Concept explainers

Videos

Devon Bishop, age 45, is single. He lives at 1507 Rose Lane, Albuquerque, NM 87131. His Social Security number is 111-11-1117. Devon does not want $3 to go to the Presidential Election Campaign Fund.

Devon’s wife, Ariane, passed away in 2014. Devon’s son, Tom, who is age 18, resides with Devon. Tom’s Social Security number is 123-45-6788.

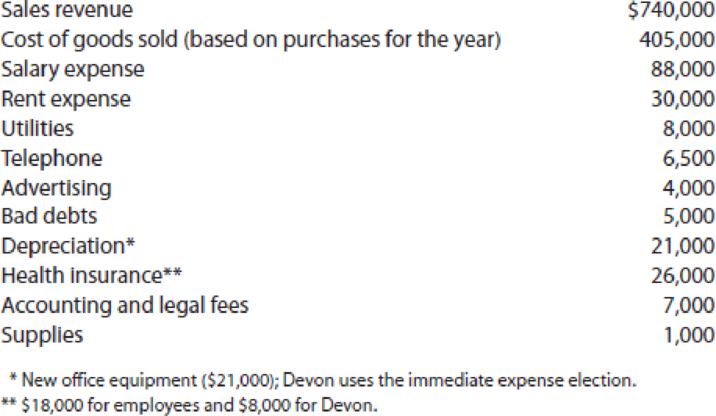

Devon owns a sole proprietorship for which he uses the accrual method of accounting and maintains no inventory; the business operates as Devon’s Copy Shop, 422 E. Main Street, Albuquerque, NM 87131, IRS business activity code: 453990. His revenues and expenses for 2018 are as follows.

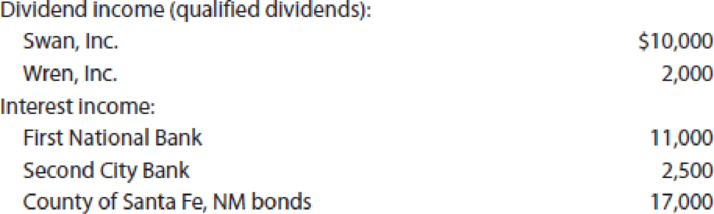

Other income received by Devon includes the following.

During the year, Devon and his sole proprietorship were involved in the following property transactions. Stock transactions were reported to Devon on Form 1099–B; basis was not reported to the IRS.

- a. Sold Blue, Inc. stock for $45,000 on March 12, 2018. He had purchased the stock on September 5, 2015, for $50,000.

- b. Received an inheritance of $300,000 from his uncle, Henry. Devon used $200,000 to purchase Green, Inc. stock on May 15, 2018, and invested $100,000 in Gold, Inc. stock on May 30, 2018.

- c. Received Orange, Inc. stock worth $9,500 as a gift from his aunt, Jane, on June 17, 2018. Her adjusted basis for the stock was $5,000. No gift taxes were paid on the transfer. Jane had purchased the stock on April 1, 2012. Devon sold the stock on July 1, 2018, for $22,000.

- d. On July 15, 2018, Devon sold one-half of the Green, Inc. stock for $40,000.

- e. Devon was notified on August 1, 2018, that Yellow, Inc. stock he purchased from a colleague on September 1, 2017, for $52,500 had become worthless. Although he understood that investing in Yellow was risky, Devon did not anticipate that the corporation would declare bankruptcy.

- f. On August 15, 2018, Devon received a parcel of land in Phoenix worth $220,000 in exchange for a parcel of land he owned in Tucson. Because the Tucson parcel was worth $245,000, he also received $25,000 cash. Devon’s adjusted basis for the Tucson parcel was $210,000. He originally purchased it on September 18, 2015.

- g. On December 1, 2018, Devon sold the condominium in which he had been living for the past 20 years (1844 Lighthouse Lane, Albuquerque, NM 87131) and moved into a rented townhouse. The sales price was $480,000, selling expenses were $28,500, and repair expenses related to the sale were $9,400. Devon purchased the condominium for $180,000.

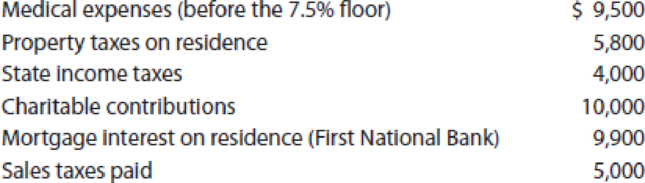

Devon’s potential itemized deductions, exclusive of the aforementioned information, are as follows.

During the year, Devon makes estimated Federal income tax payments of $35,000.

