Videos

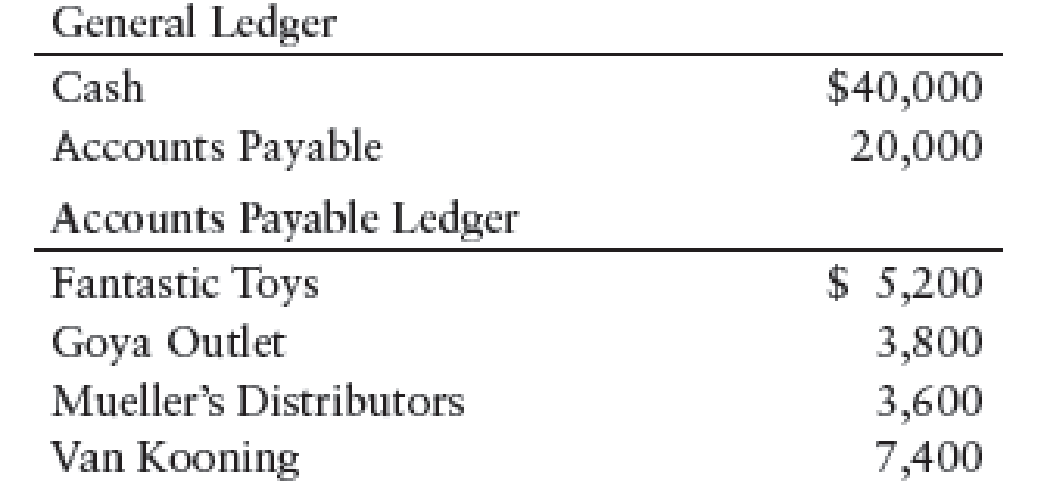

CASH PAYMENTS TR ANS ACTIONS Sam Santiago operates a retail variety store. The books include a general journal and an accounts payable ledger. Selected account balances on May 1 are as follows:

The following are the transactions related to cash payments for the month of May:

May 1 Issued Check No. 426 in payment of May rent (Rent Expense), $2,400.

3 Issued Check No. 427 to Mueller’s Distributors in payment of merchandise purchased on account, $3,600, less a 3% discount. Check was written for $3,492.

7 Issued Check No. 428 to Van Kooning in partial payment of merchandise purchased on account, $5,500. A cash discount was not allowed.

12 Issued Check No. 429 to Fantastic Toys for merchandise purchased on account, $5,200, less a 1% discount. Check was written for $5,148.

15 Issued Check No. 430 to City Power and Light (Utilities Expense), $1,720.

18 Issued Check No. 431 to A-1 Warehouse for a cash purchase of merchandise, $4,800.

26 Issued Check No. 432 to Goya Outlet for merchandise purchased on account, $3,800, less a 2% discount. Check was written for $3,724.

30 Issued Check No. 433 to Mercury Transit Company for freight charges on merchandise purchased (Freight-In), $1,200.

31 Issued Check No. 434 to Town Merchants for a cash purchase of merchandise, $3,000.

Required

- 1. Enter the transactions starting with page 9 of a general journal.

- 2. Post from the general journal to the general ledger and the accounts payable ledger. Use general ledger account numbers as shown in the chapter.

1.

Journalize the cash payment transactions for the month of May.

Explanation of Solution

Journal entry: Journal entry is a set of economic events which can be measured in monetary terms. These are recorded chronologically and systematically.

Debit and credit rules:

- Debit an increase in asset account, increase in expense account, decrease in liability account, and decrease in stockholders’ equity accounts.

- Credit decrease in asset account, increase in revenue account, increase in liability account, and increase in stockholders’ equity accounts.

Journalize the cash payment transactions for the month of May.

Transaction on May 1:

| Page: 9 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| May | 1 | Rent Expense | 521 | 2,400 | ||

| Cash | 101 | 2,400 | ||||

| (Record payment of rent expense) | ||||||

Table (1)

Description:

- Rent Expense is an expense account. An increase in expense reduces the equity value, and a decrease in equity is debited.

- Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Transaction on May 3:

| Page: 9 | ||||||

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| May | 3 | Accounts Payable, M Distributors | 202/✓ | 3,600 | ||

| Cash | 101 | 3,492 | ||||

| Purchases Discounts | 501.2 | 108 | ||||

| (Record cash paid for purchases on account) | ||||||

Table (2)

Description:

- Accounts Payable, M Distributors is a liability account. Since the payable decreased, the liability decreased, and a decrease in liability is debited.

- Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

- Purchases Discounts is a contra-purchases or contra-costs account, and contra-purchases accounts increase the equity value, and an increase in equity is credited.

Working Note 1:

Compute purchases discount value.

Transaction on May 7:

| Page: 9 | ||||||

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| May | 7 | Accounts Payable, VK | 202/✓ | 5,500 | ||

| Cash | 101 | 5,500 | ||||

| (Record cash paid for purchases on account) | ||||||

Table (3)

Description:

- Accounts Payable, VK is a liability account. Since the payable decreased, the liability decreased, and a decrease in liability is debited.

- Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Transaction on May 12:

| Page: 9 | ||||||

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| May | 12 | Accounts Payable, F Toys | 202/✓ | 5,200 | ||

| Cash | 101 | 5,148 | ||||

| Purchases Discounts | 501.2 | 52 | ||||

| (Record cash paid for purchases on account) | ||||||

Table (4)

Description:

- Accounts Payable, F Toys is a liability account. Since the payable decreased, the liability decreased, and a decrease in liability is debited.

- Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

- Purchases Discounts is a contra-purchases or contra-costs account, and contra-purchases accounts increase the equity value, and an increase in equity is credited.

Working Note 2:

Compute purchases discount value.

Transaction on May 15:

| Page: 9 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| May | 15 | Utilities Expense | 533 | 1,720 | ||

| Cash | 101 | 1,720 | ||||

| (Record payment of utilities expense) | ||||||

Table (5)

Description:

- Utilities Expense is an expense account. An increase in expense reduces the equity value, and a decrease in equity is debited.

- Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Transaction on May 18:

| Page: 9 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| May | 18 | Purchases | 501 | 4,800 | ||

| Cash | 101 | 4,800 | ||||

| (Record purchase of inventory) | ||||||

Table (6)

Description:

- Purchases is an expense account which records the cost of inventory purchased. An increase in expense reduces the equity value, and a decrease in equity is debited.

- Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Transaction on May 26:

| Page: 9 | ||||||

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| May | 26 | Accounts Payable, G Outlet | 202/✓ | 3,800 | ||

| Cash | 101 | 3,724 | ||||

| Purchases Discounts | 501.2 | 76 | ||||

| (Record cash paid for purchases on account) | ||||||

Table (7)

Description:

- Accounts Payable, G Outlet is a liability account. Since the payable decreased, the liability decreased, and a decrease in liability is debited.

- Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

- Purchases Discounts is a contra-purchases or contra-costs account, and contra-purchases accounts increase the equity value, and an increase in equity is credited.

Working Note 3:

Compute purchases discount value.

Transaction on May 30:

| Page: 9 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| May | 30 | Freight-In | 502 | 1,200 | ||

| Cash | 101 | 1,200 | ||||

| (Record payment of freight charges) | ||||||

Table (8)

Description:

- Freight-In is an expense account. An increase in expense reduces the equity value, and a decrease in equity is debited.

- Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Transaction on May 31:

| Page: 9 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| May | 31 | Purchases | 501 | 3,000 | ||

| Cash | 101 | 3,000 | ||||

| (Record purchase of inventory) | ||||||

Table (9)

Description:

- Purchases is an expense account which records the cost of inventory purchased. An increase in expense reduces the equity value, and a decrease in equity is debited.

- Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

2.

Post the given transactions into the accounts of the general ledger, and the suppliers account in accounts payable ledger.

Explanation of Solution

Posting transactions: The process of transferring the journalized transactions into the accounts of the ledger is known as posting the transactions.

Post the given transactions into the accounts of the general ledger.

| ACCOUNT Cash ACCOUNT NO. 101 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| May | 1 | Balance | ✓ | 40,000 | |||

| 1 | J9 | 2,400 | 37,600 | ||||

| 3 | J9 | 3,492 | 34,108 | ||||

| 7 | J9 | 5,500 | 28,608 | ||||

| 12 | J9 | 5,148 | 23,460 | ||||

| 15 | J9 | 1,720 | 21,740 | ||||

| 18 | J9 | 4,800 | 16,940 | ||||

| 26 | J9 | 3,724 | 13,216 | ||||

| 30 | J9 | 1,200 | 12,016 | ||||

| 31 | J9 | 3,000 | 9,016 | ||||

Table (10)

| ACCOUNT Accounts Payable ACCOUNT NO. 202 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| May | 1 | Balance | ✓ | 20,000 | |||

| 3 | J9 | 3,600 | 16,400 | ||||

| 7 | J9 | 5,500 | 10,900 | ||||

| 12 | J9 | 5,200 | 5,700 | ||||

| 28 | J9 | 3,800 | 1,900 | ||||

Table (11)

| ACCOUNT Purchases ACCOUNT NO. 501 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| May | 18 | J9 | 4,800 | 4,800 | |||

| 31 | J9 | 3,000 | 7,800 | ||||

Table (12)

| ACCOUNT Purchases Discounts ACCOUNT NO. 501.2 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| May | 3 | J9 | 108 | 108 | |||

| 12 | J9 | 52 | 160 | ||||

| 26 | J9 | 76 | 236 | ||||

Table (13)

| ACCOUNT Freight-In ACCOUNT NO. 502 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| May | 30 | J9 | 1,200 | 1,200 | |||

Table (14)

| ACCOUNT Rent Expense ACCOUNT NO. 521 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| May | 1 | J9 | 2,400 | 2,400 | |||

Table (15)

| ACCOUNT Utilities Expense ACCOUNT NO. 533 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| May | 15 | J9 | 1,720 | 1,720 | |||

Table (16)

Post the accounts payable balances of the suppliers to the supplier accounts in the accounts payable ledger.

| NAME F Toys | ||||||

| ADDRESS | ||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance ($) | |

| May | 1 | Balance | ✓ | 5,200 | ||

| 12 | J9 | 5,200 | 0 | |||

Table (17)

| NAME G Outlet | ||||||

| ADDRESS | ||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance ($) | |

| May | 1 | Balance | ✓ | 3,800 | ||

| 26 | J9 | 3,800 | 0 | |||

Table (18)

| NAME M Distributors | ||||||

| ADDRESS | ||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance ($) | |

| May | 1 | Balance | ✓ | 3,600 | ||

| 3 | J9 | 3,600 | ||||

Table (19)

| NAME VK | ||||||

| ADDRESS | ||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance ($) | |

| May | 18 | Balance | ✓ | 7,400 | ||

| 7 | J9 | 5,500 | 1,900 | |||

Table (20)

Want to see more full solutions like this?

Chapter 11 Solutions

College Accounting, Chapters 1-9 (New in Accounting from Heintz and Parry)

- I want to correct answer general accounting questionarrow_forwardQuestion Content Area Work in Process Account Data for Two Months; Cost of Production Reports Pittsburgh Aluminum Company uses process costing to record the costs of manufacturing rolled aluminum, which consists of the smelting and rolling processes. Materials are entered from smelting at the beginning of the rolling process. The inventory of Work in Process—Rolling on September 1 and debits to the account during September were as follows:arrow_forwardQuestion Content Area Work in Process Account Data for Two Months; Cost of Production Reports Pittsburgh Aluminum Company uses process costing to record the costs of manufacturing rolled aluminum, which consists of the smelting and rolling processes. Materials are entered from smelting at the beginning of the rolling process. The inventory of Work in Process—Rolling on September 1 and debits to the account during September were as follows:arrow_forward

- A B CORRECT ANSWER PLEASarrow_forwardKindly help me with accounting questionsarrow_forward1. I want to know how to solve these 2 questions and what the answers are 3. Field & Co. expects its EBIT to be $125,000 every year forever. The firm can borrow at 7%. The company currently has no debt, and its cost of equity is 12%. If the tax rate is 24%, what is the value of the firm? What will the value be if the company borrows $205,000 and uses the proceeds to purchase shares? 2. Firms HD and LD each have $30m in invested capital, $8m of EBIT, and a tax rate of 25%. Firm HD has a D/E ratio of 50% with an interest rate of 8% on their debt. Firm LD has a debt-to-capital ratio of 30%, however, pays 9% interest on its debt. Calculate the following: a. Return on invested capital for firm LDb. Return on equity for each firmc. If HD’s CFO is thinking of lowering the D/E from 50% to 40%, which will lower their interest rate further from 8% to 7%, calculate the new ROE for firm HD.arrow_forward

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage LearningCentury 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage LearningCentury 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage College Accounting (Book Only): A Career ApproachAccountingISBN:9781305084087Author:Cathy J. ScottPublisher:Cengage Learning

College Accounting (Book Only): A Career ApproachAccountingISBN:9781305084087Author:Cathy J. ScottPublisher:Cengage Learning