Concept explainers

Videos

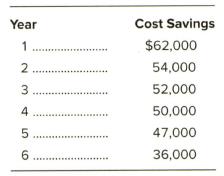

Hercules Exercise Equipment Co. purchased a computerized measuring device two years ago for

A new piece of equipment will cost

The firm's tax rate is 25 percent and the cost of capital is 12 percent.

a. What is the book value of the old equipment?

b. What is the tax loss on the sale of the old equipment?

c. What is the tax benefit from the sale?

d. What is the

e. What is the net cost of the new equipment? (Include the inflow from the sale of the old equipment.)

f. Determine the depreciation schedule for the new equipment.

g. Determine the depreciation schedule for the remaining years of the old equipment.

h. Determine the incremental depreciation between the old and new equipment and the related tax shield benefits.

i. Compute the aftertax benefits of the cost savings.

j. Add the depreciation tax shield benefits and the aftertax cost savings, and determine the

k. Compare the present value of the incremental benefits (j) to the net cost of the new equipment (e). Should the replacement be undertaken?

a.

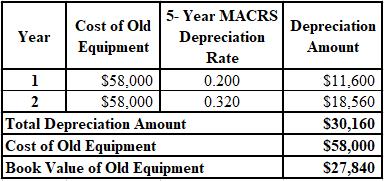

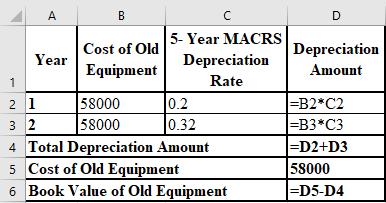

To calculate: The book value of the old equipment.

Introduction:

Book value:

It refers to the total worth of the company if it liquidates all its assets and pays off all the liabilities. It is also referred to as asset price in the balance sheet.

MACRS depreciation method:

MACRS stands for modified accelerated cost recovery system, which is a tool of depreciation used in the U.S. for tax purposes. This system places all the assets into categories with pre-specified depreciation periods.

Answer to Problem 33P

The calculation of the book value of the old equipment is shown below:

Hence, the book value of the old equipment is $27,480.

Explanation of Solution

The formulae used for calculation of the book value of the old equipment are shown below:

b.

To calculate: The tax loss incurred on the sale of the old equipment.

Introduction:

Tax loss:

It is the loss incurred when the total deduction claimed in a financial year exceeds the total assessable income of the year.

Answer to Problem 33P

The tax loss incurred on the sale of the old equipment is $3,040.

Explanation of Solution

The calculation of the tax loss on the sale of the old equipment is shown below:

c.

To calculate: The tax benefit from the sale of the old equipment.

Introduction:

Tax benefit:

It is the allowable deductions on the assessable income of the taxpayer, with an intent to reduce the tax liability and burden of the taxpayer.

Answer to Problem 33P

The tax benefit from the sale of the old equipment is $760.

Explanation of Solution

The calculation of the tax benefit from the sale of the old equipment is shown below:

d.

To calculate: The cash inflow received due to sale of old equipment.

Introduction:

Cash inflow:

It is the money received by the firm as the result of its operating, investing, and financing activities. It is the money which is received in the business and recorded in the cash flow statement.

Answer to Problem 33P

The cash inflow received due to sale of old equipment is $25,560.

Explanation of Solution

The calculation of the cash inflow from the sale of the old equipment is shown below:

e.

To calculate: The net cost of the new equipment.

Introduction:

Net cost:

The cost that is computed by deducting all the expenses related to an object, such as freight costs, discounts, etc. from the gross cost of the object.

Answer to Problem 33P

The net cost of the new equipment is $122,440.

Explanation of Solution

The calculation of the net cost of the new equipment is shown below:

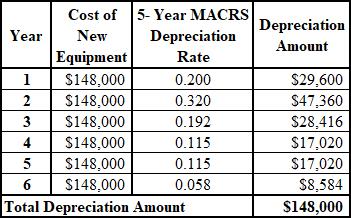

f.

To prepare: The depreciation schedule of new equipment.

Introduction:

Depreciation schedule:

A table that shows the amount of depreciation of a particular asset over the years of its usage is termed as depreciation schedule.

MACRS depreciation method:

MACRS stands for modified accelerated cost recovery system, which is a tool of depreciation used in the U.S. for tax purposes. This system places all the assets into categories with pre-specified depreciation periods.

Answer to Problem 33P

The depreciation schedule of new equipment is shown below:

Explanation of Solution

The formulae used for the preparation of the depreciation schedule of new equipment are shown below:

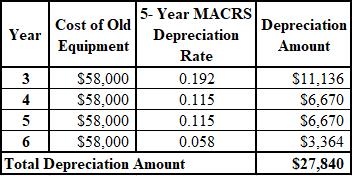

g.

To prepare: The depreciation schedule of remaining years of the old equipment.

Introduction:

Depreciation schedule:

A table that shows the amount of depreciation of a particular asset over the years of its usage is termed as depreciation schedule.

MACRS depreciation method:

MACRS stands for modified accelerated cost recovery system, which is a tool of depreciation used in the U.S. for tax purposes. This system places all the assets into categories with pre-specified depreciation periods.

Answer to Problem 33P

The depreciation schedule of remaining years of the old equipment is shown below:

Explanation of Solution

The formulae used for the preparation of the depreciation schedule of remaining years of the old equipment are shown below:

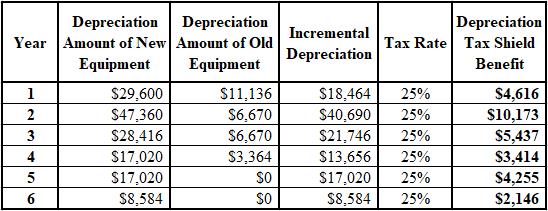

h.

To calculate: The incremental depreciation of old and new equipment and the depreciation tax shield benefit.

Introduction:

MACRS depreciation method:

MACRS stands for modified accelerated cost recovery system, which is a tool of depreciation used in the U.S. for tax purposes. This system places all the assets into categories with pre-specified depreciation periods.

Depreciation tax shield:

It is a particular kind of a tax shield provided to an individual or corporations in which depreciation as an expense is deducted from the taxable income.

Answer to Problem 33P

The calculation of the incremental depreciation of old and new equipment and the tax shield benefit is shown below:

Explanation of Solution

The formulae used for the calculation of the incremental depreciation of old and new equipment and the tax shield benefit are shown below:

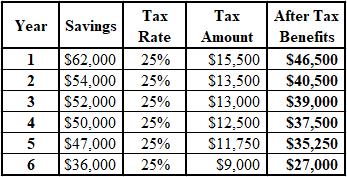

i.

To calculate: The after tax benefits of the cost savings.

Introduction:

After tax benefits:

After tax benefits are those deductions for which the individuals are eligible post the income tax is calculated.

Answer to Problem 33P

The calculation of the after tax benefits of the cost savings is shown below:

Explanation of Solution

The formulae used for the calculation of the after tax benefits of the cost savings are shown below:

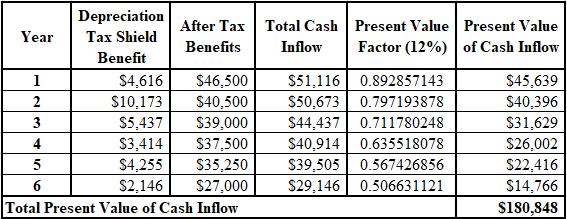

j.

To calculate: The present value of the total cash inflow (sum of depreciation tax shield and after tax benefits).

Introduction:

Present value (PV):

The current value of an investment or an asset is termed as its present value. It is calculated by discounting the future value of the investment or asset.

Cash inflow:

It is the money received by the firm as the result of its operating, investing, and financing activities. It is the money which is received in the business and recorded in the cash flow statement.

Answer to Problem 33P

The calculation of the PV of the total cash inflow is shown below:

Explanation of Solution

The formulae used for the calculation of the PV of the total cash inflow are shown below:

k.

To determine: Whether the replacement shall be undertaken or not.

Introduction:

Net present value (NPV):

It is the difference between the PV (present value) of cash inflows and the cash outflows. It is used in capital budgeting and planning of investment to assess the benefits and losses of any project or investment.

Answer to Problem 33P

The replacement should be undertaken because the NPV of the project is $58,408 and the positive NPV indicates that the replacement is beneficial for the corporation.

Explanation of Solution

The calculation of the NPV of the replacement is as follows:

Want to see more full solutions like this?

Chapter 12 Solutions

EBK FOUNDATIONS OF FINANCIAL MANAGEMENT

- What are some of Airbnb Legal Issues? How have Airbnb Resolved these Legal issues?WHat happened in the legal problem with Airbnb and Italy?arrow_forwardWhat are AIrbnb's Legal Foundations? What are Airbnb's Business Ethics? What are Airbnb's Corporate Social Responsibility?arrow_forwardDiscuss in detail the differences between the Primary Markets versus the Secondary Markets, The Money Market versus the Capital Market AND the Spot Market versus the Futures Market. Additionally, discuss the various Interest Rate Determinants listed in your textbook (such as default-risk premium.....).arrow_forward

- How can the book value still serve as a useful metric for investors despite the dominance of market value?arrow_forwardHow do you think companies can practically ensure that stakeholder interests are genuinely considered, while still prioritizing the financial goal of maximizing shareholder equity? Do you think there’s a way to measure and track this balance effectively?arrow_forward$5,000 received each year for five years on the first day of each year if your investments pay 6 percent compounded annually. $5,000 received each quarter for five years on the first day of each quarter if your investments pay 6 percent compounded quarterly. Can you show me either by hand or using a financial calculator please.arrow_forward

- Can you solve these questions on a financial calculator: $5,000 received each year for five years on the last day of each year if your investments pay 6 percent compounded annually. $5,000 received each quarter for five years on the last day of each quarter if your investments pay 6 percent compounded quarterly.arrow_forwardNow suppose Elijah offers a discount on subsequent rooms for each house, such that he charges $40 for his frist room, $35 for his second, and $25 for each room thereafter. Assume 30% of his clients have only one room cleaned, 25% have two rooms cleaned, 30% have three rooms cleaned, and the remaining 15% have four rooms cleaned. How many houses will he have to clean before breaking even? If taxes are 25% of profits, how many rooms will he have to clean before making $15,000 profit? Answer the question by making a CVP worksheet similar to the depreciation sheets. Make sure it works well, uses cell references and functions/formulas when appropriate, and looks nice.arrow_forward1. Answer the following and cite references. • what is the whole overview of Green Markets (Regional or Sectoral Stock Markets)? • what is the green energy equities, green bonds, and green financing and how is this related in Green Markets (Regional or Sectoral Stock Markets)? Give a detailed explanation of each of them.arrow_forward

- Could you help explain “How an exploratory case study could be goodness of work that is pleasing to the Lord?”arrow_forwardWhat are the case study types and could you help explain and make an applicable example.What are the 4 primary case study designs/structures (formats)?arrow_forwardThe Fortune Company is considering a new investment. Financial projections for the investment are tabulated below. The corporate tax rate is 24 percent. Assume all sales revenue is received in cash, all operating costs and income taxes are paid in cash, and all cash flows occur at the end of the year. All net working capital is recovered at the end of the project. Year 0 Year 1 Year 2 Year 3 Year 4 Investment $ 28,000 Sales revenue $ 14,500 $ 15,000 $ 15,500 $ 12,500 Operating costs 3,100 3,200 3,300 2,500 Depreciation 7,000 7,000 7,000 7,000 Net working capital spending 340 390 440 340 ?arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT