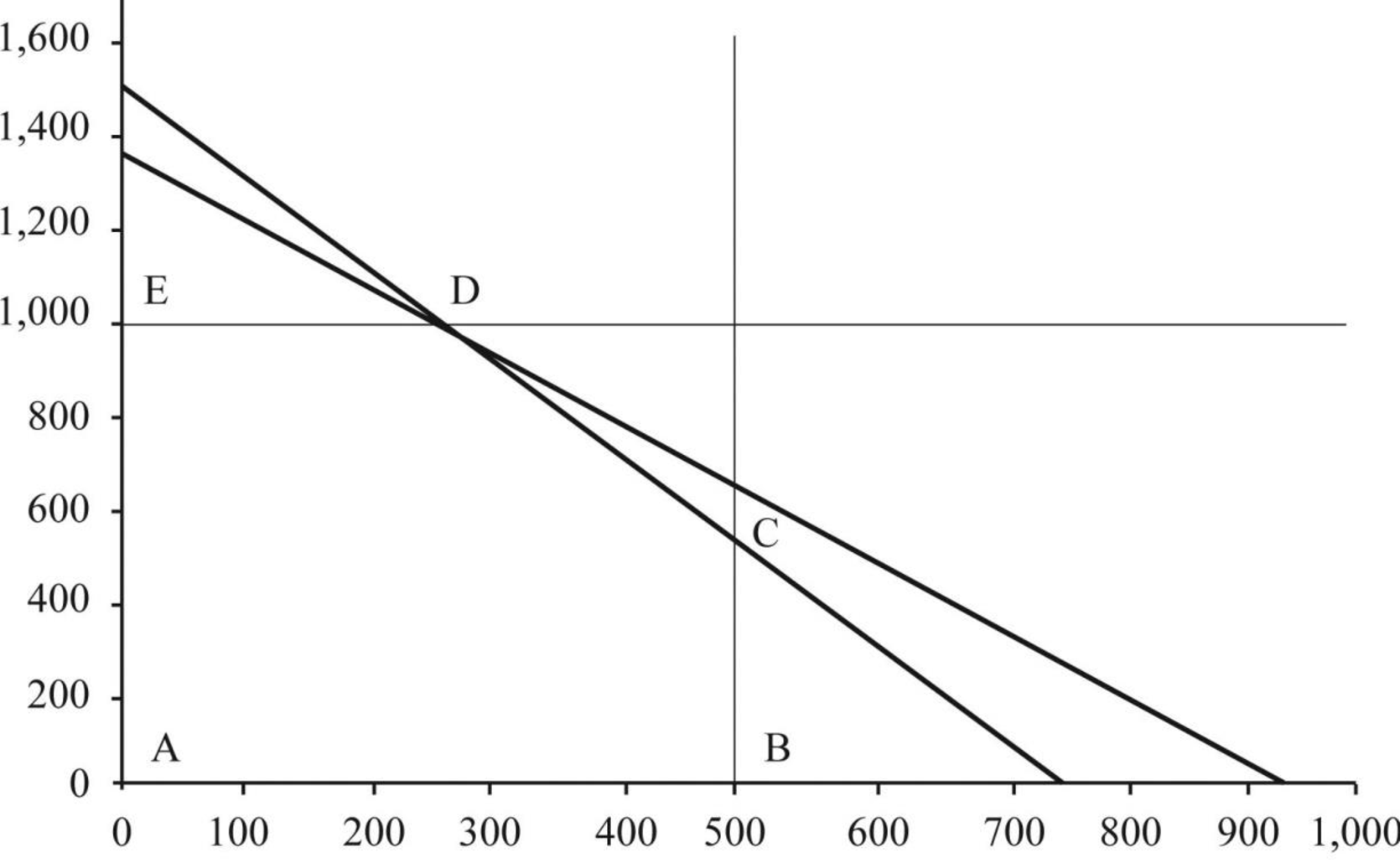

- 3. Assume that the machine hours available in Department 3 are 1,500 instead of 2,700. Calculate the optimal monthly product mix using the graphing approach to linear programming. Prepare a schedule that shows the contribution to profits from this optimal mix. (CMA adapted)

1.

Calculate the monthly machine hours and direct labor hours for product 401, 402 and 403 and indicate whether the factory can meet monthly sales demand or not.

Explanation of Solution

Contribution margin: Contribution margin is a measurement of performance where only revenue and variable costs are taken into consideration. Hence, this measurement is useful in the evaluation of the probable outcomes of decisions including pricing decisions and other marketing strategies that affect primarily revenue and variable costs.

Calculate the monthly machine hours and direct labor hours for product 401, 402 and 403 and indicate whether the factory can meet monthly sales demand or not as follows:

Direct labor hours:

| Particulars | Department 1 | Department 2 | Department 3 | Total |

| Product 401: | ||||

| Labor hours per unit (A) | 2 | 3 | 3 | |

| Unit sold (B) | 500 units | 500 units | 500 units | |

| Labor hours for Product 401 | 1,000 | 1,500 | 1,500 | 4,000 hours |

| Product 402: | ||||

| Labor hours per unit (A) | 1 | 2 | 0 | |

| Unit sold (B) | 400 units | 400 units | 400 units | |

| Labor hours for Product 401 | 400 | 800 | 0 | 1,200 hours |

| Product 403: | ||||

| Labor hours per unit (A) | 2 | 2 | 2 | |

| Unit sold (B) | 1,000 units | 1,000 units | 1,000 units | |

| Labor hours for Product 401 | 2,000 | 2,000 | 2,000 | 6,000 hours |

| Totals | 3,400 hours | 4,300 hours | 3,500 hours | 11,200 hours |

Table (1)

Machine hours:

| Particulars | Department 1 | Department 2 | Department 3 | Total |

| Product 401: | ||||

| Machine hours per unit (A) | 1 | 1 | 2 | |

| Unit sold (B) | 500 units | 500 units | 500 units | |

| Machine hours for Product 401 | 500 | 500 | 1,000 | 2,000 hours |

| Product 402: | ||||

| Machine hours per unit (A) | 1 | 1 | 0 | |

| Unit sold (B) | 400 units | 400 units | 400 units | |

| Machine hours for Product 401 | 400 | 400 | 0 | 800 hours |

| Product 403: | ||||

| Machine hours per unit (A) | 2 | 2 | 1 | |

| Unit sold (B) | 1,000 units | 1,000 units | 1,000 units | |

| Machine hours for Product 401 | 2,000 | 2,000 | 1,000 | 5,000 hours |

| Totals | 2,900 hours | 2,900 hours | 2,000 hours | 7,800 hours |

Table (2)

In this case, company can meet the demand in all departments expect Department 3, because available labor hours for department 3 (2,750 hours) is less than the monthly requirement of 3,500 hours.

2.

Prepare a schedule of contribution to profits for the given product mix.

Explanation of Solution

Prepare a schedule of contribution to profit for the given product mix as follows:

In this case, department 3 in product 401 has more labor hour than the actual available hours. Hence, after meeting the demand the additional labor hours of Department 3 is used to produce the product 1 as a subsidy of department 1. Thus, department 1 would produce only 250 units

| Particulars | Optimal output (A) | Contribution margin per unit (B) |

Total contribution |

| Product 401 | 250 units | $93 (1) | $23,250 |

| Product 402 | 400 units | $50 (2) | $20,000 |

| Product 403 | 1,000 units | $70 (3) | $70,000 |

| Total contribution margin | $113,250 | ||

Table (3)

Working note (1):

Calculate the contribution margin per unit for product 401.

Working note (2):

Calculate the contribution margin per unit for product 402.

Working note (3):

Calculate the contribution margin per unit for product 403.

3.

Compute the optimal monthly product mix using the graphical approach to linear program and calculate the contribution profit for the optimal mix.

Explanation of Solution

Compute the optimal monthly product mix using the graphical approach to linear program and calculate the contribution profit for the optimal mix as follows:

Machine constraint:

Direct labor constraint:

Demand constraint for each product:

Note: X denotes number of product produced in Product 401, Y denotes number of product produced in Product 402, and Z denotes number of product produced in Product 403.

| Corner point | X-value | Y-value | W-value | |

| A | 0 | 0 | 400 | $20,000 |

| B | 500 | 0 | 400 | $66,500 |

| C | 500 | 500 | 400 | $101,500 |

| D | 250 | 1,000 | 400 | $113,250 |

| E | 0 | 1,000 | 400 | $90,000 |

Table (1)

Figure (1)

Hence, contribution margin under optimal output is $113,250.

Want to see more full solutions like this?

Chapter 20 Solutions

Cornerstones of Cost Management (Cornerstones Series)

- Terri Ronsin had recently been transferred to the Home Security Systems Division of National Home Products. Shortly after taking over her new position as divisional controller, she was asked to develop the division’s predetermined overhead rate for the upcoming year. The accuracy of the rate is important because it is used throughout the year and any underapplied or overapplied overhead is closed out to Cost of Goods Sold at the end of the year. National Home Products uses direct labor-hours in all of its divisions as the allocation base for manufacturing overhead. To compute the predetermined overhead rate, Terri divided her estimate of the total manufacturing overhead for the coming year by the production manager’s estimate of the total direct labor-hours for the coming year. She took her computations to the division’s general manager for approval but was quite surprised when he suggested a modification in the allocation base. Her conversation with the general manager of the Home…arrow_forwardThe Gilster Company, a machine tooling firm, has several plants. One plant, located in St. Cloud, Minnesota, uses a job order costing system for its batch production processes. The St. Cloud plant has two departments through which most jobs pass. Plant-wide overhead, which includes the plant manager’s salary, accounting personnel, cafeteria, and human resources, is budgeted at $250,000. During the past year, actual plantwide overhead was $230,000. Each department’s overhead consists primarily of depreciation and other machine-related expenses. Selected budgeted and actual data from the St. Cloud plant for the past year are as follows. Department A Department B Budgeted department overhead (excludes plantwide overhead) $ 108,000 $ 329,000 Actual department overhead 120,000 344,000 Expected total activity: Direct labor hours 44,000 10,000 Machine-hours 18,000 47,000 Actual activity:…arrow_forwardThe Gilster Company, a machine tooling firm, has several plants. One plant, located in St. Cloud, Minnesota, uses a job order costing system for its batch production processes. The St. Cloud plant has two departments through which most jobs pass. Plant-wide overhead, which includes the plant manager’s salary, accounting personnel, cafeteria, and human resources, is budgeted at $250,000. During the past year, actual plantwide overhead was $230,000. Each department’s overhead consists primarily of depreciation and other machine-related expenses. Selected budgeted and actual data from the St. Cloud plant for the past year are as follows. Department A Department B Budgeted department overhead (excludes plantwide overhead) $ 108,000 $ 329,000 Actual department overhead 120,000 344,000 Expected total activity: Direct labor hours 44,000 10,000 Machine-hours 18,000 47,000 Actual activity:…arrow_forward

- The Gilster Company, a machine tooling firm, has several plants. One plant, located in St. Cloud, Minnesota, uses a job order costing system for its batch production processes. The St. Cloud plant has two departments through which most jobs pass. Plant-wide overhead, which includes the plant manager’s salary, accounting personnel, cafeteria, and human resources, is budgeted at $250,000. During the past year, actual plantwide overhead was $230,000. Each department’s overhead consists primarily of depreciation and other machine-related expenses. Selected budgeted and actual data from the St. Cloud plant for the past year are as follows. Department A Department B Budgeted department overhead (excludes plantwide overhead) $ 108,000 $ 329,000 Actual department overhead 120,000 344,000 Expected total activity: Direct labor hours 44,000 10,000 Machine-hours 18,000 47,000 Actual activity:…arrow_forwardThe Gilster Company, a machine tooling firm, has several plants. One plant, located in St. Cloud, Minnesota, uses a job order costing system for its batch production processes. The St. Cloud plant has two departments through which most jobs pass. Plant-wide overhead, which includes the plant manager’s salary, accounting personnel, cafeteria, and human resources, is budgeted at $250,000. During the past year, actual plantwide overhead was $230,000. Each department’s overhead consists primarily of depreciation and other machine-related expenses. Selected budgeted and actual data from the St. Cloud plant for the past year are as follows. Department A Department B Budgeted department overhead (excludes plantwide overhead) $ 108,000 $ 329,000 Actual department overhead 120,000 344,000 Expected total activity: Direct labor hours 44,000 10,000 Machine-hours 18,000 47,000 Actual activity:…arrow_forwardTerri Ronsin had recently been transferred to the House Security Division of National Home products. Shortly after taking over her new position as individual controller, she was asked to develop the divisions' predetermined overhead rate for the upcoming year. The accuracy of the rate is important because it is used throughout the year and any over applied or under applied overhead is closed out to Cost of Goods Sold at the end of the year. National Home Products uses direct labor -hours in all of its divisions as the allocation base for manufacturing overhead. To compute the pretermined overhead rate, Terri divided her estimate of the total manufacturing overhead for the coming year by the production manager's estimate of the total direct labor hours for the coming year. She took her computations to the division's general manager for approval but was quite surprised when he suggested a modification in the base. Her conversation with the general manager…arrow_forward

- Jasper Company, a machine tooling firm, has several plants. One plant, located in Saint Cloud, Minnesota, uses a job order costing system for its batch production processes. The Saint Cloud plant has two departments through which most jobs pass. Plantwide overhead, which includes the plant manager's salary, accounting personnel, cafeteria, and human resources, is budgeted at $360,000. During the past year, actual plantwide overhead was $340,000. Each department's overhead consists primarily of depreciation and other machine-related expenses. Selected budgeted and actual data from the Saint Cloud plant for the past year are as follows: Budgeted department overhead (excludes plantwide overhead) Actual department overhead Expected total activity: Direct labor hours Machine-hours Actual activity: Direct labor hours Machine-hours Department A Department B $ 100,000 $ 282,000 120,000 302,000 38,000 20,000 20,000 47,000 39,000 18,700 20,800 49,000 Mc Graw Hill For the coming year, the…arrow_forwardJasper Company, a machine tooling firm, has several plants. One plant, located in Saint Cloud, Minnesota, uses a job order costing system for its batch production processes. The Saint Cloud plant has two departments through which most jobs pass. Plantwide overhead, which includes the plant manager's salary, accounting personnel, cafeteria, and human resources, is budgeted at $360,000. During the past year, actual plantwide overhead was $340,000. Each department's the Saint Cloud plant for the past year are as follows: overhead consists primarily of depreciation and other machine-related expenses. Selected budgeted and actual data from Department A Department B Budgeted department overhead (excludes plantwide overhead) $ 100,000 $ 282,000 Actual department overhead Expected total activity: Direct labor hours Machine-hours Actual activity: Direct labor hours Machine-hours 120,000 302,000 38,000 20,000 20,000 47,000 39,000 20,800 18,700 49,000 For the coming year, the accountants at the…arrow_forwardThe Hy-Tech Services Corporation employs researchers based in countries around the world. Employee time is the basis upon which charges to many customers are made. The geographically dispersed nature of its operations makes it extremely difficult for the payroll staff to collect time records, so the management team authorizes the design of an in-house, web-based timekeeping system. The project team incurs the following costs: Concept design - 2,500; Evaluation of design alternatives - 3,700; Determination of required technology - 8,100; Final selection of alternatives - 1,400; Software design - 28,000; Software coding - 42,000; Quality assurance testing - 30,000; Data conversion costs - 3,900; Training - 14,000; Overhead allocation - 6,900; General and administrative costs - 11,200; Ongoing maintenance costs - 6,000. Required: Compute the amount of intangible asset recognized from the given transactionsarrow_forward

- Kingsport Containers Company makes a single product that is subject to wide seasonal variations in demand. The company uses a job-order costing system and computes plantwide predetermined overhead rates on a quarterly basis using the number of units to be produced as the allocation base. Its estimated costs, by quarter, for the coming year are given below: Management finds the variation in quarterly unit product costs to be confusing and difficult to work with. It has been suggested that the problem lies with manufacturing overhead because it is the largest element of total manufacturing cost. Accordingly, you have been asked to find a more appropriate way of assigning manufacturing overhead cost to units of product.Required:1. Assuming the estimated variable manufacturing overhead cost per unit is $2.00, what must be the estimated total fixed manufacturing overhead cost per quarter?2. Assuming the assumptions about cost behavior from the first three quarters hold constant, what is the…arrow_forwardHobart, Evans, and Nix is a small law firm that contains 10 partners and 12 support persons. The firm employs a job-order costing system to accumulate costs chargeable to each client, and it is organized into two departments - the Research and Documents Department and the Litigation Department. The firm uses predetermined overhead rates to charge the costs of these departments to its clients. At the beginning of the year, the firm's management made the following estimates for the year:Department Research and Documents Litigation Research-hours 31,000 — Direct attorney-hours 11,800 23,400 Legal forms and supplies £ 21,100 £ 6,700 Direct lawyer cost 593,300 1,186,700 Departmental overhead cost 930,000 474,680 The predetermined overhead rate in the Research and Documents Department is based on research-hours, and the rate in the Litigation Department is based on direct lawyer cost.The costs charged to each client are made up of three elements: legal forms and supplies used, direct lawyer…arrow_forwardThe management of Garn Corporation would like to investigate the possibility of basing its predetermined overhead rate on activity at capacity rather than on the estimated activity for the coming year. The Corporation's controller has provided an example to illustrate how this new system would work. In this example, the allocation base is machine-hours and the estimated activity for the upcoming year is 59,400 machine-hours. Capacity is 78,400 machine-hours. All of the manufacturing overhead is fixed and is $3,136,000 per year within the range of 59,400 to 78,400 machine-hours. If the Corporation bases its predetermined overhead rate on capacity but the actual level of activity for the year turns out to be 59,900 machine-hours, the cost of unused capacity shown on the income statement prepared for internal management purposes would be closest to: Multiple Choice $26.177 $766,177 $740,000 $26,397arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub