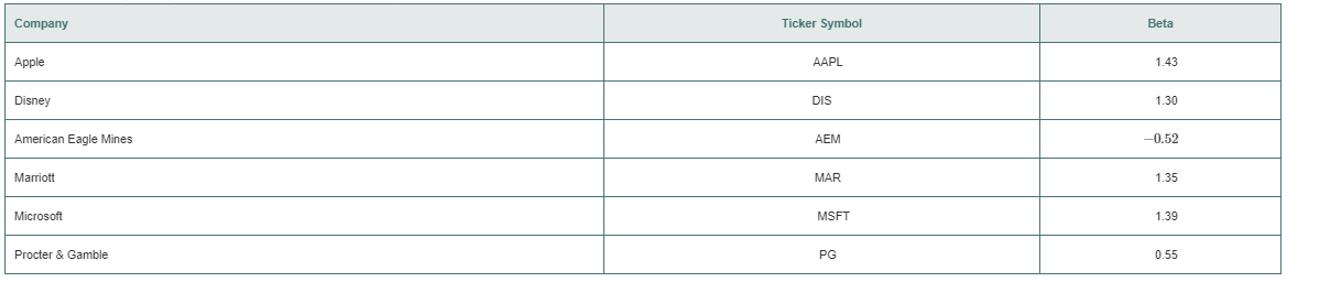

The volatility of a stock is often measured by its beta value. You can estimate the beta value of a stock by developing a simple linear regression model, using the percentage weekly change in the stock as the dependent variable and the percentage weekly change in a market index as the independent variable. The S&P 500 Index is a common index to use. For example, if you wanted to estimate the beta value for Disney you could use the following model, which is sometimes referred to as a market model : ( % weekly change in Disney)Â = β 0 + β 1 ( % weekly change in S amp P 500 index) + ε The least- square regression estimate of the slope b 1 is the estimates of the beta value for Disney. A stock with a beta value of 1.0 tends to move the same as the overall market. A stock with a beta value of 1.5 tends to move 50 % more than the overall market, and a stock with a beta value of 0.6 tends to move only 60 % as much as the overall market. Stocks with negative beta values tend to move in the opposite direction of the overall market. The following table gives some beta values for some widely as of a June 27, 2017: a. For each of the six companies, interpret the beta value. b. How can investors use the beta value as a guide for investing?

The volatility of a stock is often measured by its beta value. You can estimate the beta value of a stock by developing a simple linear regression model, using the percentage weekly change in the stock as the dependent variable and the percentage weekly change in a market index as the independent variable. The S&P 500 Index is a common index to use. For example, if you wanted to estimate the beta value for Disney you could use the following model, which is sometimes referred to as a market model : ( % weekly change in Disney)Â = β 0 + β 1 ( % weekly change in S amp P 500 index) + ε The least- square regression estimate of the slope b 1 is the estimates of the beta value for Disney. A stock with a beta value of 1.0 tends to move the same as the overall market. A stock with a beta value of 1.5 tends to move 50 % more than the overall market, and a stock with a beta value of 0.6 tends to move only 60 % as much as the overall market. Stocks with negative beta values tend to move in the opposite direction of the overall market. The following table gives some beta values for some widely as of a June 27, 2017: a. For each of the six companies, interpret the beta value. b. How can investors use the beta value as a guide for investing?

Solution Summary: The author explains the beta value for each of the six companies. Beta is defined as the measure of risk or volatility of stock.

The volatility of a stock is often measured by its beta value. You can estimate the beta value of a stock by developing a simple linear regression model, using the percentage weekly change in the stock as the dependent variable and the percentage weekly change in a market index as the independent variable. The S&P 500 Index is a common index to use. For example, if you wanted to estimate the beta value for Disney you could use the following model, which is sometimes referred to as a market model:

(

%

weekly change in Disney)Â =

β

0

+

β

1

(

%

weekly change in S amp P 500 index) +

ε

The least- square regression estimate of the slope

b

1

is the estimates of the beta value for Disney. A stock with a beta value of 1.0 tends to move the same as the overall market. A stock with a beta value of 1.5 tends to move

50

%

more than the overall market, and a stock with a beta value of 0.6 tends to move only

60

%

as much as the overall market. Stocks with negative beta values tend to move in the opposite direction of the overall market. The following table gives some beta values for some widely as of a June 27, 2017:

a. For each of the six companies, interpret the beta value.

b. How can investors use the beta value as a guide for investing?

Please could you explain why 0.5 was added to each upper limpit of the intervals.Thanks

28. (a) Under what conditions do we say that two random variables X and Y are

independent?

(b) Demonstrate that if X and Y are independent, then it follows that E(XY) =

E(X)E(Y);

(e) Show by a counter example that the converse of (ii) is not necessarily true.

1. Let X and Y be random variables and suppose that A = F. Prove that

Z XI(A)+YI(A) is a random variable.

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, statistics and related others by exploring similar questions and additional content below.

Correlation Vs Regression: Difference Between them with definition & Comparison Chart; Author: Key Differences;https://www.youtube.com/watch?v=Ou2QGSJVd0U;License: Standard YouTube License, CC-BY

Correlation and Regression: Concepts with Illustrative examples; Author: LEARN & APPLY : Lean and Six Sigma;https://www.youtube.com/watch?v=xTpHD5WLuoA;License: Standard YouTube License, CC-BY

Glencoe Algebra 1, Student Edition, 9780079039897...AlgebraISBN:9780079039897Author:CarterPublisher:McGraw Hill

Glencoe Algebra 1, Student Edition, 9780079039897...AlgebraISBN:9780079039897Author:CarterPublisher:McGraw Hill

Functions and Change: A Modeling Approach to Coll...AlgebraISBN:9781337111348Author:Bruce Crauder, Benny Evans, Alan NoellPublisher:Cengage Learning

Functions and Change: A Modeling Approach to Coll...AlgebraISBN:9781337111348Author:Bruce Crauder, Benny Evans, Alan NoellPublisher:Cengage Learning Algebra and Trigonometry (MindTap Course List)AlgebraISBN:9781305071742Author:James Stewart, Lothar Redlin, Saleem WatsonPublisher:Cengage Learning

Algebra and Trigonometry (MindTap Course List)AlgebraISBN:9781305071742Author:James Stewart, Lothar Redlin, Saleem WatsonPublisher:Cengage Learning Algebra & Trigonometry with Analytic GeometryAlgebraISBN:9781133382119Author:SwokowskiPublisher:Cengage

Algebra & Trigonometry with Analytic GeometryAlgebraISBN:9781133382119Author:SwokowskiPublisher:Cengage College AlgebraAlgebraISBN:9781305115545Author:James Stewart, Lothar Redlin, Saleem WatsonPublisher:Cengage Learning

College AlgebraAlgebraISBN:9781305115545Author:James Stewart, Lothar Redlin, Saleem WatsonPublisher:Cengage Learning