Compute Devon’s lowest net tax payable or refund due for 2018 assuming that he makes any available elections that will reduce the tax. If you use tax forms for your computations, you will need Form 1040 and its Schedules 1, 4, 5, A, B, C, D, and SE and Forms 4562, 8824, and 8949. Suggested software: ProConnect Tax Online.

Compute the lowest net tax payable or refund due for 2018.

Explanation of Solution

Compute the lowest net tax payable or refund due for 2018:

| Particulars | Amount ($) |

| Business income (Note 1) | $146,500 |

| Dividend Income | $12,000 |

| Interest income | $13,500 |

| Capital loss (Note 3) | ($3,000) |

| Self employment tax deduction (Note 4) | ($9,923) |

| Self employed health insurance (Note 4) | ($8,000) |

| Adjusted gross income | $151,077 |

| Less: Itemized deductions (Note 6) | ($29,900) |

| Deduction for qualifies business income (Note 7) | ($21,835) |

| Taxable income | $99,342 |

| Income tax computation: | |

| Tax on taxable income of $99,342 (Note 8) | $15,656 |

| Self employment tax (Note 4) | $19,845 |

| Tax liability before prepayments and credits | $35,501 |

| Less: Estimated tax payments | ($35,000) |

| Dependent tax credit (Note 9) | ($500) |

| Net tax payable (or refund) for 2018 | $1 |

Table (1)

Therefore, Net tax payable for the year 2018 is $1

Working note 1: Compute the business income:

| Particulars | Amount ($) | Amount ($) |

| Sales revenue | $740,000 | |

| Less: Cost of goods sold | ($405,000) | |

| Gross profit | $335,000 | |

| Less: Salary expense | $88,000 | |

| Rent expense | $30,000 | |

| Utilities | $8,000 | |

| Telephone | $6,500 | |

| Advertising | $4,000 | |

| Bad debts | $5,000 | |

| Depreciation | $21,000 | |

| Health insurance for employees | $18,000 | |

| Accounting and legal fees | $7,000 | |

| Supplies | $1,000 | ($188,500) |

| Net income | $146,500 |

Table (2)

Note: Out of the health insurance payments, only the $18,000 of health insurance paid for employees is allowed as a deduction while computing the net income of the sole proprietorship. The $8,000 paid for Person D eligible as a deduction for AGI.

Working Note 2: The amount of $17,000 interest on the County of SF, NM bonds is expelled from the gross income.

Working note 3: Compute the capital loss:

Compute the recognized gain or loss for each item:

Item a:

| Particulars | Amount ($) |

| Amount realized | $45,000 |

| Less: Adjusted basis | ($50,000) |

| Realized loss | ($5,000) |

| Recognized loss (long-term capital loss) | ($5,000) |

Table (3)

Item b: The $300,000 inheritance is barred from Person D’s gross income. His adjusted basis for Incorporation GR’s stock is the cost of $200,000, and his adjusted basis for Incorporation G’s, stock is $100,000.

Item c: Gifts are expelled from Person D’s gross income. His adjusted basis for the Incorporation O’s stock is a postpone basis of $5,000. His holding period also is a postpone holding period (i.e., it comprises Person J’s holding period, which began April 1, 2012).

| Item c. | |

| Amount realized | $22,000 |

| Less: Adjusted basis | ($5,000) |

| Realized gain | $17,000 |

| Recognized gain (long-term capital gain) | $17,000 |

Table (4)

Item d:

| Item d. | |

| Amount realized | $40,000 |

| Less: Adjusted basis | ($100,000) |

| Realized loss | ($60,000) |

| Recognized loss (short-term capital loss) | ($60,000) |

Table (5)

Item e:

| Item e. | |

| Amount realized | $0 |

| Less: Adjusted basis | ($52,500) |

| Realized loss | ($52,500) |

| Recognized loss (long-term capital loss) | ($52,500) |

Table (6)

Item f:

| Item f. | |

| Amount realized | $245,000 |

| Less: Adjusted basis | ($210,000) |

| Realized gain | $35,000 |

| Recognized gain (long-term capital gain) | $25,000 |

Table (7)

Item g:

| Item g. | |

| Amount realized | $451,500 |

| Less: Adjusted basis | ($180,000) |

| Realized gain | $271,500 |

| § 121 exclusion | ($250,000) |

| Recognized gain (long-term capital gain) | $21,500 |

Table (8)

Person D eligible’s for the § 121 exclusion since he has owned and occupied the residence as his principal residence throughout at least two of the five years prior to the date of sale. Therefore, his realized gain of $271,500 is decreased to $21,500.

Repair expenses of amount $9,400 are neither capitalizable nor allowed as deduction.

Person D’s capital gains and losses are abridged as follows:

| Long term capital gains: | ||

| Incorporation O’s stock | $17,000 | |

| Residence | 21,500 | |

| T land | 25,000 | $63,500 |

| Long-term capital losses: | ||

| Incorporation B’s stock | ($5,000) | |

| Incorporation Y stock | ($52,500) | ($57,500) |

| Net long-term capital gain | $6,000 | |

| Short-term capital loss: | ||

| Incorporation G’s stock | ($60,000) | |

| Net capital loss | ($54,000) |

Table (9)

Out of $54,000 capital loss, only $3,000 of the net capital loss can be allowed as a deduction in the year 2018. The balance amount of $51,000 is carried forwarded to the following year (2019).

Working note 4: Compute the self-employment tax:

| Particulars | Amount ($) |

| Step 1: Net profit from Schedule C (line 31 of Schedule C) | $146,500 |

| Step 2: Multiply step 1 amount by 92.35% | $135,293 |

| Step 3: If the amount in step 2 is $128,400 or less, multiply the step 2 amount by 15.3%. If the step 2 amount is more than $128,400, multiply the excess of the step 2 amount ($135,293) over $128,400 by 2.9% and add $19,645.20. This is the self-employment tax. | $19,845.10 |

Table (10)

The deduction for AGI for part of the self-employment tax is $9,923 (50% of $19,845.10).

Working note 5: Out of the amount $8,000 of health insurance premiums paid for Person D 100% is allowed as a deduction for AGI.

Working note 6: Compute the itemized deductions:

| Itemized deductions: | |

| Medical expenses | $0 |

| Property taxes and sales taxes (greater than $4,000 state income taxes); limited to $10,000 | $10,000 |

| Charitable contributions | $10,000 |

| Mortgage interest | $9,900 |

| Total itemized deductions | $29,900 |

Table (11)

Working note 7: Person D’s taxable income previous to the eligible business income deduction is $121,177

- (a) 20% of qualified business income $25,175

- (b) 20% of taxable income prior to the qualified business income deduction, decreased by any net capital gain (including any qualified dividends) is $21,835

Working note 8: Compute the taxable income:

All of Person D’s qualified dividends of $12,000 are taxed at 15% as his taxable income net of the qualified dividends goes above $51,700 and the head-of-household zero percent rate thresholds.

| Particulars | Amount ($) |

| Taxable income | $99,342 |

| Qualified dividends | ($12,000) |

| Portion of taxable income taxed at regular tax rates | $87,342 |

| Tax on qualified dividends | $1,800 |

| Tax on $87,342 from the 2018 Tax Tables (Head of Household) | 13,856 |

| Tax on taxable income | $15,656 |

Table (12)

Working note 9: Determine the dependent tax credit:

The child tax credit is not available (As Person T is 18, hence he is not eligible as child). But, Person T does qualify for a dependent tax credit of $500.

Want to see more full solutions like this?

Chapter 15 Solutions

Individual Income Taxes

- Eminent Apparel sold merchandise inventory on account at a price of $18,000 with payment terms of 3/10, n/30. The merchandise cost of Eminent Apparel is $12,000. If the customer paid for the merchandise 7 days after receiving the invoice, how much cash was collected by Eminent Apparel? a. $12,000 b. $17,460 c. $11,640 d. $18,000arrow_forwardPlease given correct optionarrow_forwardBy year end the firm's overhead was?arrow_forward

- Can you help me with accounting questionsarrow_forwardDuring its first year, Yutsang Enterprises showed a $22 per-unit profit under absorption costing but would have reported a total profit of $20,000 less under variable costing. Suppose production exceeded sales by 600 units and an average contribution margin of 58% was maintained. a. What is the fixed cost per unit? b. What is the sales price per unit? c. What is the variable cost per unit? d. What is the unit sales volume if total profit under absorption costing was $240,000?arrow_forwardWood Manufacturing uses a job-order costing system and a predetermined overhead rate based on direct labor-hours to apply manufacturing overhead to jobs. Manufacturing overhead cost and direct labor hours were estimated at $120,000 and 50,000 hours, respectively, for the year. In August, Job #527 was completed at a cost of $6,200 in direct materials and $3,000 in direct labor. The labor rate is $7 per hour. By the end of the year, Wood had worked a total of 55,000 direct labor-hours and had incurred $130,500 in actual manufacturing overhead cost. If Job #527 contained 250 units, the unit product cost on the completed job cost sheet would be___. Answerarrow_forward

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT